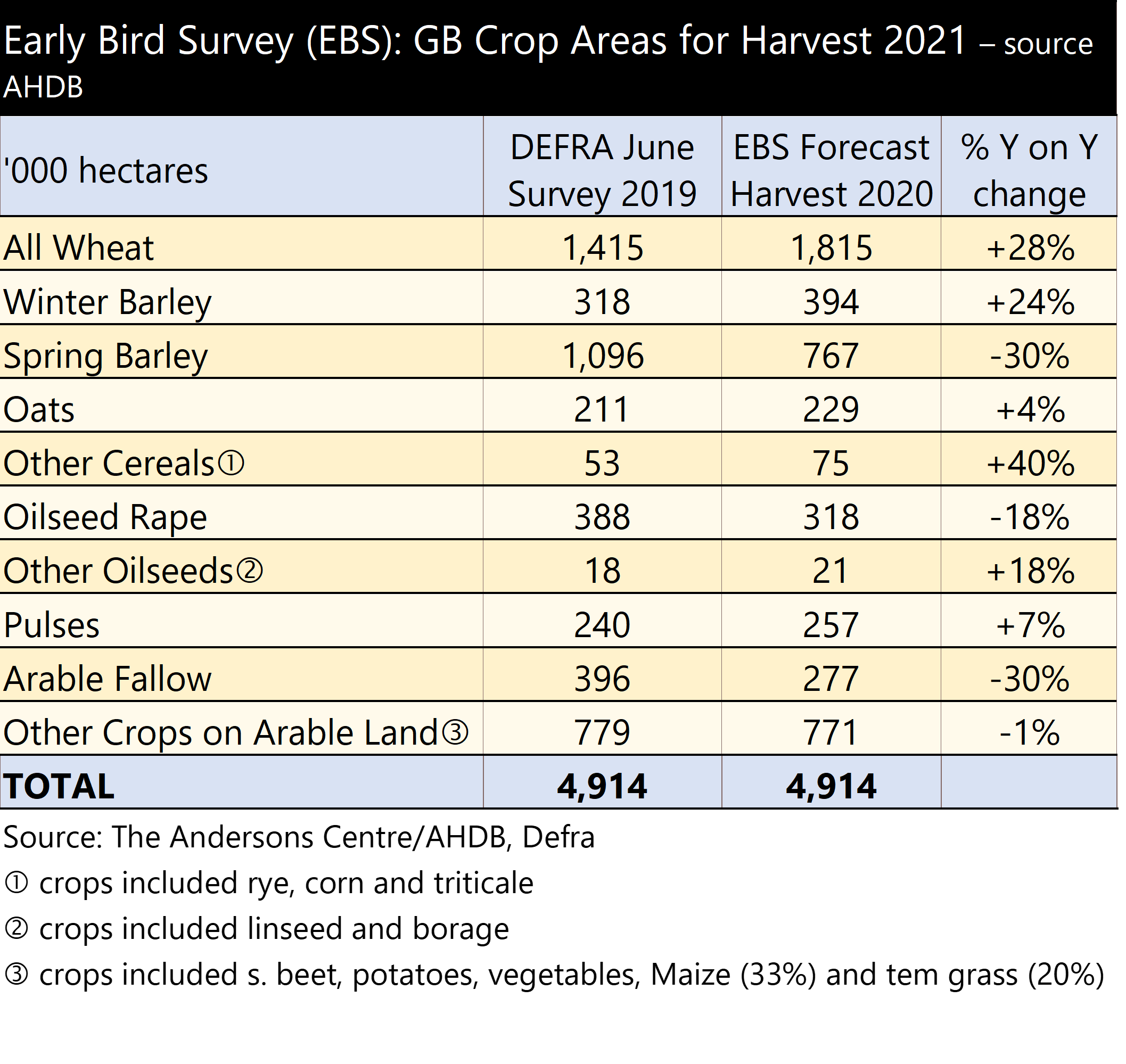

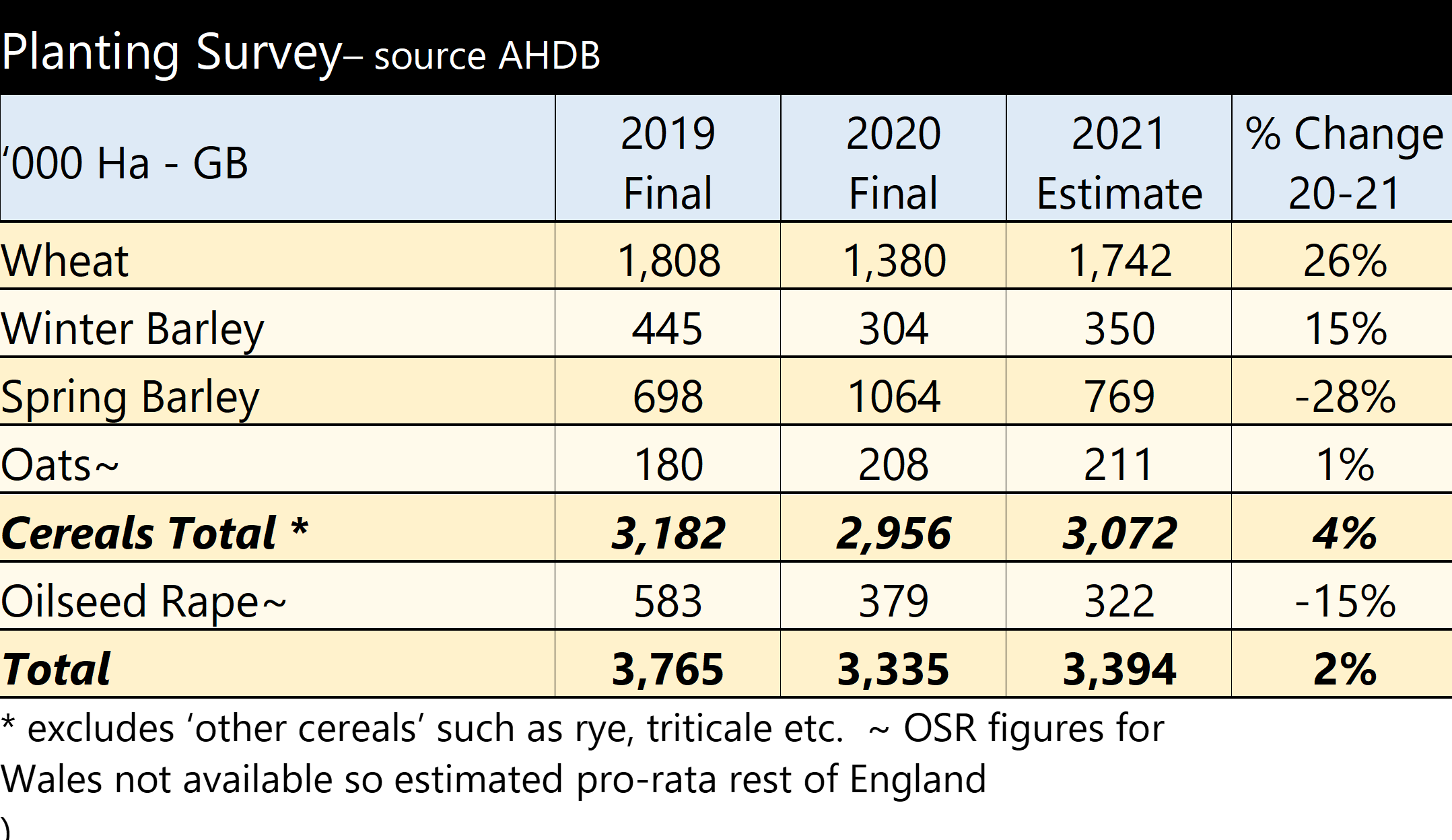

The far better establishment conditions for the 2021 crop compared with the atrocious weather for 2020 harvest has resulted in a huge swing to cropping, largely back to more ‘normal’ levels. For oilseed rape, the loss of confidence in growing the crop largely because of the mostly uncontrollable pressure from cabbage stem flea beetle (CSFB) has meant the harvested area has dropped to its lowest for over 30 years.

According to the AHDB’s 2021 Planting and Variety Survey, GB winter wheat plantings have recorded a year-on-year rise of 26% to 1,742 thousand hectares. Every region recorded a rise in plantings, the most significant being in the East Midlands (+47%) and West Midlands (+42%). Nabim Group 1 and 2 varieties made up 44% of the area in 2020 compared with 41% last year and 36% in 2019, showing a rising proportion of milling wheat being grown.

The total GB barley cropped area has recorded a 18% year-on-year fall to 1,119K hectares as growers ‘correct’ their rotations from their enforced spring cropping regime last season. The winter barley area (not surprisingly) rose 15% to 350K hectares, with again the East Midlands recording the most significant rise of 88% with the South West showing the next largest rise of 35%. As a consequence, spring barley plantings have inevitably recorded a 28% fall on the year to 769K hectares; still quite high compared with the years before 2020, demonstrating the gradual increase in spring cropping we are seeing in the UK. According to the AHDB, 58% of the GB barley area is malting barley varieties; last year it was 75% and 56% in 2019.

The area of oats has risen by 1%, with an 18% rise in Scotland, and 2% fall in England and Wales with big swings in some regions (down 22% in the East Midlands and up 28% in the East).

The awful growing year in 2019/20 for oilseed rape, because of both the weather but also worst infestation so far of CSFB, clearly put a large number of growers off for this year. Ironically, the crop looks good and its harvest is starting. Yet, with a 21% fall of area in the East Midlands, 22% decline in the South West and 34% reduction in the East, the overall crop area has fallen 15% since even last year. This makes the cropped area the lowest since 1989 when including spring OSR. We expect those who stuck with it for this year will observe a good harvest and high gross margin so it may encourage a small resurgence of cropping for 2022.

The full AHDB Planting and Variety Survey can be found at https://ahdb.org.uk/planting-variety-survey