Old crop grain and oilseed markets tumbled through March. There is a compounding set of factors behind this, including good planting progress in South America, improved weather in key growing regions, lacklustre domestic demand, and tariffs on Canadian canola (rapeseed) products.

The most liquid old crop UK feed wheat futures contract (May-25) reached a contract low in March at £172 per tonne. Domestically, the strong import campaign this year is going to result in an increase in stocks year-on-year. This is despite a 20% reduction in wheat production in 2024 compared to 2023. Milling wheat premiums have been eroded by the strong import levels. Milling wheat premiums have fallen to just £20 per tonne, compared with £60 per tonne post-harvest.

There is currently a £20 per tonne carry from old crop (May-25) to new crop (Nov-25) futures. With crops reportedly coming out of winter in good condition, with limited disease levels, this premium could come under pressure.

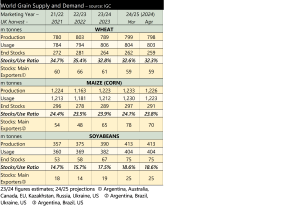

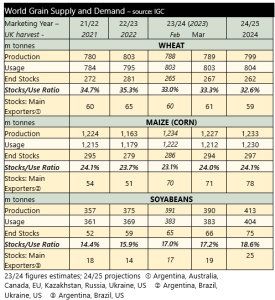

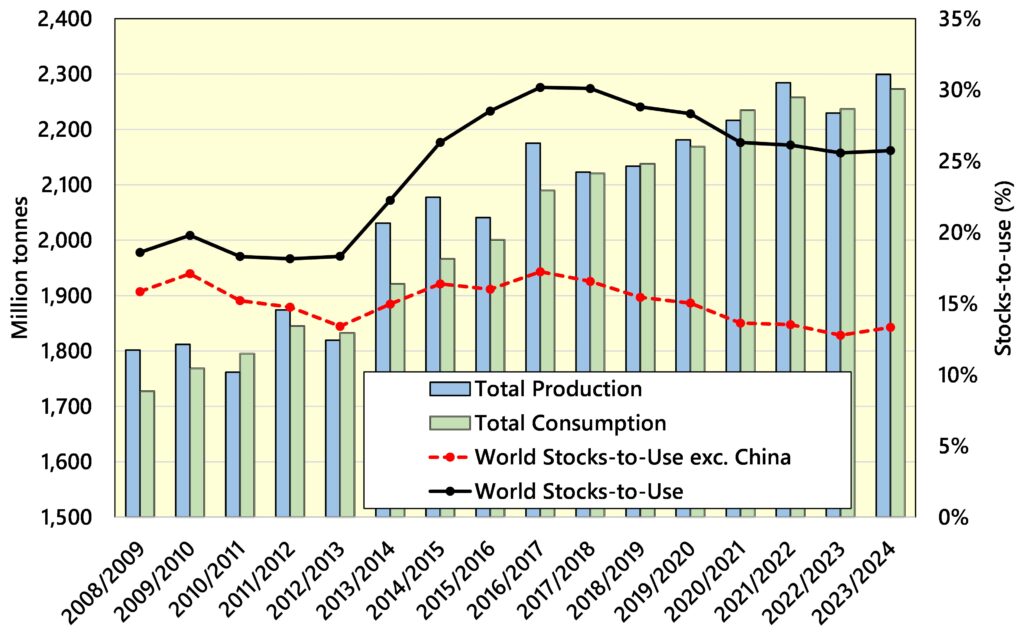

The International Grains Council (IGC) published its first projections of supply and demand for the 2025/26 season on 20th March. It forecasts that wheat carryover stocks will fall by six million tonnes year-on-year, despite an eight million tonne increase in wheat production. For the wider grains complex, a forecast 52 million tonne increase in maize production leads to a one million tonne increase in total grain stocks. The increase in stocks is further underpinned by an eleven million tonne increase in major exporter stocks. This will put pressure on maize prices which is the main cereal crop in terms of global output. There is still a long way to go until the 2025 crops are harvested so there is time for prices to move in either direction depending on crop progress and conditions.

For oilseeds, soyabean stocks are expected to rise marginally, year-on-year (up one million tonnes). However, prices have been undermined by the ongoing ‘trade war’. Following a drawn-out anti-dumping investigation, China has placed 100% tariffs on Canadian canola (rapeseed) oil and meal. Since the beginning of March, the value of Paris rapeseed futures (Nov-25) has fallen considerably. From 3rd to 17th March the value of the contract fell by €40 per tonne (reaching €460 per tonne). Prices have since recovered to €475 per tonne.

Currency is another important watchpoint for the UK market. Sterling has moved stronger against the Dollar. This reduces UK grain prices relative to global markets. However, it also makes imported inputs cheaper. Movements against the Euro have been mixed although the Pound is currently weaker than at the start of the year (supportive of rapeseed prices in the UK).