At last the weather has turned out nice. The rain has stopped, at least for now, but certainly for long enough for many farmers from Oxfordshire to Newcastle to complete (and in some cases even start) their drilling. At the time of writing, many farmers are busily trying to get as much of their spring seed in the ground as possible. Seed merchants are reporting low availability of late drilled seeds like maize and spring beans as a result of high demand.

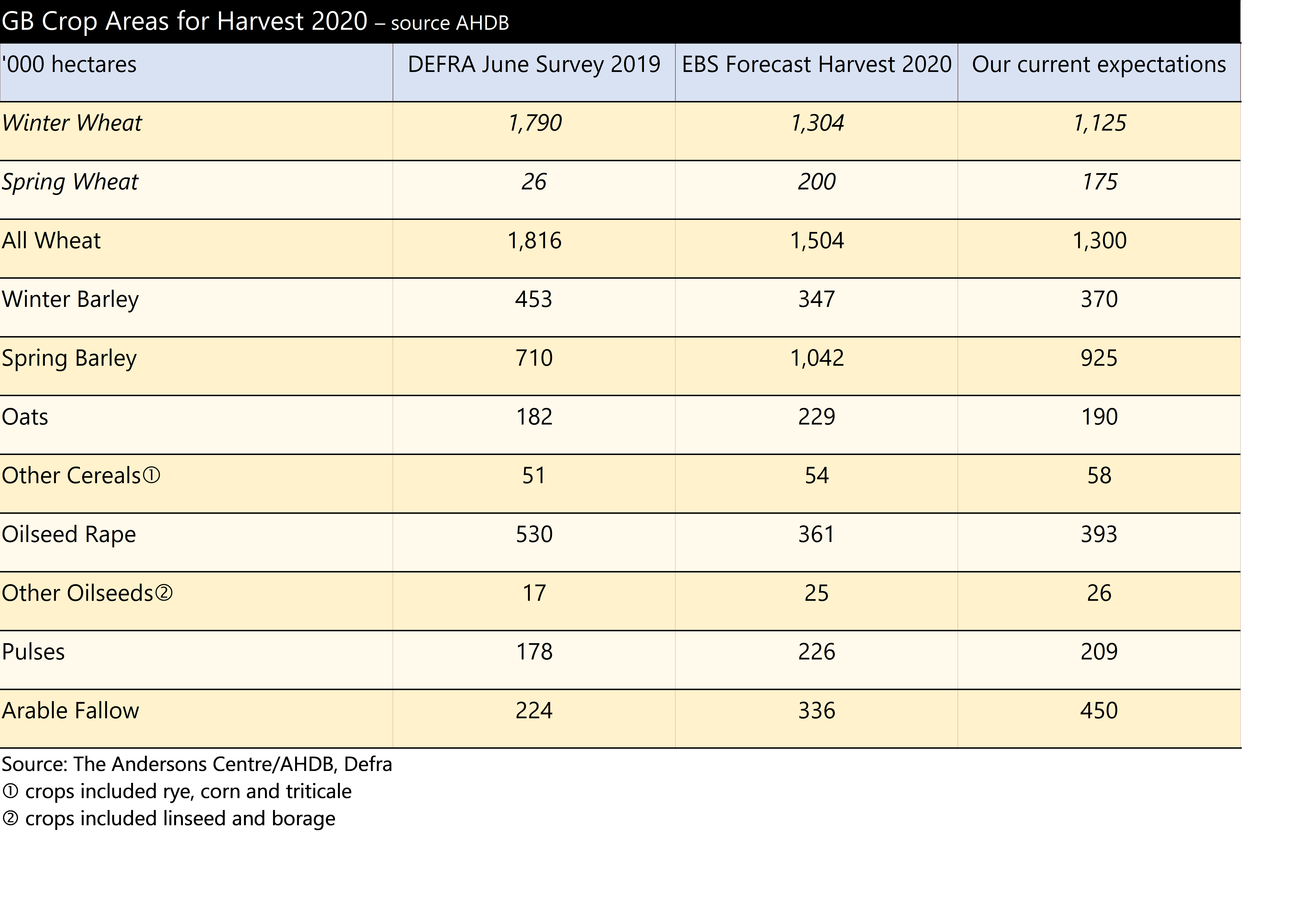

Last month we published an article commenting on the second Early Bird survey that we support AHDB with. This is the survey that assesses what has been planted and what growers intend to plant in the UK. It included planting intentions which, at the time, left opportunity for winter wheat to be planted. The rain did not stop in time for winter crops to be drilled and also may have curbed the spring drilling window for some growers leaving, we believe, a high chance of elevated fallow land and grass this year compared with normal. Our updated projections on crop areas look as follows:

If this projection is correct, it would leave potentially the lowest wheat area planted in the UK since 1978/79, and the highest spring barley area since 1987/88. Some projections expect spring barley to exceed 1 million hectares but we are not convinced there is enough time for that to occur. Oilseed rape area might end up being the lowest since 1988/89. Even so, it still might be the highest we see again because the difficulties of growing the crop this year have been only partly because of the rain, and partly because of the flea beetle. The fallow land area we have suggested here would be the highest level since set aside was mandatory back in 2007. For 2020 autumn drilling and the 2021 harvest, we would expect a high proportion of farmers very keen to capitalise on the first wheat opportunity, possibly planting a little earlier than this year too. Hold tight for a big wheat crop next year.

If this projection is correct, it would leave potentially the lowest wheat area planted in the UK since 1978/79, and the highest spring barley area since 1987/88. Some projections expect spring barley to exceed 1 million hectares but we are not convinced there is enough time for that to occur. Oilseed rape area might end up being the lowest since 1988/89. Even so, it still might be the highest we see again because the difficulties of growing the crop this year have been only partly because of the rain, and partly because of the flea beetle. The fallow land area we have suggested here would be the highest level since set aside was mandatory back in 2007. For 2020 autumn drilling and the 2021 harvest, we would expect a high proportion of farmers very keen to capitalise on the first wheat opportunity, possibly planting a little earlier than this year too. Hold tight for a big wheat crop next year.