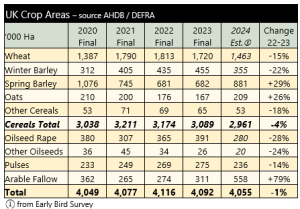

Rainfall in the UK between August 2023 and February 2024 is the second highest for the period since records began in 1837. This has caused major challenges for crop planting for the 2024 harvest. In December, AHDB published the Early Bird Survey showing planting intentions for the coming year. With weather issues continuing the Survey has been re-run capturing planting intentions up to the end of March.

Wheat planting is down 15% on the year at 1.46 million hectares; this includes a significant increase in spring wheat planting. In 2019/20, the last seriously wet planting season, spring barley area increased considerably to pick up the slack. The area of spring barley is forecast to increase for harvest 2024, to 881,000 hectares. The oat area is also forecast to increase in response to the challenged winter planting conditions, with farmers seeing spring oats as an option. The oat area is forecast at 208,000 hectares, an increase of 26%. These spring cereals plantings are only the intentions of farmers. The weather over the next few weeks will determine whether these intentions can be turned into actions.

Oilseed rape has also been challenged significantly, both by poor establishment conditions and increased pest pressure, notably from slugs, in the autumn. The result is a 28% decline in the area likely to be taken through to harvest at 280,000 hectares.

One of the most notable increases this year is that of arable fallow, up 79%, to 558,000 hectares. This area is will include a proportion of land which will be placed into environmental schemes.

Area figures only give a part picture of the state of cropping in the UK this season. Whilst areas of winter crops are down there are significant area of crops in poor or very poor condition. Very little of the poorer quality crop will be re-drilled, as such it will be carried forward with lower yield prospects.