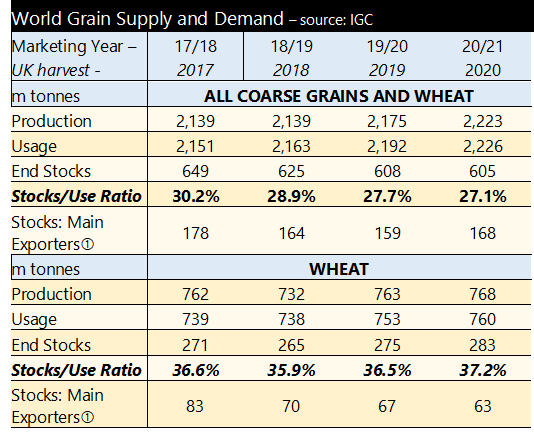

The International Grains Council (IGC) has released its first full supply and demand projection for the 2020/21 year. This shows 48 million tonnes more grain production than last year with a 34 million tonne rise in consumption.

Grain consumption goes up every year (by about this much) as might be expected; simply as the population rises and each person consumes more grain on average (mostly indirectly through animal feed). This means that production should be a record each year, simply to keep pace. However, this coming year, despite production clearly rising by more than demand, the stock level is thought likely to fall, albeit only by 3 million tonnes. This is because the stock level was already falling and simply to keep pace, production would have had to rise further. This is demonstrated in the table. The level of year-end stock has fallen from over 30.1% three years ago to 27.1% now. This is what has underwritten improvements in grain prices in the last year. China is ever-increasing its holdings of grain stocks, with over half of wheat and possibly as much as 65% of global maize grains being held in its stores. This potentially means there is much less grain available than these figures suggest as Chinese stocks are not generally available for the wider market.

18/19 figures estimates; 19/20 forecasts; 20/21 projections (1) Argentina, Australia, Canada, EU, Kazakhstan, Russia, Ukraine, US

For wheat specifically, the picture is reversed. The stock level is seen rising, with a greater rise of wheat production for harvest 2020, resulting in production remaining well ahead of consumption. Overall, the figures suggest a strong level of price support for grains overall, but there is ample wheat, suggesting the price premium that wheat tends to carry over maize and other feed grains, might be rather slim for a year, notwithstanding the impact of lock down.