Tag: global grain

Grain Market Update

Old crop UK feed wheat futures prices (May-25) declined through February. There has been little news to support prices for some time. Large opening stocks, high levels of imports and subdued demand will mean the current trend likely continues. The large import levels of milling wheat in particular have reduced the milling wheat premium from an early season peak of £60 per tonne to around £25 now.

Whilst old crop prices have fallen, new crop prices (Nov-25) have increased, driven by rising global grain markets. US maize futures in particular have increased considerably in recent months. Speculative traders (managed money funds) have bought considerable volumes of maize futures, elevating prices. The weather outlook for maize production in both North and South America had been in question, including excess rainfall in Brazil. In the main maize producing region of Mato Grosso, planting of maize is more than eight percentage points behind the five-year average. However, the forecast is for improved weather.

The US weather has also been a key focus. Key wheat producing states in the US have been on the receiving end of temperatures as much as 15C below normal for February. However, this picture is also improving. Additionally, the current market price dynamics for maize and soyabeans in the US is expected to drive an increase in maize planting for 2025. The price gap between old and new crop could close quickly if the funds started selling.

In the short term, there has been support for UK feed barley prices with export demand driving selling opportunities. This has been much-needed owing to the surplus of out-of-specification malting barley adding to the feed heap from harvest 2024.

One positive aspect for arable markets is the strength of the oilseed rape price. That said, the crop area has declined significantly in recent years meaning the price support will only the minority of cereals farmers still growing the crop. In addition, the positive price movement in oilseed rape may not be enough to tempt nervous growers of the crop for 2025 harvest to sell.

A final point worth noting is the direction of fertiliser prices. Natural gas prices, a key input in the production of ammonium nitrate, hit the highest point since October 2023 in February. Prices have fallen back, but remain almost twice as high as the same point last year. So far we have seen an increase in nitrogen prices in the UK market in 2025, but not to the same level as has been observed on the Continent.

Global Grain Update

Global grain prices have been falling for much of 2024. The main driver of the decline has been ample supplies of grain anticipated to come from South America. Maize and soyabeans in Argentina and Brazil are still developing, making prices volatile in response to weather conditions. Concerns over excess rainfall in the region prompted some fund managers to cover some of their record sold positions, supporting prices in the third week of March. The role of fund managers in Chicago grain and oilseed futures markets is important for the direction of global prices. If weather conditions turn, or other funds become more or less attractive the price of grain can move quickly.

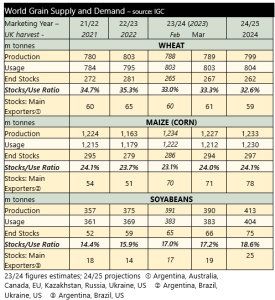

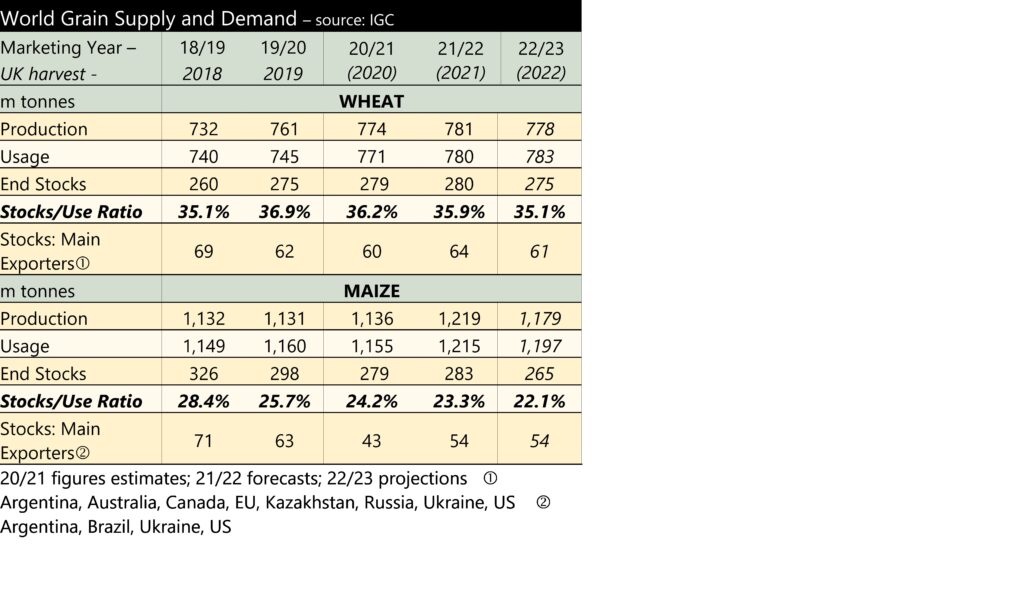

With regard to supply and demand, the International Grains Council (IGC) published its latest update for the 2023/24 season, on the 14th March. Furthermore, the IGC also published its first forecasts for 2024/25. These are shown below.

Despite cuts to global grain production in the Southern Hemisphere for the 2023/24 season, there is a greater fall in estimated consumption, resulting from reductions in feed use. As a result global stocks are forecast to increase by 10 million tonnes.

For 2024/25, the global grain and soyabean stocks are due to rise again. Whilst an increase in stocks is likely to move prices lower, the year-on-year rise is fairly small. We are still some months away from the Northern Hemisphere harvest, and it would not take a big reduction in production (forecast or actual) to move global prices higher.

For the 2024/25 season, total grains production is forecast to rise by 28 million tonnes, 10 million tonnes of that rise is wheat. Increases in wheat production are projected for Argentina, Australia, Canada and the USA. Production is expected to fall in the EU, and the Black Sea. However, usage of wheat is set to remain high and global stocks are forecast to fall by 5 million tonnes between 2023/24 and 2024/25. This may provide some specific support to wheat prices.

Grain Market Update

The August USDA World Supply and Demand Estimates forecast a slight drop in production relative to the July report. This is driven by a reduced outlook for Canadian and European wheat production. Additionally, US maize production forecasts were reduced slightly with lower yields expected, following results from a producer survey. The sentiment for reducing supply and demand forecasts (month-on-month) is echoed by the International Grains Council who cut both production and stock forecasts for total grains.

Although estimates have been reduced, this years global harvest is forecast to be considerably larger than last years, putting downwards pressure on prices. As harvests continue across the Northern Hemisphere, and better yield information becomes available, wheat prices have continued to fall. Suggestions of large crops in Russia, and the ease of shipping costs compared to the same time last year has moved spot feed wheat prices lower after the late July spike.

In the UK, the changeable weather continues to result in a challenging, stop-start harvest, although progress improved at the end of August. In the South and East, many businesses have now finished harvest for another year. Reports suggest that both yield and quality are down on last year, with lower proteins and hagbergs a potential challenge for the milling supply chain. Malting barley nitrogens are low, a positive; but bushel weights are also low.

In August, UK feed wheat values average just over £174 per tonne, down £4 per tonne on the July average. Milling wheat values have also moved lower, down nearly £5 per tonne on the July average, at £237 per tonne. There is still a considerable premium of milling wheat over feed (£62 per tonne) which will be supported if quality issues turn out to be correct..

The discount of feed barley to feed wheat has narrowed over the past month. Reduced availability of the crop has pushed the discount to £22 per tonne on average across August, compared with £28 per tonne in July. In the last week of August the discount was as narrow as £17 per tonne.

The supply and demand for oilseeds has also eroded prices this month. There is larger availability of oilseed rape in Europe this season, with expectations of significant carryover into the 2024/25 season. The oilseed rape price averaged £349 per tonne in August, down from £362 per tonne in July.

The value of pulse crops has taken the biggest hit over the last month. The price of feed beans and feed peas fell by £37 and £41 per tonne, respectively, mont-on-month. With harvest underway greater availability. Early reports suggested that quality has been variable.

Global Grain Markets

Global factors have been key for grain pricing in June, with wheat moving up, largely supported by maize.

Maize has been the significant driver of global grain prices, with drought conditions seemingly worsening through to 20th June. A USDA report of that date showed 67% of the US maize crop to be in moderate to extreme drought. Some parts of the ‘Corn Belt’ have now received rain, but much more is needed and at present this is not forthcoming in the forecast.

There is still significant time to go until the crop is harvested. The crop will begin silking (flowering) soon. Once silking starts, soil moisture, or lack thereof, will become increasingly important for yields.

At present, the USDA are forecasting a record maize crop for the US (388 million tonnes), based on a trend yield. Additionally, US maize ending stocks are forecast to grow by more than 20 million tonnes. With world maize stocks expected to grow by 16 million tonnes, year-on-year, any problems with US production would be supportive of grain prices. This remains an ongoing watch point.

Another key supportive factor for wheat prices is the situation in Ukraine. The short-lived rebellion by the Wagner Mercenaries on 24th June led to some increases in wheat price during the day on Monday. The Black Sea Grain Initiative is also due on 17th July; posturing by all sides in the run up to this date will be a key influencer of price.

The outlook for crops in the EU worsened in June, with the EU Joint Research Centre revising its yield forecasts for all crops lower. For winter crops, most forecasts remain above the five-year average. A key driver of the cuts to yield forecasts is the dry conditions being experienced by much of Northern Europe.

Global Grain Supply & Demand

Global grain and oilseed markets have continued to fall over the past month. A large driver of the drop in wheat prices was the renewal of the Black Sea Initiative. The deal was renewed for a further 60 days on 17th May 2023. The shorter deal length drives greater uncertainty for the global supply chain. The deal now runs until 18th July 2023. There were moments during the last 60-day period where an extension seemed less likely; this resulted in temporary price spikes.

The renewal of the Black Sea Grain Initiative comes at a time when forecasts of Russian wheat production have increased, also pressuring prices. Whilst the Black Sea Grain Initiative is vital to market direction, we also must pay attention to the underlying supply and demand fundamentals.

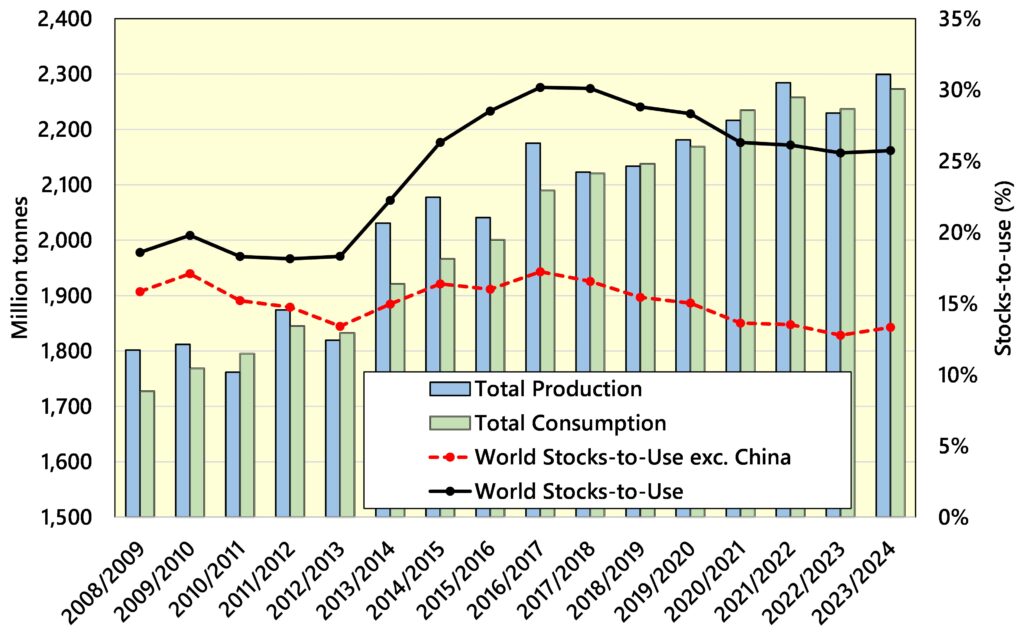

In May, the USDA released its first estimates of 2023/24 global grain supply and demand. In contrast to the International Grains Council (IGC) forecasts, the USDA sees a softening of the grain balance, year-on-year, with significant maize stock growth offsetting a fall in wheat stocks. The IGC’s updated 2023/24 forecasts show a further tightening of the global supply and demand. The chart shows the USDA figures with production exceeding consumption. It also translates this into year-end stock figures. Whilst, on the headline stock figures, the world looks well-supplied with grain, taking China out of the calculation shows the world is in a far tighter position. China tends to hold its stocks for strategic rather than trading reasons and they don’t really contribute to the availability of grain to the rest of the world.

The US and Global maize crop are an important element of the softening USDA supply and demand picture. Maize production is expected to increase by 69 million tonnes globally, and stocks by 15 million tonnes. The US alone is expected to account for 39 million tonnes of the production increase, while seeing its stocks rise by 20 million tonnes.

The US maize crop is currently 81% planted (week ending 21st May). Crop conditions will need to be watched closely for their impact, either positive or negative, on crop potential and so, price. At present the outlook for maize in the US remains positive.

In Europe there have been contrasting weather conditions. Conditions have generally been favourable in Northern Europe, albeit with too much rain during spring planting. However, prolonged drought in Spain is causing concern. Grain yields in Spain are forecast to be down by 30-40% against the five-year average, by the EU Joint Research Centre. This may support demand for UK barley exports.

Black Sea Grain and Global Markets

UK feed wheat futures contracts for May-23 and November-23 delivery dropped by £31 and £20 per tonne respectively between 1st March and 23rd March. Declines have been driven by the renewal of the Black Sea grain corridor and good prospects for EU crops.

The Black Sea grain deal allowing shipments of grain from Ukrainian ports (mainly Odessa) has now been renewed, but only for 60 days. Previous extensions have been for 120 days; the shorter agreement length means commodity traders will have to contend with a greater degree of geopolitical uncertainty. That said, the continued transit of grain through the Black Sea is bearish for grain pricing.

Old crop (May-23) futures rallied by almost £10 per tonne on Friday 24th March, on suggestions that Russia would not grant export licenses for shipments below a certain price. Theoretically this sets a floor to old crop grain prices.

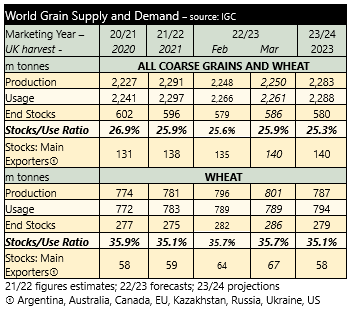

The International Grain Council (IGC) published and updated forecast for 2022/23, and its first estimates of global grain supply and demand for the 2023/24 season. In 2022/23 (harvest 2022 in the UK) the supply and demand situation is seen softening, with growth in ending stocks driven by reduced consumption. However, for 2023/24 the grain market is projected to be tighter year-on-year – again driven by consumption. The level of global grain ending stocks is forecast to fall by 5.4 million tonne year-on-year.

With concerns already for the lack of rainfall in parts of the USA and the EU any adverse weather for the 2023/24 crop would support prices. The first wheat condition reports in the USA are due in early April, alongside the first update on maize plantings. Early yield estimates for the EU suggest a 3% increase for wheat, versus the five year average.

Global Grain and Oilseed Markets

Throughout November the price of grain has fallen back considerably. Futures prices were dropping before the announcement of a 120-day extension to the Ukrainian grain export corridor, 17th November. Global grain markets have softened primarily on expectations of a large maize crop. The crop underpins global feed and industrial (ethanol) markets.

There are expectations of record maize production in South America, in response to high prices. Brazilian weather conditions appear well suited to a big crop. Conversely, Argentina is also forecast for a record maize crop despite currently experiencing a severe drought. The drought in Argentina has, however, trimmed production outlooks for wheat. South American weather remains a key watch point for grain markets, particularly with an active La Niña (the third in three years). La Niña brings dry weather to South America.

Despite forecasts for bumper maize production, the balance of global grain supply and demand remains tight. This ought to offer some underlying support. However, concerns about the impact of recession on demand, particularly industrial demand, seem to be outweighing this fundamental tightness.

Demand concerns are also impacting global oilseed prices. China’s zero-tolerance approach to Covid is driving expectations of reduced palm oil demand. This, combined with increased palm oil production in Southeast Asia, has depressed prices. This has impacted rapeseed markets with the underlying value of rapeseed oil falling. Additionally, a rebound in Canadian canola (rapeseed) production following last year’s disastrous crop is leaving global oilseeds well supplied.

Global Grain Production

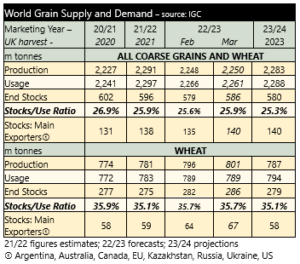

The latest International Grains Council (IGC) supply and demand figures show a year-on-year reduction of stocks of grains globally. The change in global grain supply is driven by tighter maize production, the price of which underpins the feed grains market.

The IGC forecast of maize production is ten million tonnes lower than it was in July at 1,179 million tonnes. If realised, maize production would be 40.9 million tonnes lower than in 2021/22. Even with a fall in usage, ending stocks would be 5% lower year-on-year. The maize production forecast has mostly declined due to the conflict in Ukraine. However, the impact of drought conditions in the EU cannot be overstated. Maize production in the EU is forecast at 59.6 million tonnes in 2022/23, down 8.7 million tonnes from the IGC’s July forecast.

Wheat production is forecast to decline by 2.9 million tonnes, whilst usage is seen rising by 2.5 million tonnes. Global wheat stocks are forecast to decline by 4.6 million tonnes. Excluding Chinese supply and demand from the equation, global stocks are estimated to fall by almost nine million tonnes.

With the grains supply and demand balance tightening, year-on-year, we can expect support for grain prices to remain. But, bear in mind that the lack of supply from Ukraine will already be priced-in to some degree. Any positive changes in the conflict will still drive a fall in prices.

The oilseed market is moving in the opposite direction to grains. World soyabean production is expected to increase by almost twelve million tonnes. Ending stocks of soyabeans are forecast to rise by almost ten million tonnes. The next forecasts of global supply and demand from the USDA are due on 12th September 2022, with the next IGC figures published on 22nd September 2022.

Ukrainian Grain Shipments

On 22nd July, Russia and Ukraine reached an agreement to allow shipments of grain to leave Black Sea ports. Reports suggest that up to 20 million tonnes of old-crop grain, needs to be exported from Ukraine. Understandably, the news of the grain deal caused markets to fall significantly, owing to expectations of increased grain availability. UK feed wheat futures (November 2022) dropped by £16.75 per tonne on the day.

Prices have since recovered, despite the first vessels having left Ukraine. One vessel has successfully passed inspection in Turkey, en-route to Lebanon. The continued movement of vessels out of Ukraine ought to lead to a fall in prices. However, there are some key considerations which may limit any drop. These include;

- Volume of grain – the primary factor, which could prevent a sustained fall in prices is the volume of grain which needs to be moved. The grain deal only runs for 120 days, yet if reports are to be believed there is circa 20 million tonnes of old crop grain alone needing to be moved. That is around 170,000 tonnes of grain per day. There are a number of vessels waiting to leave Odessa, a key grain port, which will move with comparative ease, but this will not be the case for all of the grain.

- Logistics – logistical challenges are likely to restrict the volume of grain that can be shipped. Contrary to some reports, the volume of grain needing to be exported is not held at ports, or in a single province. It needs to be moved from within Ukraine to ports before it can be shipped.

- Insurance and crew – one of the primary concerns surrounding the ability to ship grain was the insurance premium on vessels although, given grain is now moving, this would not appear to be to prohibitive. Crewing the vessels may be another challenge, each vessel needs 20+ crew.

- Russia – the big caveat to all shipments at the moment is Russia’s intentions. The day after the deal was signed, it shelled the port of Odessa. This was followed a few days later by the killing of a prominent Ukrainian grain exporter in Mykolaiv. Similar incidents over the next 120 days will have as much impact on grain prices as the movement of vessels out of the Black Sea.

Shipments of grain out of Ukraine will ease prices, however, there still remains a lot of grain to be moved. The risk of Russia reneging on the shipment deal will also remain a concern. This will fundamentally limit the fall in prices. Furthermore, it is worth highlighting that there is still underlying support for grain prices with supply and demand of global grain tighter year-on-year. There is also continued uncertainty over the condition of the EU maize crop, due to heat stress, keeping prices supported.