Beef and sheepmeat trade with the EU could plummet by over 90% under a ‘No Deal’ Brexit. This is one of the headline findings of a study recently published by the AHDB in collaboration with QMS and HCC. The report, complied by The Andersons Centre, looks at the impact of trade barriers on the UK beef and sheepmeat sector post-Brexit. It examined two scenarios; a Brexit Deal and a No Deal Brexit. Some of the main points include;

- Trade impact under a Brexit Deal scenario is relatively small: total exports would decline by about 1% in volume terms (imports 0.8% lower), driven by EU27 declines. Sheepmeat exports to EU27 are forecast to decline by 1.5% whilst corresponding imports would be 3% lower. These declines are chiefly due to Non-Tariffs Measures (NTMs) – i.e. the increased trade ‘friction once the UK was not part of the Single Market. There would be minimal changes to non-EU trade.

- Significant upheaval under No Deal: trade with the EU27 would plummet (by 92.5%) due to the imposition of tariffs, TRQs and higher impact of NTMs. Sheepmeat trade with the EU would be almost completely wiped out. Substantial declines in trade with the EU27 would also ensue for beef – exports down by 87%, imports declining by 92%. Somewhat better market access for beef compared to sheep, due to TRQs, would permit some UK-EU trade to continue. The introduction of a new 230Kt TRQ for UK beef imports would cause non-EU imports to soar by over 1,300%. This would lower prices and drive-up UK consumption by approximately 7%. Sheepmeat imports from non-EU countries are not anticipated to change whilst consumption is projected to rise by 14% due to declining prices.

- Price impacts: there would be small declines under a Brexit Deal scenario (-1 to -3% respectively). Under No Deal severe price declines would be seen. Sheepmeat is particularly exposed (projected 24% price fall under No Deal). Downward price pressure for beef (-4%) under No Deal arises due to competition from lower priced world-market imports. This would be exacerbated if significant volumes of Irish beef enter the UK barrier-free via NI.

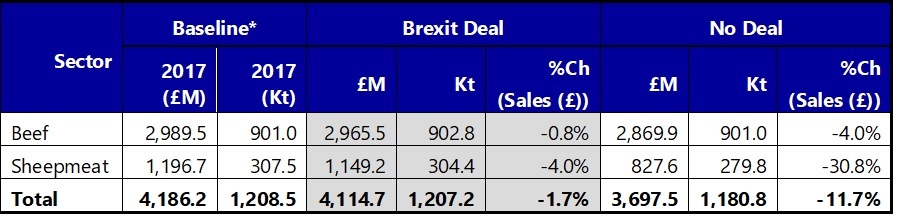

- Value of carcase meat output: under a Brexit Deal, output would decline by an estimated 1.7% whilst under a No Deal the decline would increase by nearly ten-fold (-11.7%) with sheepmeat output nearly 31% lower which would be devastating for incomes in the sector. Growth in exports to non-EU markets under No Deal would be insufficient to compensate for the loss of access to the EU27.

Projected Impact of Trade Barriers on Domestically-Produced Beef and Sheepmeat (Farm-Gate Level)

Sources: Defra (2019) and The Andersons Centre (2019) *Baseline Figures derived from Defra data.

- Similar Impacts at Farm Level: Andersons’ Meadow Farm model projects a 27% decline in profitability (£68 per Ha versus the current £93 per Ha) under a Brexit Deal, but the farm would still be profitable provided it can maintain its current support levels. Even with support unchanged, Meadow Farm starts to generate unsustainable losses under No Deal with a projected deficit of £45 per Ha, equating to a £7,000 loss.

- Domestic Market Opportunities: could arise for domestic producers if trade barriers reduce the competitiveness of imports. However, the proposed access granted under additional TRQs in the beef sector would diminish this. There are also fears that future changes to standards might make imports more competitive, thus limiting domestic market opportunities even further.

- Frictionless trade with the EU27 as a third country is not currently possible: and looks set to remain so for at least a decade as the required technology has not yet been developed, let alone tested. Long-term, technology can contribute to reducing this via e-certification systems, but friction cannot be reduced completely. Post-Brexit increases in trade friction are inevitable.

- Most significant non-tariff measures relate to value deterioration: value deterioration (especially fresh meat) arising from border-related delays associated with physical checks and sampling (associated with sanitary and phytosanitary (SPS) regulations) is of most concern to industry and is the biggest contributor to non-tariff costs generally. Its impact on frozen products is much lower but still a factor in terms of potential penalties imposed on delayed consignments.

- Uncertainty about future border arrangements: under No Deal centres particularly on trade on the island of Ireland which the UK Government has claimed would remain frictionless. If there are also no checks on NI-GB trade, whilst any exports routed from Dublin to Holyhead would be subject to tariffs and regulatory checks, the potential for re-routing meat from the Republic of Ireland via NI and onwards to GB without any checks, could result in substantial volumes of Irish beef being placed on the UK market (beyond the 230Kt TRQ) by the ‘backdoor’. If significant volumes enter the UK in this fashion, substantial price declines for UK beef farmers would ensue.

- Disproportionate impact on Small and Medium-Sized Enterprises (SMEs): arising from higher operating costs, fewer loads dispatched and a lower propensity to avail of special authorisations such as AEO status (which confers a lower risk on operators from a regulatory authority perspective).

- Inflationary pressures: particularly for farm-level imported inputs from the EU27 (e.g. fertiliser, medicines etc.) but also elsewhere. These costs are unlikely to be absorbed by the supply trade and would be passed on to consumers and/or to primary producers (i.e. farmers). Any meat price rises are likely to cause consumers to increase their propensity to substitute with cheaper sources of protein, thereby making it more likely that beef and sheep farmers would beat the brunt of price pressures.

The study concluded that a Brexit Deal based on a comprehensive FTA and close customs and regulatory arrangements with the EU would be far preferable to a No Deal Brexit, which could have a devastating impact, especially for sheepmeat. Whilst developing overseas markets will be crucial to the long-term success of British beef and sheepmeat, close attention must be paid to protecting existing markets, specifically the domestic UK market and the EU27 export market. The study also found that even if the UK had never entered the EU (or EEC) in the first place, it is highly likely that markets such as France would still be vital to the British sheepmeat industry due to proximity. To minimise any upheaval post-Brexit, the report states that having a comprehensive mutual recognition agreement between the UK and the EU is crucial.

The report’s findings were similar to several previous studies; however, this study goes into significantly more detail on how non-tariff measures could affect the sector. It also provides useful insights on the implications of a No Deal Brexit for carcase balance in the sheepmeat sector where it estimates that up to 22% of the annual UK lamb kill (3.1 million head) could be affected. This would be a major challenge to a sector where approximately one-third of the lamb crop is exported each year. If it wasn’t already clear, this report underscores the importance of a good Brexit Deal for the grazing livestock sector. The report is available via: https://ahdb.org.uk/knowledge-library/red-meat-route-to-market-project-report