No two potato seasons are the same and that is certainly the case this year. A year ago growers were struggling to plant potatoes in wet and difficult conditions, with some not seeing an end to the planting season until June. This year conditions are much more favourable allowing growers to get onto fields and plant. Soon the cry may be for more water after one of the driest March’s for years.

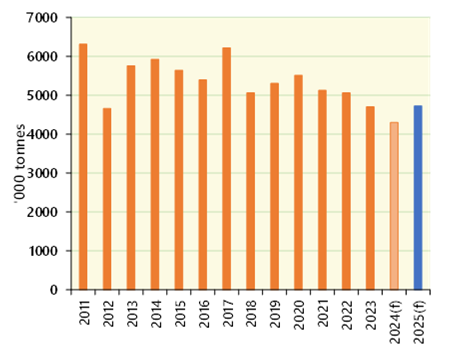

Despite improved field conditions, growers are unlikely to plant a large potato area. Last year the UK potato area was up a little on the all-time low of 98,000 hectares planted in 2023 to around 100,000 hectares – there are still no definitive Defra figures. A poor growing season meant that the total harvest was around 4.4 million tonnes – the smallest on record. This year, the favourable conditions and two years of much higher prices means growers will probably plant more. However, the area increase is not likely to be above 5%. Average five-year yields of 45 tonnes per Ha would deliver a 4.725 million tonne crop, which would not be much larger than the 2023 crop. It would be remarkable if production nears anything like five million tonnes – before that only weather-affected crops were below that volume – 1976, 1977 and 2012.

GB Potato Production – Source Defra/World Potato Markets

Prices have eased compared to last year, but they are still historically high. Newsletter Potato Call’s latest report puts Maris Piper prices for packing at up to £350 per tonne. A year ago some buyers were prepared to pay £600 per tonne for the best of the variety.

Whilst prices are lower this season, British growers have not been exposed to the same decline in values that has taken place over recent weeks in mainland Europe. Free-buy prices had reached as high as €300 per tonne for processing potatoes, but lower demand for processed and a spooked market has seen them drop to €175 per tonne in six weeks. Processors in Belgium asked growers to reduce their contracted areas for the 2025 crop, which did not go down well, but hinted at concern among the industry.

Fears of a trade war between processed potato trading nations such as the US, the EU and Canada have affected the market, as has the rise of other suppliers including India, China and Egypt who have seen sales jump by more than 40% over the last year. Lower potato prices in Europe make those stocks more attractive to importers into the British market, given the price difference between the two territories.