New Crop

In terms of growing conditions, little could be more extreme than the temperatures recorded this month compared to last February. In the February 2018 bulletin we cited the ‘Beast from the East’ delaying drilling. This year, spring drilling is well ahead of normal with almost 25% of spring barley already in the ground. A word of warning though; early drilled spring crops are not always the highest yielding, and there is time yet for very cold weather. We reserve any judgement on harvest yield potential.

The USDA makes its first prediction of US wheat area every February, this year suggesting decreased plantings, in a falling area trend. Indeed, if correct, it would be smallest US wheat area for 110 years. This identifies the changing demands for grains, shifting to maize, for pig and poultry feed, biofuels and indeed even human food.

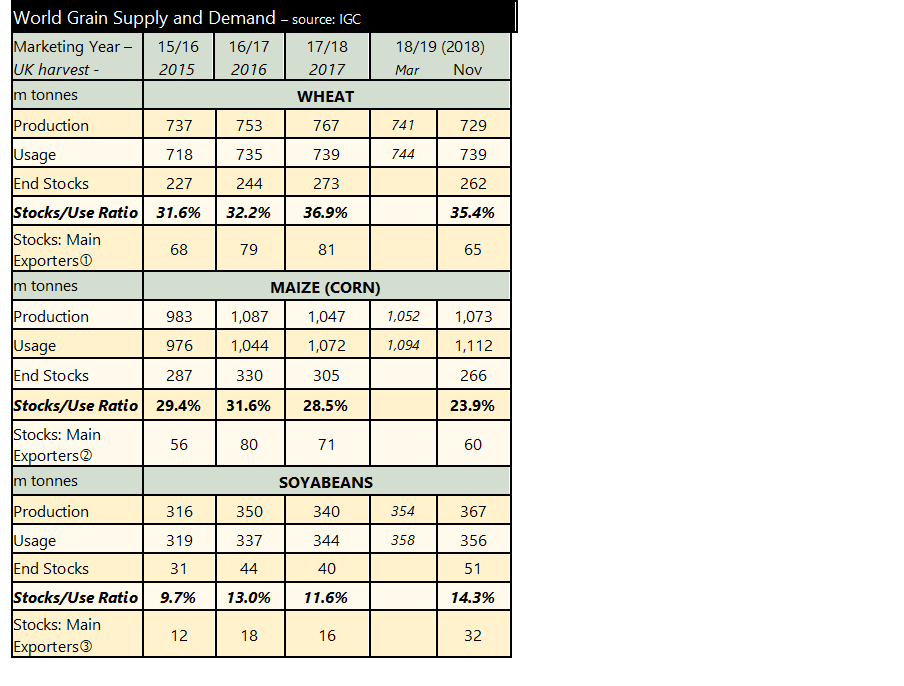

The International Grains Council’s first expectations of the forthcoming 2019/20 year are for a rise in global wheat production, of about 1%, a similar magnitude to the annual rise in demand so no substantial changes in year-end stocks. This seems to contradict the findings of the USDA, but theirs, of course is USA only. An increase in coarse grain harvests are also foreseen by the IGC, with maize and barley both up about 1%. This is in line with the rise in demand so is no more than trend demand. Much of the coarse grain increases are predicted to occur in the USA and China; the two biggest grain producers, so a small proportional change in these countries will be noticed. However, there are also rumours that China is considering rolling-out a major expansion to its bioethanol inclusion policy, which would have a considerable impact on feed grain demand in the coming few harvests.

Of course, much of these crops that have been forecast have not yet even been drilled; all maize, and soybeans are spring crops and Canadian, Russian and half of the US wheat is also spring varieties. Therefore, these projections are statistical analyses coupled with a smattering of planting intention data, not hard evidence of plants sprouting from the ground yet.

Old Crop

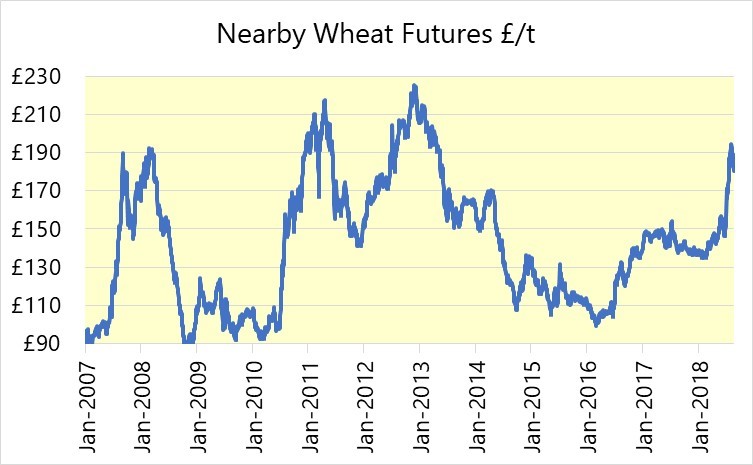

In the EU wheat market, a gradual decline in values this month (making European grain cheap compared with American grain) led to Europe and Russia winning some large export contracts to Saudi Arabia, boosting the export figures and balancing the supply and demand books.

The demand for ruminant feed is currently slipping away as cattle venture into the fields and sheep have grass to eat; leaving a lack of demand for feed barley, which has fallen to a £25 per tonne discount beneath feed wheat (which is primarily fed to housed chickens). Barley is being included at maximum rates in rations now for this reason.

Oilseed rape prices have taken a tumble, based on the arrival of a large vessel loaded with Canadian canola, and the reduction of the rapeseed crush volumes in the UK. This time of year is often difficult for European rapeseed (and pulses) as harvests from the Southern Hemisphere become available and start putting pressure in markets. The Old Crop pulse market is increasingly thin and new opportunities will become rarer now, despite a healthy premium over feed wheat for pulses.