UK cereal and oilseed pricing continues to face pressure from global market conditions. Ex-farm feed wheat (nearby) was worth £179 per tonne in May. This is down £9 per tonne on the April average price. The price of feed wheat has now fallen more than £40 per tonne since January. Milling wheat continues to hold a strong premium over feed wheat, extending to £70 per tonne on average in May. Feed barley prices averaged £165 per tonne in May, with the discount to wheat narrowing.

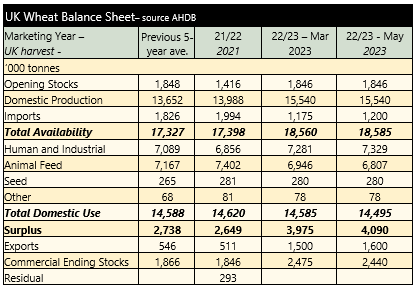

AHDB published its latest UK supply and demand estimates for the 2022/23 season. The estimates highlight the increased ending stocks for both wheat and barley. Large cereal crops from harvest 2022, have been met with weak animal feed demand. The ongoing challenges for the pig and poultry sector resulted in a further cut to wheat demand of 130Kt.

The challenges for animal feed demand will carry into the new season. With large carry-in stocks and crops generally looking healthy, domestic prices will need to remain export competitive.

The value of Oilseed rape has fallen to the lowest point since October 2020, at £345 per tonne ex-farm in May. Prices have continued to fall throughout the month, reaching £330 per tonne, delivered into Erith, on 24th May. Oilseed rape prices are being undermined by large EU carry-in stocks for the new season, with the EU expected to harvest its largest OSR crop since 2014 (20 million tonnes). Wider oilseed market fundamentals are also pressuring OSR prices, with the USDA forecasting a 40 million tonne increase in soyabean production in 2023/24.

Bean and Pea prices have bucked the trend of other combinable crop markets, with both commodities gaining £7 per tonne, month-on-month. Feed beans were quoted at £228 per tonne and peas £234 per tonne.