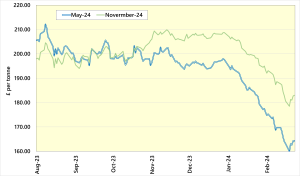

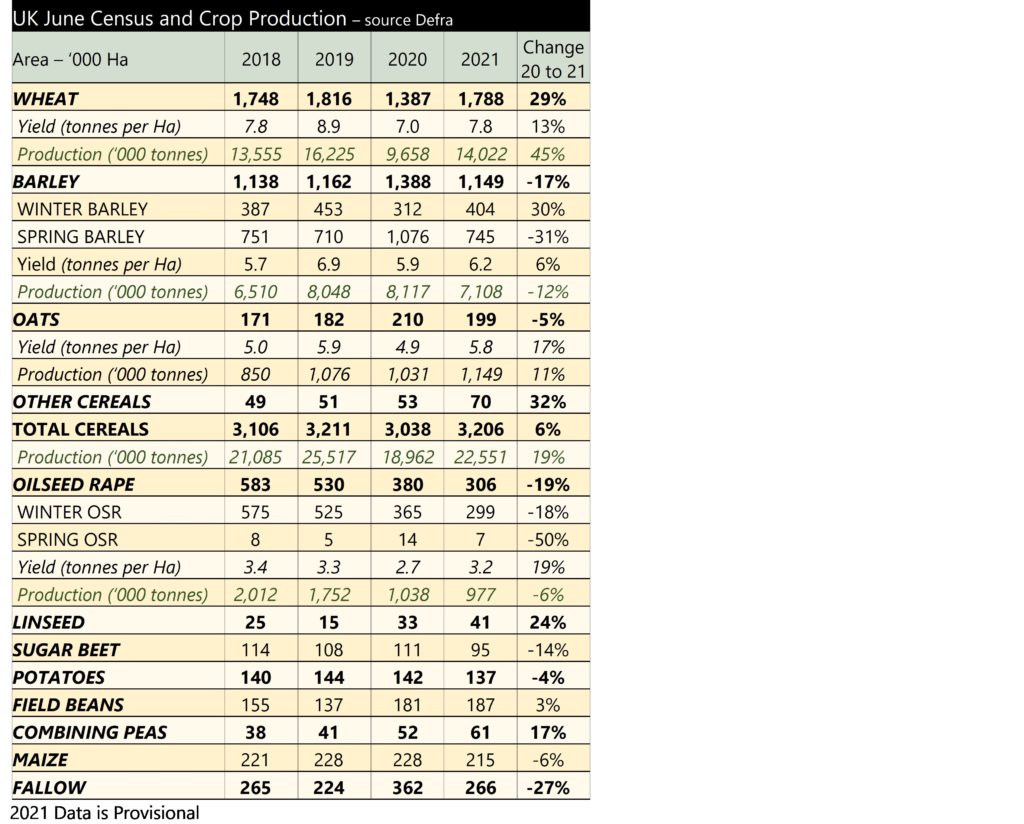

UK wheat prices were largely stable through January. This is despite further tightening of the global grain supply and demand and rising maize prices.

The chart shows the latest figures from the International Grains Council (IGC). The latest figures relate the the previous, 2024 harvest. The IGC produces its first current-year estimates in March.

US maize prices have been rising following a further tightening of the global grain balance sheet. As can be seen, production has been cut whilst the consumption forecast has risen. End stocks are set to be the lowest for some years. These figures are supported by the United States Department of Agriculture’s forecasts which have output and stocks reducing by 7 and 5 million tonnes, respectively.

Attention will now turn to the South American maize and soyabean crops. There has been some concern about excess rainfall in Brazil which could hamper planting of the second maize crop. The second maize crop accounts for 75% of Brazilian maize production and is planted in February and March. However, the outlook now looks like rainfall in Brazil will be at normal levels. Production forecasts point to record Brazilian maize production at 120 million tonnes. For Argentina, dry conditions are a concern, but production forecasts again remain high. Increased concerns for the Brazilian maize crop or changes to Argentinian forecasts could see prices increase and provide short-term selling opportunities.

Despite rising maize prices, which underpin feed markets, UK wheat prices, while up on December, have remained largely flat through January. One of the drivers for this is the strong import programme of grain in 2024. Data available from HMRC, from July to November 2024, shows 2.6 million tonnes of combined wheat and maize imports. These imports are keeping a lid on domestic values.

UK oilseed prices have been supported by a tight UK market. Ex-farm oilseed rape in January averaged the highest monthly price since February 2023, at £430 per tonne. There has been growing concern about the decline of rapeseed area in the UK, with an ‘OSR reboot’ campaign, led by United Oilseeds looking to help the area recover.

While UK grain prices remain stable, the cost of fertiliser has been rising heavily through January. Reports of a tightness in UK and European nitrogen supplies have resulted in increases in the price of ammonium nitrate and urea of around £20-30 per tonne. Adding to the challenge, offers are being withdrawn quickly, making it hard to gauge the price of fertiliser on any given day.