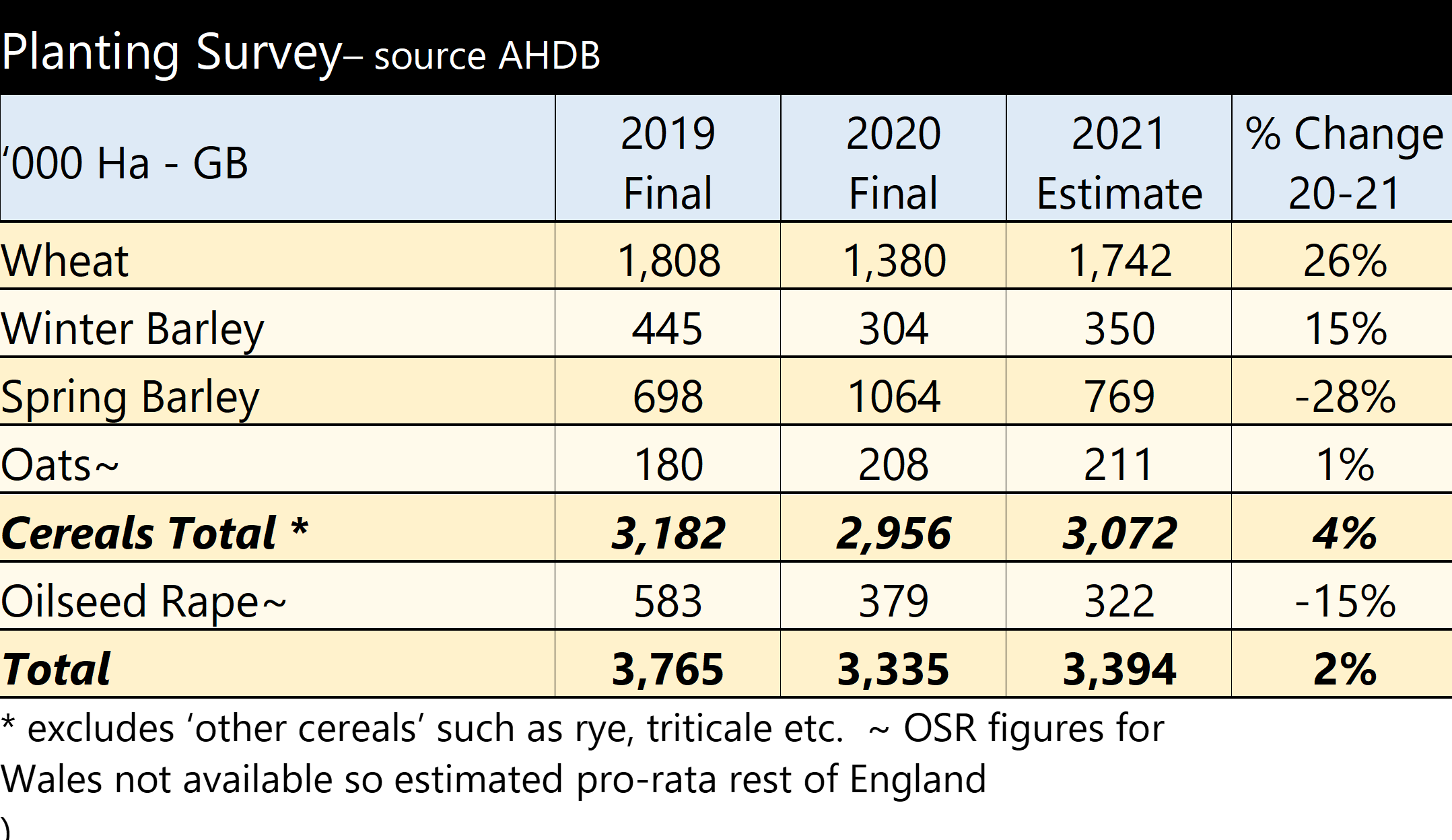

The area planted to wheat in the UK is expected to fall by 1.3% according to the results of the annual AHDB Early Bird Survey of UK planting intentions. The survey, conducted by The Andersons Centre with the support of the AICC and other agronomists, captures a snapshot in early November. This is a crucial caveat to the survey, in that it reflects the time before storms Babet, Ciarán and Debi.

Irrespective of the conditions of the storm, winter plantings were already expected to decline owing to the wet conditions which have persisted since harvest. The area planted to winter barley is expected to fall by 6%. Much of the fall in winter cropping will be replaced by spring barley (forecast up 13%) or oats (up 12%).

With prices having tumbled from their post-Ukraine invasion high, it is no surprise to also see the area intended to be planted to OSR falling by 16%. This will also include a proportion which has already been written off, with flea beetle and slugs enjoying the mild post-planting weather.

Time will tell as to whether all the wheat area intended is planted. Weather conditions between now and mid-January will be pivotal. In addition, close attention needs to be paid to the condition of crops in the ground (see accompanying article).

A further update, with regional detail will be produced in mid-December, once Defra publish a full UK crop area figure.

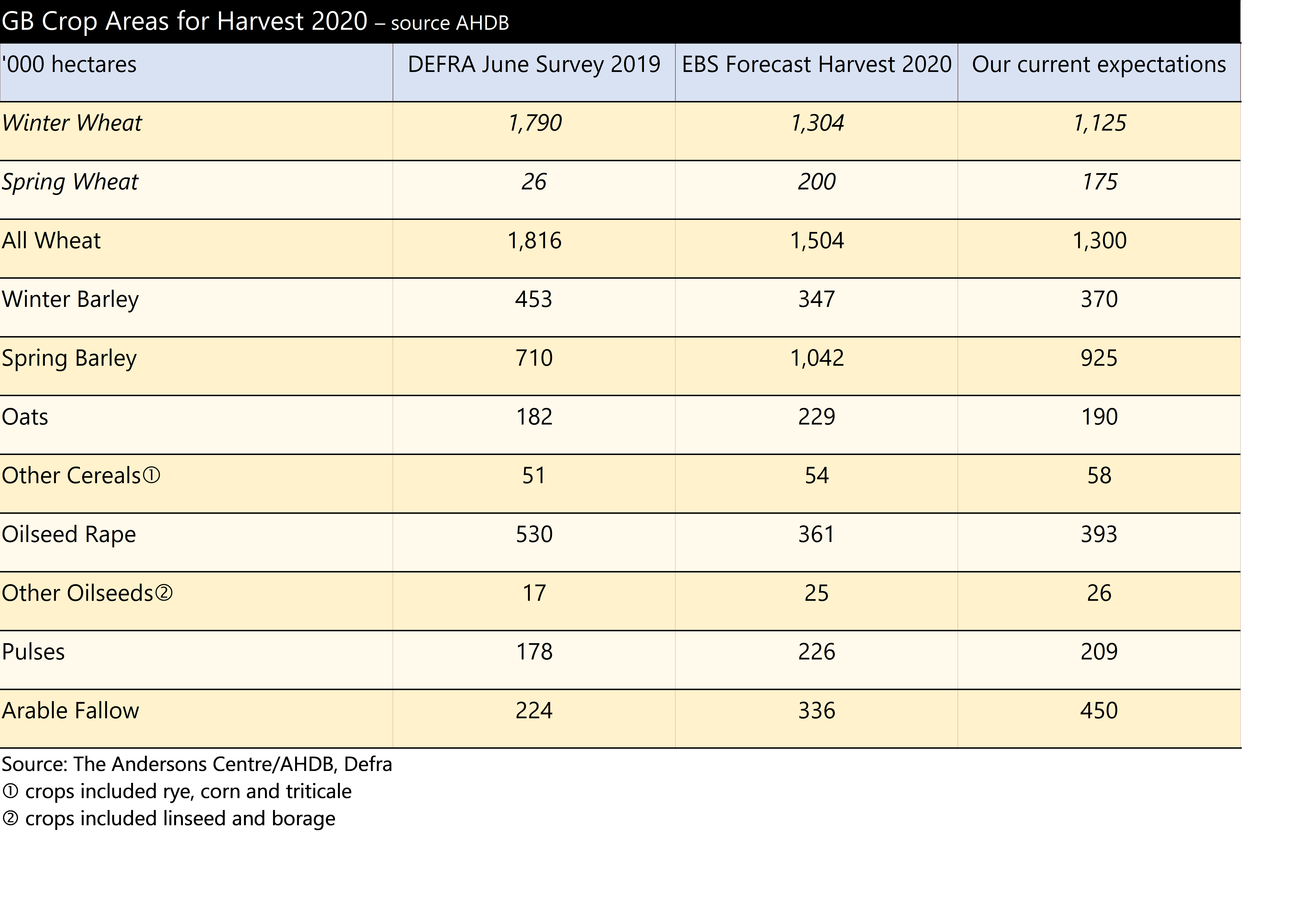

If this projection is correct, it would leave potentially the lowest wheat area planted in the UK since 1978/79, and the highest spring barley area since 1987/88. Some projections expect spring barley to exceed 1 million hectares but we are not convinced there is enough time for that to occur. Oilseed rape area might end up being the lowest since 1988/89. Even so, it still might be the highest we see again because the difficulties of growing the crop this year have been only partly because of the rain, and partly because of the flea beetle. The fallow land area we have suggested here would be the highest level since set aside was mandatory back in 2007. For 2020 autumn drilling and the 2021 harvest, we would expect a high proportion of farmers very keen to capitalise on the first wheat opportunity, possibly planting a little earlier than this year too. Hold tight for a big wheat crop next year.

If this projection is correct, it would leave potentially the lowest wheat area planted in the UK since 1978/79, and the highest spring barley area since 1987/88. Some projections expect spring barley to exceed 1 million hectares but we are not convinced there is enough time for that to occur. Oilseed rape area might end up being the lowest since 1988/89. Even so, it still might be the highest we see again because the difficulties of growing the crop this year have been only partly because of the rain, and partly because of the flea beetle. The fallow land area we have suggested here would be the highest level since set aside was mandatory back in 2007. For 2020 autumn drilling and the 2021 harvest, we would expect a high proportion of farmers very keen to capitalise on the first wheat opportunity, possibly planting a little earlier than this year too. Hold tight for a big wheat crop next year.