Tag: Oilseeds

Combinable Crops Roundup

Old crop grain and oilseed markets tumbled through March. There is a compounding set of factors behind this, including good planting progress in South America, improved weather in key growing regions, lacklustre domestic demand, and tariffs on Canadian canola (rapeseed) products.

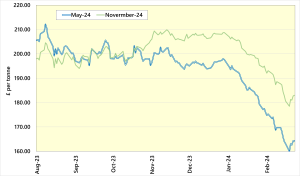

The most liquid old crop UK feed wheat futures contract (May-25) reached a contract low in March at £172 per tonne. Domestically, the strong import campaign this year is going to result in an increase in stocks year-on-year. This is despite a 20% reduction in wheat production in 2024 compared to 2023. Milling wheat premiums have been eroded by the strong import levels. Milling wheat premiums have fallen to just £20 per tonne, compared with £60 per tonne post-harvest.

There is currently a £20 per tonne carry from old crop (May-25) to new crop (Nov-25) futures. With crops reportedly coming out of winter in good condition, with limited disease levels, this premium could come under pressure.

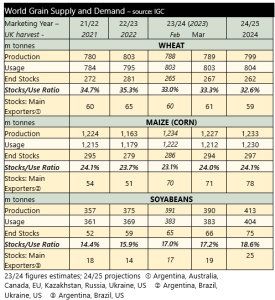

The International Grains Council (IGC) published its first projections of supply and demand for the 2025/26 season on 20th March. It forecasts that wheat carryover stocks will fall by six million tonnes year-on-year, despite an eight million tonne increase in wheat production. For the wider grains complex, a forecast 52 million tonne increase in maize production leads to a one million tonne increase in total grain stocks. The increase in stocks is further underpinned by an eleven million tonne increase in major exporter stocks. This will put pressure on maize prices which is the main cereal crop in terms of global output. There is still a long way to go until the 2025 crops are harvested so there is time for prices to move in either direction depending on crop progress and conditions.

For oilseeds, soyabean stocks are expected to rise marginally, year-on-year (up one million tonnes). However, prices have been undermined by the ongoing ‘trade war’. Following a drawn-out anti-dumping investigation, China has placed 100% tariffs on Canadian canola (rapeseed) oil and meal. Since the beginning of March, the value of Paris rapeseed futures (Nov-25) has fallen considerably. From 3rd to 17th March the value of the contract fell by €40 per tonne (reaching €460 per tonne). Prices have since recovered to €475 per tonne.

Currency is another important watchpoint for the UK market. Sterling has moved stronger against the Dollar. This reduces UK grain prices relative to global markets. However, it also makes imported inputs cheaper. Movements against the Euro have been mixed although the Pound is currently weaker than at the start of the year (supportive of rapeseed prices in the UK).

Grain Market Update

Old crop UK feed wheat futures prices (May-25) declined through February. There has been little news to support prices for some time. Large opening stocks, high levels of imports and subdued demand will mean the current trend likely continues. The large import levels of milling wheat in particular have reduced the milling wheat premium from an early season peak of £60 per tonne to around £25 now.

Whilst old crop prices have fallen, new crop prices (Nov-25) have increased, driven by rising global grain markets. US maize futures in particular have increased considerably in recent months. Speculative traders (managed money funds) have bought considerable volumes of maize futures, elevating prices. The weather outlook for maize production in both North and South America had been in question, including excess rainfall in Brazil. In the main maize producing region of Mato Grosso, planting of maize is more than eight percentage points behind the five-year average. However, the forecast is for improved weather.

The US weather has also been a key focus. Key wheat producing states in the US have been on the receiving end of temperatures as much as 15C below normal for February. However, this picture is also improving. Additionally, the current market price dynamics for maize and soyabeans in the US is expected to drive an increase in maize planting for 2025. The price gap between old and new crop could close quickly if the funds started selling.

In the short term, there has been support for UK feed barley prices with export demand driving selling opportunities. This has been much-needed owing to the surplus of out-of-specification malting barley adding to the feed heap from harvest 2024.

One positive aspect for arable markets is the strength of the oilseed rape price. That said, the crop area has declined significantly in recent years meaning the price support will only the minority of cereals farmers still growing the crop. In addition, the positive price movement in oilseed rape may not be enough to tempt nervous growers of the crop for 2025 harvest to sell.

A final point worth noting is the direction of fertiliser prices. Natural gas prices, a key input in the production of ammonium nitrate, hit the highest point since October 2023 in February. Prices have fallen back, but remain almost twice as high as the same point last year. So far we have seen an increase in nitrogen prices in the UK market in 2025, but not to the same level as has been observed on the Continent.

Grain Market Update

UK wheat prices were largely stable through January. This is despite further tightening of the global grain supply and demand and rising maize prices.

The chart shows the latest figures from the International Grains Council (IGC). The latest figures relate the the previous, 2024 harvest. The IGC produces its first current-year estimates in March.

US maize prices have been rising following a further tightening of the global grain balance sheet. As can be seen, production has been cut whilst the consumption forecast has risen. End stocks are set to be the lowest for some years. These figures are supported by the United States Department of Agriculture’s forecasts which have output and stocks reducing by 7 and 5 million tonnes, respectively.

Attention will now turn to the South American maize and soyabean crops. There has been some concern about excess rainfall in Brazil which could hamper planting of the second maize crop. The second maize crop accounts for 75% of Brazilian maize production and is planted in February and March. However, the outlook now looks like rainfall in Brazil will be at normal levels. Production forecasts point to record Brazilian maize production at 120 million tonnes. For Argentina, dry conditions are a concern, but production forecasts again remain high. Increased concerns for the Brazilian maize crop or changes to Argentinian forecasts could see prices increase and provide short-term selling opportunities.

Despite rising maize prices, which underpin feed markets, UK wheat prices, while up on December, have remained largely flat through January. One of the drivers for this is the strong import programme of grain in 2024. Data available from HMRC, from July to November 2024, shows 2.6 million tonnes of combined wheat and maize imports. These imports are keeping a lid on domestic values.

UK oilseed prices have been supported by a tight UK market. Ex-farm oilseed rape in January averaged the highest monthly price since February 2023, at £430 per tonne. There has been growing concern about the decline of rapeseed area in the UK, with an ‘OSR reboot’ campaign, led by United Oilseeds looking to help the area recover.

While UK grain prices remain stable, the cost of fertiliser has been rising heavily through January. Reports of a tightness in UK and European nitrogen supplies have resulted in increases in the price of ammonium nitrate and urea of around £20-30 per tonne. Adding to the challenge, offers are being withdrawn quickly, making it hard to gauge the price of fertiliser on any given day.

Grain Markets

Grain prices have fallen as harvest has commenced in the UK. Many in the East and South East of England are progressing well with winter barley and oilseed rape harvests; early results have been varied, reflecting the picture of crops throughout this season. That said, overall, early yields are perhaps not as disappointing as feared.

Grain prices have declined due to plentiful global supplies. In its July update to the World Agriculture Supply and Demand Estimates, the USDA increased global grain stock forecasts for the 2024/25 season by 6 million tonnes. The increase was largely driven by an almost 5 million tonne increase in expectations of global wheat stocks.

Harvests also are well underway in much of the Northern Hemisphere, with harvest completion ahead of normal in the US. In France, progress is slightly behind the five-year average pace, and results have reportedly been disappointing. That said, with expectations for harvests already low, it takes further reductions in reported yields to increase prices.

In the UK, AHDB published its annual Planting and Variety Survey results. The results show year-on-year declines in wheat area (-9%, UK) and oilseed rape (-21%, GB). The total barley area is estimated to have increased by 6%, owing to increases in spring barley plantings. It is notable that the results show a smaller decline in wheat area than was forecast in the spring re-run of the Early Bird Survey. The Early Bird forecast a wheat area decline of 15%.

AHDB suggest that less wheat was replaced by spring cropping than the Early Bird Survey indicated. However, it is notable that the sample size of the Planting and Variety Survey is smaller than that of the re-run Early Bird Survey. One thing the difference between the results does draw into question is the reliability of surveys, and how individual farmers record data. Have farmers entered the area of the fields which were cropped which will be reflected by lower average yields? Or, have farmers subtracted lost/ poor areas from planting figures, which would be reflected by better-than-expected yields? Defra June survey area data will be published in late August.

Whilst UK ex-farm grain prices have fallen, on average, across the month, oilseed rape prices have increased. It remains to be seen whether the better price will encourage more oilseed rape planting this autumn. More details on cereal and oilseed prices can be seen in Key Farm Facts.

Grain Markets

Prices for feed grains have fallen considerably throughout June, pressured by improved global conditions. The value of UK feed wheat futures (Nov-24), averaged over £217 per tonne in May, but just £205 per tonne in the month to 26th June. The decline in UK futures prices is the result of falling global prices. New crop (Dec-24) US wheat futures fell consistently during June, towards the contract low, set in March 2024.

The US wheat harvest is progressing well, and the increased liquidity of global grain has put downwards pressure on prices. In addition, the harvest of Brazil’s second and largest (Safrinha) maize crop is adding to the volume of available grain. The increased availability of grain has so far outweighed the fact that global grain stocks-to-use ratios are set to be tighter year-on-year; posting an eighth consecutive annual decline.

The months immediately before harvest are often some of the most volatile and reactive to weather and harvest progress stories. For prices to rise, almost continual negative stories are needed. There are some events that could offer support to grain prices. If they materialise there may be opportunities to gain on short term market rallies.

There has been excess heat and rainfall across the US corn belt. This has led to flooding in some key grain producing regions, most notably Minnesota. However, assessments of the US maize crop remain largely positive, although these assessments do not fully capture recent negative weather. One watch point for grain markets is the US acreage survey. The survey will be published on Friday 29th June, giving the clearest indication yet of the scale of the US maize and soyabean crops.

Another area of concern had been Russian wheat crops, which were hit by unfavourable weather in April and May. Whilst early information points to good yields, this is based on a small proportion of the harvest. Russian analytical firm SovEcon point to the potential for yields to come down as harvest progresses.

As mentioned, the value of UK grain has followed the global market lower, for both old and new crop. At the same time, the value of UK milling wheat over feed wheat has grown, averaging £68 per tonne, ex-farm in June. The value of pulses have also increased, with little availability of old crop, and some time before new crop is available. That said there is also little to no demand at present. Domestic cereal, oilseed and pulse prices can be seen in Key Farm Facts.

Oilseed rape continues to look attractive for planting this autumn. Dependent on available moisture, many will be anxious to drill early following the wet 2023-24 season. Provided soil moisture is sufficient prices approaching £400 including bonuses will be attractive. Of course, much will also depend on pest pressure.

Global Grain Update

Global grain prices have been falling for much of 2024. The main driver of the decline has been ample supplies of grain anticipated to come from South America. Maize and soyabeans in Argentina and Brazil are still developing, making prices volatile in response to weather conditions. Concerns over excess rainfall in the region prompted some fund managers to cover some of their record sold positions, supporting prices in the third week of March. The role of fund managers in Chicago grain and oilseed futures markets is important for the direction of global prices. If weather conditions turn, or other funds become more or less attractive the price of grain can move quickly.

With regard to supply and demand, the International Grains Council (IGC) published its latest update for the 2023/24 season, on the 14th March. Furthermore, the IGC also published its first forecasts for 2024/25. These are shown below.

Despite cuts to global grain production in the Southern Hemisphere for the 2023/24 season, there is a greater fall in estimated consumption, resulting from reductions in feed use. As a result global stocks are forecast to increase by 10 million tonnes.

For 2024/25, the global grain and soyabean stocks are due to rise again. Whilst an increase in stocks is likely to move prices lower, the year-on-year rise is fairly small. We are still some months away from the Northern Hemisphere harvest, and it would not take a big reduction in production (forecast or actual) to move global prices higher.

For the 2024/25 season, total grains production is forecast to rise by 28 million tonnes, 10 million tonnes of that rise is wheat. Increases in wheat production are projected for Argentina, Australia, Canada and the USA. Production is expected to fall in the EU, and the Black Sea. However, usage of wheat is set to remain high and global stocks are forecast to fall by 5 million tonnes between 2023/24 and 2024/25. This may provide some specific support to wheat prices.

Arable Roundup

Grain prices fell considerably during February. The May-24 UK Feed Wheat Futures contract started the Month at £175 per tonne, as of 24th February the same contract was worth £164 per tonne. It is a similar story for the 2024 crop, with November-24 Futures £9 per tonne lower on the month.

The direction of the UK market is driven by the availability of global grains. Concern had been building about dry conditions in South America hindering planting progress. However, both Brazil and Argentina have received rainfall and planting of maize and soyabeans has progressed. Argentina is forecast to harvest an additional 22.5 million tonnes of maize in 2023/24 compared to 2022/23 (when it was affected by a widespread drought). Brazilian grain and oilseed production forecast have fallen. However, the country is still expected to harvest a combined 300 million tonnes of cereals and oilseeds; the second largest harvest on record.

Furthermore, grain prices are weighed down by cheap Black Sea wheat, slow US grain and oilseed exports, and the large sold position held by speculative traders in US grain futures.

Looking ahead to the 2024 UK harvest, the window of opportunity for further winter wheat plantings, prior to latest safe sowing dates, is closing. Heavier ground is still sodden, especially across the East Midlands. Crops on lighter land look far better. UK growers face the prospect of smaller crops being sold at lower prices. The poor outlook for the 2024 harvest is increasingly accounted for in grain prices. Looking at the gap between old crop and new crop wheat futures (May-24 versus November-24), the new crop is worth almost £19 per tonne more that the old crop. This time last year the November crop (November-23) was worth just £3 per tonne more than the old crop (May-23).

UK Feed Wheat Futures Chart

Source: AHDB

Farmgate grain prices have reflected the wider trend in futures, as shown in Key Farm Facts. The UK still has ample old crop wheat and barley stocks, with prices uncompetitive into export markets.