The results of the annual Early Bird Survey of UK planted intentions show a 13% rise in rapeseed area for harvest 2022, at 345,000 hectares. The increase is not surprising given how firm rapeseed prices are. But, the fact the increase is not greater, reflects the large increases in rapeseed prices since mid-September. This is after most planting has been completed.

The area of arable fallow is also seen increasing year-on-year. This is a possible reflection of the surging cost of inputs this season, which will challenge many margins. With high nitrogen costs we may have expected to see an increase in the area planted to leguminous crops. However, this is not the case, and the area planted to pulses is forecast to fall by 5%. As with OSR, this is likely driven by the timing of price rises.

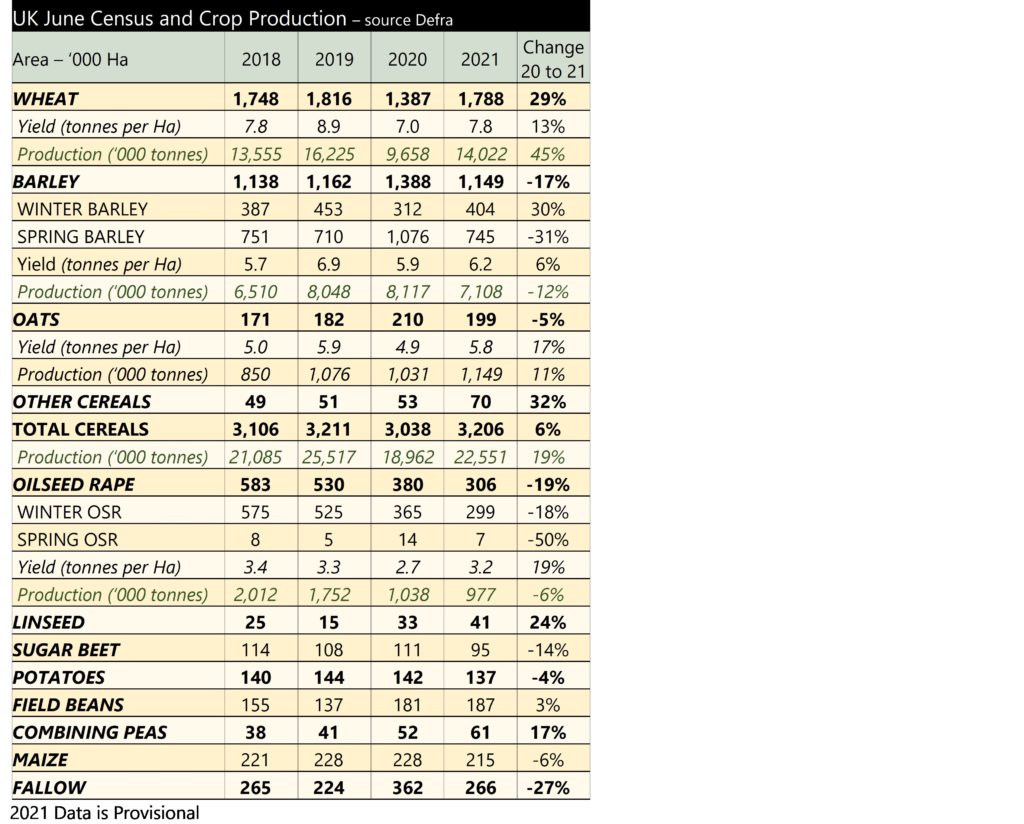

Unsurprisingly, wheat remains a firm feature in the rotation. The area planted to the crop is set to rise for the second year in a row, following the disastrous 2020 harvest. The area is seen rising to 1.81 million hectares. This is slightly down on the 1.82 million hectare crop for 2019. This will go further to easing the tight domestic market we have now, following the 2020 crop.

With a rise in the area planted to wheat and OSR, barley and oats look set to lose out. The total area intended to be planted to barley is down 4% at 1.10 million hectares year-on-year. Area is also seen down 101 thousand hectares on the five-year average. With grain prices firm it is arguably no surprise that spring acreage is down 8%, whilst winter area is seen up 4%.

If the intended area planted to barley is realised, then we could see the narrow discount of barley to wheat continue. The barley market is tight at present in the UK, and a reduced acreage would do little to replenish stocks.

It is worth highlighting at this stage these figures represent intentions, rather than confirmed plantings. Spring acreages are still very much open to change, dependent on the price of both outputs and inputs (especially this season).