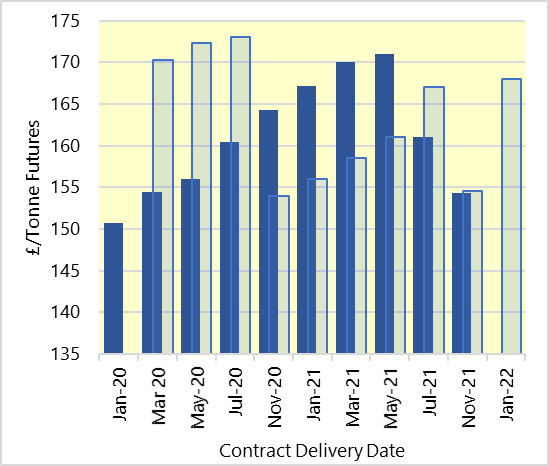

This time last year, we showed the chart below with the faded bars. It demonstrated wheat was priced with a typical carry as it goes through the year; with the monthly rise in value the longer you keep it to account for the costs of storage. It also showed the usual drops in value each year when the new crop physically comes into the marketplace.

The dark blue bars show this year’s equivalent set of futures prices, and how there is a full carry from now all the way through to May 2021. In other words there is no drop in price when the flush of new crop becomes available this summer. It demonstrates that the market understands that there might not be much harvest to account for the flush. Only when we get to the summer of next year, do we see wheat futures prices start to fall.

| UK Wheat Futures Price – source AHDB |

Old crop wheat is currently cheaper than new crop, but is still dearer than equivalent continental values meaning they are too expensive to secure exports to EU destinations. It also suggests that, if the supply situation changes in coming weeks, the market might fall considerably. This may be prompted if there are enough dry conditions for the many farmers still sitting on their winter wheat seed, some varieties of which could still be planted well into February, to get some more drillings done. Globally, wheat prices are strong, sitting at levels not seen at all in 2019. Some with a crop already safely growing, will see this as an opportunity to sell some new crop forward now.

Higher wheat prices have boosted feed barley values this month too. This has been coupled with some useful exports, particularly from old crop. New crop barley could be a big one this year, with large volumes of spring barley seed committed or delivered. The markets (both wheat and barley) will be sensitive to both the ongoing weather throughout the spring and also the updates on drilling. We do not expect a million hectares of spring barley to be drilled, but it largely depends on how the weather turns out in coming weeks. Wherever possible, many growers are still very focussed on getting their wheat in the ground. It is difficult selling even the feed base forward this year as currently, many farmers are not even sure what they will harvest.

It is emerging that large crops of soybean from the southern Hemisphere, Brazil in particular, are expected this coming year, and other regions such as Ukraine are looking to grow more oilseed rape. This, coupled with trade talks between the Chinese and Americans, has seen oilseed rape lose some value.

Old crop pulses have been rising in price this month, partly because of demand for the protein, but also, it is thought, as growers hold tonnages back for potentially drilling. Winter beans can be drilled relatively late, and of course, spring beans might also play an important role in the 2020 rotation. Many seed merchants have sold out of bean seed and potentially, we could have the largest pulse cropped area the UK has recorded for many years. It takes a long time to multiply beans up (compared with cereals and especially oilseed rape), hence the high proportion of home saved seed.