The spread of the Covid 19 coronavirus has seen the world stop working as we understand it. The impact on the supermarkets and food availability for consumers has been clear. Here are our thoughts on the crisis on the wider food and farming industry. They can be divided into short, medium and long-term implications.

Short Term

The Consumer: Supermarket shelf stripping has been a consequence of both panic buying and preparing to feed families and elderly for prolonged periods without the use of food service, restaurants and coffee shops. Consequently, the demand for most goods including milling wheat for bread and biscuits has rocketed; the broiler kill rate has gone up sharply and the demand for other meats has also increased hugely. The emergency is to replace the empty shelves with goods for the consumer.

Total food requirements should not change overall. So presumably demand will slow at some point soon when people’s stores and freezers are full. However, eating habits in the home differ from the restaurant or food service. With no eating out, evidence suggests consumption of expensive cuts of beef and lamb and ‘top-end’ cheeses such as Stilton will probably fall after a while. We would expect more chicken and lower priced pig and beef meat for burgers and sausage style foods. Perhaps people will eat more healthily, with more vegetables rather than a typical restaurant pizza or burger option, so demand may shift. Beer consumption is falling around the world, people drink less in the home and less alone.

We are also finding several farmers, notably some dairy farmers are struggling to sell their farm goods at the normal prices because they supply the food chain that ends up in the food-service or catering outlets. Suppliers of high-end cheese manufacturers for example are not being paid in full, as most quality cheeses are consumed in restaurants. Other suppliers of places like burger bars and fast food chains are also seeing their conventional supply tailing off. It is clearly taking a while for these supply lines to re-route to where the food is desperately needed.

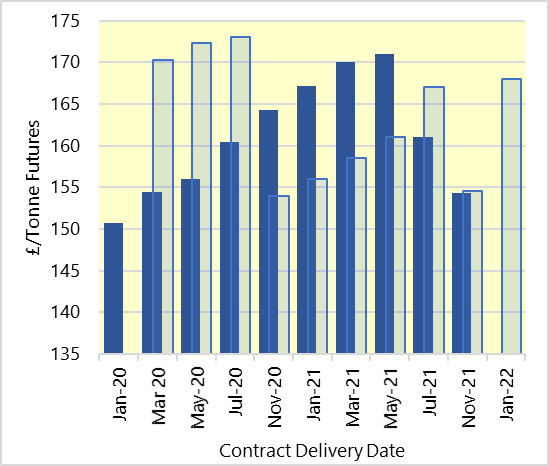

Prices: Commodity prices move when demand and supply are not aligned. Expect some volatility. Prices for all the goods mentioned above where demand has risen would be expected to go up (such as wheat up £10 per tonne). Overall trends may take some time to establish according to how the supply chain manages the flow of goods and how the consumer changes their habits.

Medium Term

The Farmer: Farmers are relatively good ‘self-isolators’ already. We would expect many to be able to ‘carry on farming’ with most farms operating as usual as long as supplies get through. However, staff absences could lead to livestock welfare issues, diversified business dependant on general public foot fall could be hard hit, and estates renting out cottages may be affected as tenants can stop paying rent without the threat of eviction. The only support farmers will get is loans or Statutory Sick Pay refunds as the Government grants announced by the Chancellor, Rishi Sunak, are based on Business Rates at present and (undiversified) farmers don’t pay rates.

Farm Workers: Access to casual migrant labour is going to become a big issue if travel bans remain in place over the summer. The Farmers Weekly reports that appeals have started to go out for British workers to work on farms. This is easier said than done if everybody is staying indoors.

Supply Chain: This is where we see problems of maintaining physical turnover because of lower staffing. Abattoirs, packing sheds, mills and other points where bulk commodity starts its transition into branded food products is largely labour intensive and cannot be done at home. They require lines of people working closely together in sheds. Many people will not be happy to work in these conditions. Whether work can be taken outdoors, or spread out will depend on each facility, but it is likely that turnover may fall sharply in some locations.

The flow of cash has also already started to slow, with many firms hoarding cash and not paying each other. Expenditures that are not short-term-critical are also being postponed. Profitable businesses unable to turn their profits into cash will struggle in coming weeks and months. Some supermarkets have committed to pay small manufacturers more quickly than usual.

Retailers are already shifting resources in their outlets towards the supermarket floor and fulfilling online demand. Whether this distracts them from purchasing and supply roles will depend on how well they are managed.

Trade: Travel restrictions do not apply to medical staff, medicines or, crucially, goods. However, there are inevitably going to be plenty of supply-chain glitches, people going into self-isolation, shipping containers not where they are supposed to be etc. There is no news yet on such matters.

Trade Negotiations: Michelle Barnier, the EU’s Chief Brexit negotiator, has got Coronavirus. The UK-EU trade talks had already been put on hold in any event. This has led to speculation that the Brexit Transition Period, in which the trade talks should have been completed, will be extended. However the UK Government is currently sticking to the line that the Transition will end on the 31st December. The deadline for triggering any extension is 31 July. We await announcements.

Long Term:

Policy: The severe shortages of food availability in the shops, and the images of desperate panic-buying shoppers might encourage Defra, and Government more widely, to rethink its policies on food security. Currently, there is peace of mind in Defra that 80% of our imports have been from ‘friendly neighbours’ in the EU. Might Defra consider that more home-produced goods could be a strategic benefit?

Industries will also look towards Government to support the rebuilding of the UK economy when this calms down. The cost will be immense. Whether it will mean major infrastructure projects like HS2 will be postponed remains to be seen.

Supply Chains: Following the horsemeat scandal of 2013, some food supply chains went to great effort to shorten their linkages, source from fewer and more local outlets. Perhaps this will do the same. ‘Local food’ almost became a brand in its own at that point, certainly becoming more powerful than simple patriotism when swaying shoppers how to buy.

Globalisation: The expansion of global trade routes since 2000 has been considerable, and given consumers more choice, lower inflation, cheap goods and created cost savings. However, events like Covid -19 could lead to new procurement policies, with maximum percentages from certain countries or suppliers, for example. Will this lead to a refocus on nationalisation, albeit for a short while? It might fit with some of the Brexit mantras we have been hearing.

Businesses Generally: Coronavirus will bankrupt more than it kills. Several high-profile companies have already been floored, presumably not to recover. If businesses have to take out (Government backed) loans to continue in business, these still need to be paid back at some point. This may lead to lower investment in the future and possibly reduced future profitability. Some firms will use the loans to provide liquidity as their profits are tied up in non-cash forms such as debtors or valuations.

The Economy: Whilst customers and consumers stay in their houses, the economy is in freefall. The economic effects of the pandemic look set to outstrip the recession of 2007 to 2009, even though the UK economy a month ago was in a much stronger position than it was back then. The concern of the markets is shown in the collapse of the Pound (reaching its lowest point against the dollar for 35 years). This actually helps farming, as it makes goods imported into the UK cost more in Sterling terms. Commodity prices move as a response to currency shifts immediately, whereas other goods such as agricultural inputs, wages and rent change very slowly. Thus, the rise in price will favour the farming community. But it will not take long to for a weak Pound to fuel inflation and the new Governor of the Bank of England, Andrew Bailey, will have to act quick to stop it when necessary. Both the Governor of the Bank of England and the Chancellor have both been in their posts for less than 5 weeks!