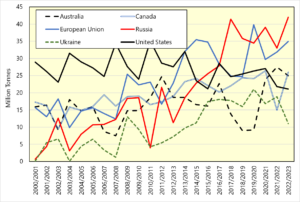

Throughout November the price of grain has fallen back considerably. Futures prices were dropping before the announcement of a 120-day extension to the Ukrainian grain export corridor, 17th November. Global grain markets have softened primarily on expectations of a large maize crop. The crop underpins global feed and industrial (ethanol) markets.

There are expectations of record maize production in South America, in response to high prices. Brazilian weather conditions appear well suited to a big crop. Conversely, Argentina is also forecast for a record maize crop despite currently experiencing a severe drought. The drought in Argentina has, however, trimmed production outlooks for wheat. South American weather remains a key watch point for grain markets, particularly with an active La Niña (the third in three years). La Niña brings dry weather to South America.

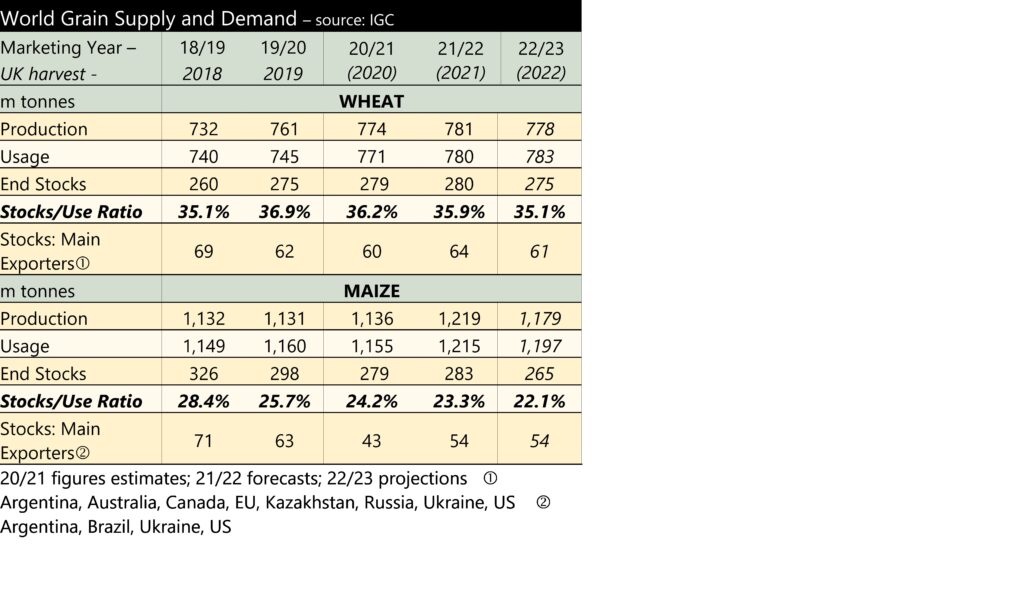

Despite forecasts for bumper maize production, the balance of global grain supply and demand remains tight. This ought to offer some underlying support. However, concerns about the impact of recession on demand, particularly industrial demand, seem to be outweighing this fundamental tightness.

Demand concerns are also impacting global oilseed prices. China’s zero-tolerance approach to Covid is driving expectations of reduced palm oil demand. This, combined with increased palm oil production in Southeast Asia, has depressed prices. This has impacted rapeseed markets with the underlying value of rapeseed oil falling. Additionally, a rebound in Canadian canola (rapeseed) production following last year’s disastrous crop is leaving global oilseeds well supplied.