Whilst multiple rounds of negotiations have taken place, talks with the EU have been stalling due to impasses on several key issues. These include governance (role of the European Court of Justice), ‘level playing-field’ issues, fisheries, criminal and judicial cooperation as well as the implementation of the Irish Protocol. On 15th June, the Prime Minister and the EU Commission President, Ursula von der Leyen, held talks where they agreed to intensify negotiations (to be held on a weekly rather than fortnightly basis) in a bid to secure a deal. Most analysts now believe that it will be October before a deal is likely to emerge.

Transition Period Extension

It now seems that the deadline for extending the Transition Period beyond 31st December this year will pass with a whimper rather than a bang. The UK Government has made it clear it will not be asking for an extension before the 1st July cut-off. The EU sees little point in asking for one from its side as it simply provides an opportunity for the UK to say ‘no’. There is a top-level committee that meets just before the deadline, but the conference call between Boris Johnson and von der Leyen has effectively ended the chance of extending the Transition.

There is still a wide gap between the parties to bridge on many issues over the next three or four months. Many commentators now believe the most likely outcome is a ‘bare bones’ deal before the end of the year. Negotiations may then continue in the months that follow, including January and beyond, to fill in the details. Negotiators could return to the deal over the years that follow to add elements or deepen the provisions (depending on political will). This all highlights Brexit is a process rather than an event. And it is all a long way from the ‘easiest trade deal in history’ promised by Liam Fox back in 2017.

Level Playing Field

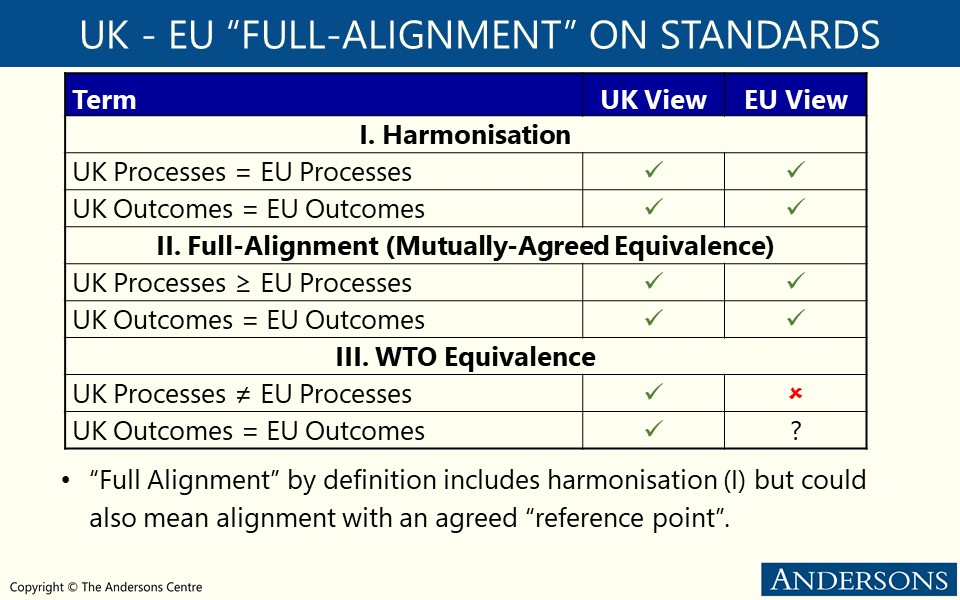

From an agri-food perspective, much of the focus is on the level playing-field issues, particularly which standards will apply in the UK from January. Whilst the UK Government has mentioned that the same high level standards will continue to apply, others believe that some dilution in standards is likely to take place as the UK tries to secure trade deals elsewhere. During a House of Commons debate on 11th June, Michael Gove stated that the UK Government was “committed to making sure that high animal welfare and environmental standards continue to characterise British farming, which is the best in the world.” During the same debate he also mentioned that the food available to consumers would “always meet high quality standards”. Arguably, this latter statement could have a looser interpretation which leaves open the possibility of accepting alternative standards on some imports. As previous articles have noted, the EU is keen to ensure that the UK’s standards remain as close as possible to the EU’s, otherwise, EU exports will not be as competitive in the UK market. This would put pressure on prices within the EU due to an excess of supply if alternative markets cannot be found.

In an attempt to resolve the level playing field impasse, there are reports of a proposed compromise that the UK would reserve the right to diverge from the EU’s standards in the future but that Brussels would have the right to impose retaliatory tariffs or place restrictions on the UK’s access to the Single Market for services. Although some view this compromise as having the potential for constant friction in the UK-EU relationship, it has the potential to open-up a landing zone for a Deal. But, time is very tight and a breakthrough is needed soon if the October deadline is to be met.

Post-Transition Border Controls

On 12th June, the UK Government also announced that it plans to delay the full imposition of border checks on imports from the EU, but acknowledges that exports from the UK to the EU27 are likely to be subject to checks from the outset. Border controls would be introduced over three stages from January to July 2021.

- Stage 1 (from January 2021): traders importing standard goods will need to prepare for basic customs requirements (e.g. keeping sufficient records of imported goods) and will have up to six months to complete customs declarations. Although tariffs will need to be paid on all imports, payments can be deferred until the customs declaration has been made. Checks on controlled goods like alcohol and tobacco will take place. Businesses will also need to consider how they account for VAT on imported goods. There will be physical checks at the point of destination or other approved premises on all high risk live animals and plants.

- Stage 2 (from April 2021): all products of animal origin (POAO) (e.g. meat, pet food, honey, milk or egg products) and all regulated plants and plant products will require pre-notification and the relevant health documentation.

- Stage 3 (from July 2021): declarations required at the point of importation for all goods and relevant tariffs must also be paid. Full Safety and Security declarations will be required, while for SPS commodities there will be an increase in physical checks and the taking of samples. Checks for animals, plants and their products will take place at GB Border Control Posts.

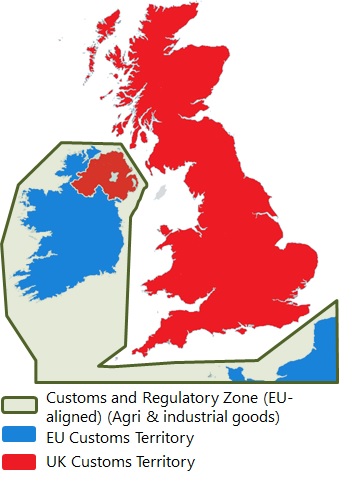

Implementation of Northern Irish Protocol

Whilst these arrangements will give UK businesses some more time to prepare it is important to note that regulatory checks on trade moving from GB to Northern Ireland are likely from January 2021 as a result of the provisions of the Northern Irish Protocol. This has the potential to create significant friction on agri-food trade between GB and NI. Whilst the UK Government has sought to alleviate this by announcing plans to reimburse companies for any imposition of tariffs, there are a lot of questions around how all of this would work. For instance, what paperwork would be required? How long would it take for reimbursement as the application of tariffs would have a significant impact on cashflow, even if they are only applied where goods are deemed “at risk” of entering the Single Market? A concept that is still quite vague and it would be helpful if the EU could define more precisely what would constitute a material risk to its Single Market.

Furthermore, there are State Aid Rules issues (which NI businesses would still be subject to). These rules limit the amount of state aid that companies can receive (circa €200,000 over 3 years). Given the substantial tariffs applicable in agriculture, some companies will quickly run up to these limits.

Although numerous challenges remain with the introduction and implementation of the Northern Irish Protocol, there has been progress in several areas recently. The HMRC have provided some details on the regulatory arrangements it plans to introduce on GB to NI trade. This includes;

- Declarations: a Pre-Import Declaration and a Safety & Security Declaration will be required. A Transit Accompanying Document might also be needed, particularly if consignment is route from GB to Northern Ireland via the Republic of Ireland.

- Goods Movement Reference: will be used to notify the authorities of the consignment details, vehicle and shipping details.

- Pre-Lodgement Model: would be used so that declarations and pre-notifications would be undertaken before shipping from GB.

- Risk Assessments: would take place whilst consignments are at sea.

- Upon Arrival: a confirmation would be provided before arrival if consignment is okay to proceed, or if a check is required.

- Goods Vehicle Movement Service (GVMS) IT platform: will link the various documentary declaration references with the vehicle registration references so that one reference can be presented at the frontier.

- SPS checks: details emerging from the negotiations suggest for UK exports to the EU (including EU checks imposed at NI ports and airports) all consignments will be subject to Documentary and Identity checks and physical checks will take place on up to 30% of consignments, with a 15% physical check rate likely for red meat. Whilst these physical check rates are lower than the EU default for third countries (50% for poultry meat and 20% for red meat), they have the potential to create significant friction.

It has been reported that the HMRC plans to have its IT platforms ready for testing in September or October before they ‘go live’ from 1st January. Although it is reassuring that the HMRC appears to be making significant progress, the timeline remains immensely challenging. It leaves little room for error, which has been a challenge with previous IT systems. Of course, whilst the authorities might claim to be on course for “being ready” for the 1st January, it is another matter entirely whether businesses are ready. Business groups have been calling for a six-month delay before the Protocol becomes fully operational. The Covid Crisis has meant that many businesses have been unable to focus much on preparing for the post-transition period of late. Few believe that businesses will be ready for the changes due to come into force on 1st January. It is evident that some form of further implementation (or application) period is needed.

EU Negotiations Timelines

Below is a summary of the key milestones anticipated in the months ahead.

- 1st July 2020: deadline by which any extension of the Transition Period must be agreed. The UK has already said that it would not be seeking an extension and the EU has noted this.

- 15-16th October 2020: European Council due to take place. A deal would need to be reached by this point, with legal texts finalised, to permit the EU to undertake its ratification process.

- October – December 2020: conclusion and ratification of first UK-EU future relationship agreement.

- 10-11th December 2020: European Council due to take place where any agreement is likely to be formally adopted.

- 31st December 2020: Transition Period formally ends.

- 1st January 2021: new UK-EU trading relationship applies. UK applies limited border control checks on imports from EU. EU likely to impose full regulatory checks on exports from the UK, including at NI ports and airports.

- January 2021: negotiations on outstanding issues of the UK-EU trading relationship likely to commence. The various Joint Committees planned during the EU Withdrawal negotiations will play a key role.

- April 2021: UK introduces full regulatory checks on all POAO and plant products.

- July 2021: full regulatory checks and payments of tariffs on all goods at the UK border.