Prices for UK arable crops have fallen lately, pressured by global supply and demand. On 9th December, the USDA released its latest supply and demand estimates. The estimates increased the stock picture for both wheat and coarse grains, leaving the global market looking better supplied than a month ago.

A month ago, the slow progress in Australia due to recent rains had caused delays to harvest and exports, increasing prices. However, harvest progress has improved with drier weather, and while exports will still take time to catch up, prices have fallen in response. Beyond the improved situation in Australia, the next key event for grain markets will be South American maize production. The crop is expected to be big, adding to the fall in prices, but with an active La Niña (which brings dry weather in South America), the crop reports need watching closely.

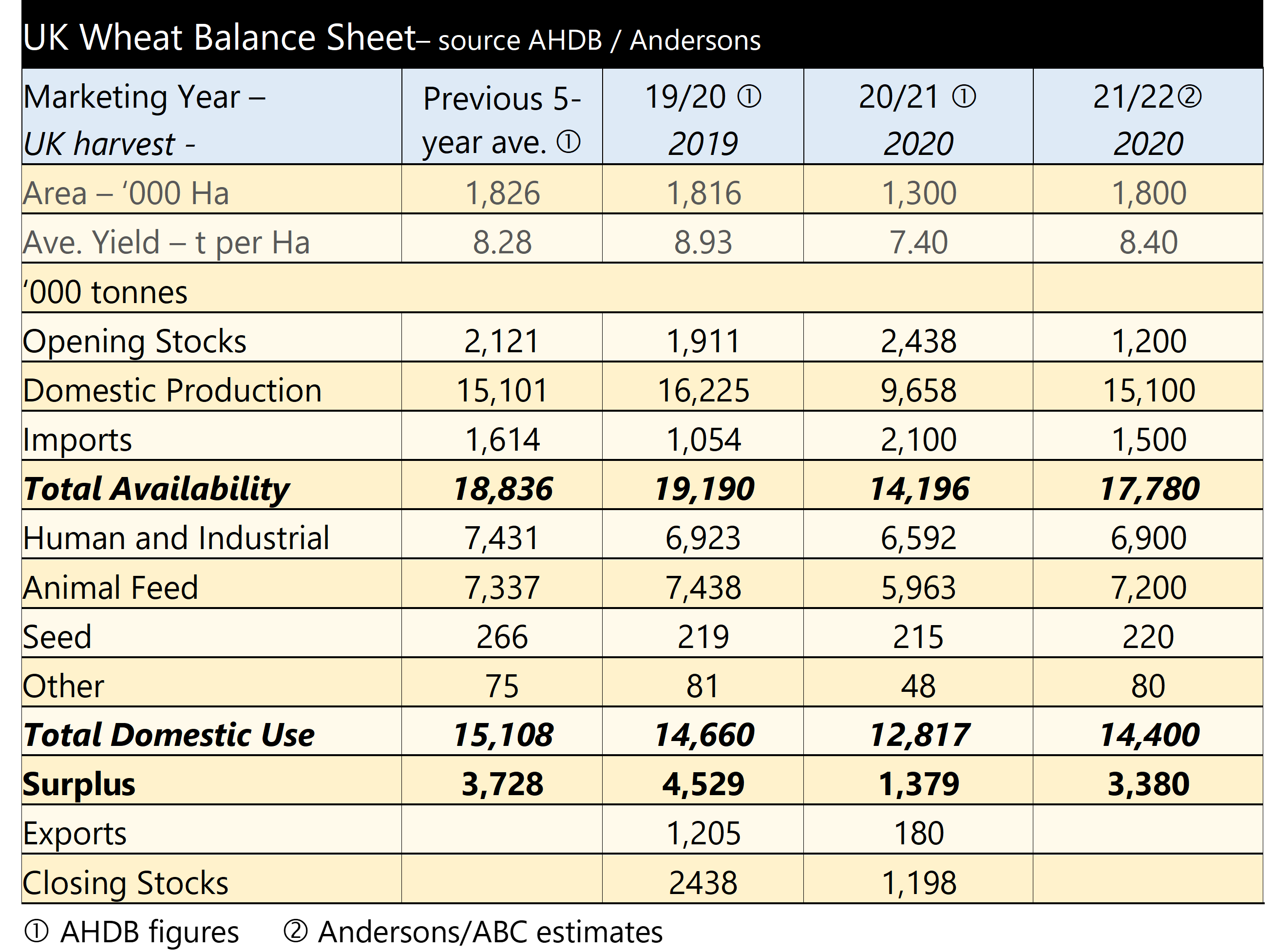

Domestically, we are seeing the price effects of global supply and demand. The price of UK wheat while initially moving up through early December, has now fallen. New crop wheat futures (November 2022), closed on 16th December 2021, at £195.65 per tonne. Whilst down from the highs we’ve seen of late, this still represents good value in historic terms, and is mitigating some of the increase in input costs.

Ex-farm value, published by AHDB, lag the futures market, and as such, continue to show strength in the most recent publication (price to 9 December). However, they do show that milling wheat premiums have remained strong. In the week ending 9th December, ex-farm milling wheat was over £50 per tonne more than feed wheat.

Barley prices in the UK are also high, in historic terms. The barley market is tight this year in the UK. Through the early part of the season barley remained a popular choice in animal feed rations. This has narrowed the gap between wheat and barley.

Oilseed prices have also fallen over the last month. Domestic oilseed rape prices for old and new crop delivery have followed the direction of Paris rapeseed futures. Oilseed rape (and rapeseed oil) prices had attracted a large premium over other oilseeds. This premium has destroyed some demand and pulled prices down. This is likely to continue, especially with Australia harvesting a record canola (rapeseed) crop.

Pulse markets have bucked the trend of other arable commodities. The price of feed beans has remained relatively flat. Trade has reportedly been ‘good’ in feed beans, but there are signs that demand may be dwindling.