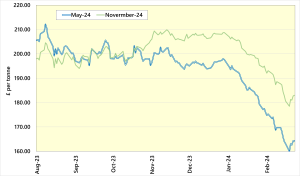

Grain prices fell considerably during February. The May-24 UK Feed Wheat Futures contract started the Month at £175 per tonne, as of 24th February the same contract was worth £164 per tonne. It is a similar story for the 2024 crop, with November-24 Futures £9 per tonne lower on the month.

The direction of the UK market is driven by the availability of global grains. Concern had been building about dry conditions in South America hindering planting progress. However, both Brazil and Argentina have received rainfall and planting of maize and soyabeans has progressed. Argentina is forecast to harvest an additional 22.5 million tonnes of maize in 2023/24 compared to 2022/23 (when it was affected by a widespread drought). Brazilian grain and oilseed production forecast have fallen. However, the country is still expected to harvest a combined 300 million tonnes of cereals and oilseeds; the second largest harvest on record.

Furthermore, grain prices are weighed down by cheap Black Sea wheat, slow US grain and oilseed exports, and the large sold position held by speculative traders in US grain futures.

Looking ahead to the 2024 UK harvest, the window of opportunity for further winter wheat plantings, prior to latest safe sowing dates, is closing. Heavier ground is still sodden, especially across the East Midlands. Crops on lighter land look far better. UK growers face the prospect of smaller crops being sold at lower prices. The poor outlook for the 2024 harvest is increasingly accounted for in grain prices. Looking at the gap between old crop and new crop wheat futures (May-24 versus November-24), the new crop is worth almost £19 per tonne more that the old crop. This time last year the November crop (November-23) was worth just £3 per tonne more than the old crop (May-23).

UK Feed Wheat Futures Chart

Source: AHDB

Farmgate grain prices have reflected the wider trend in futures, as shown in Key Farm Facts. The UK still has ample old crop wheat and barley stocks, with prices uncompetitive into export markets.