Old crop UK feed wheat futures prices (May-25) declined through February. There has been little news to support prices for some time. Large opening stocks, high levels of imports and subdued demand will mean the current trend likely continues. The large import levels of milling wheat in particular have reduced the milling wheat premium from an early season peak of £60 per tonne to around £25 now.

Whilst old crop prices have fallen, new crop prices (Nov-25) have increased, driven by rising global grain markets. US maize futures in particular have increased considerably in recent months. Speculative traders (managed money funds) have bought considerable volumes of maize futures, elevating prices. The weather outlook for maize production in both North and South America had been in question, including excess rainfall in Brazil. In the main maize producing region of Mato Grosso, planting of maize is more than eight percentage points behind the five-year average. However, the forecast is for improved weather.

The US weather has also been a key focus. Key wheat producing states in the US have been on the receiving end of temperatures as much as 15C below normal for February. However, this picture is also improving. Additionally, the current market price dynamics for maize and soyabeans in the US is expected to drive an increase in maize planting for 2025. The price gap between old and new crop could close quickly if the funds started selling.

In the short term, there has been support for UK feed barley prices with export demand driving selling opportunities. This has been much-needed owing to the surplus of out-of-specification malting barley adding to the feed heap from harvest 2024.

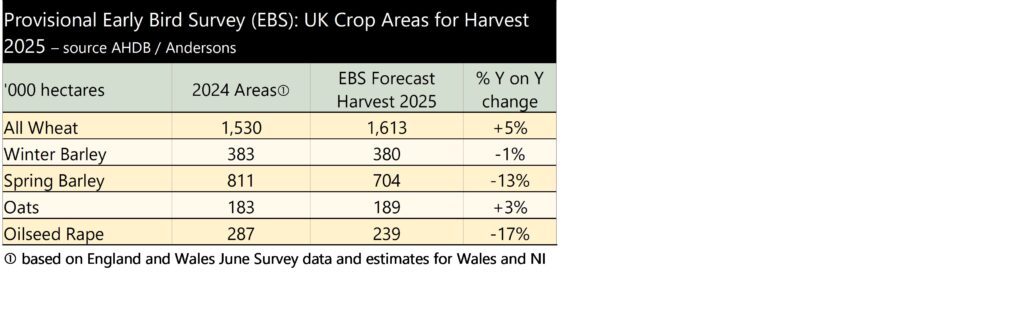

One positive aspect for arable markets is the strength of the oilseed rape price. That said, the crop area has declined significantly in recent years meaning the price support will only the minority of cereals farmers still growing the crop. In addition, the positive price movement in oilseed rape may not be enough to tempt nervous growers of the crop for 2025 harvest to sell.

A final point worth noting is the direction of fertiliser prices. Natural gas prices, a key input in the production of ammonium nitrate, hit the highest point since October 2023 in February. Prices have fallen back, but remain almost twice as high as the same point last year. So far we have seen an increase in nitrogen prices in the UK market in 2025, but not to the same level as has been observed on the Continent.