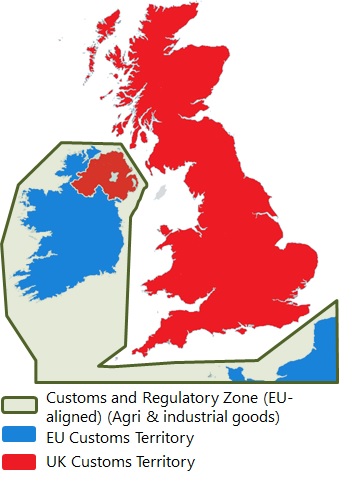

On 7th December the UK and EU announced that they agreed ‘in principle’ how the Northern Ireland (NI) Protocol would be implemented. This is a significant achievement given the problems in other UK/EU talks, and has been widely welcomed, especially by business groups. However, there is unease in some quarters on the how the new procedures will work in practice.

The arrangements will enter into force irrespective of whether the UK and the EU reach an agreement on their future trading relationship, although if such an agreement were reached, it would make the operation of the NI Protocol much easier. Key aspects include;

- No checks on goods being transported from NI to GB: this issue caused problems throughout 2020 as the EU was insisting that Exit (Export) Summary Declarations were required for Safety and Security purposes. This requirement has been obviated through the use of commercial data (e.g. from shipping manifests), which is already collected, to meet safety and security obligations. This is a pragmatic solution to the issue.

- Trusted Trader scheme: is to be introduced for supermarkets and other suppliers. This ‘UK Trader Scheme’ is primarily directed at businesses whose products will be sold to NI consumers and who can prove that such products will not leak into the Republic of Ireland (EU Single Market) and thus be potentially liable to tariffs (under a No Deal). Traders who believe that their products being sold to NI are not ‘at risk’ of entering the EU Single Market can register for authorisation via’ https://www.gov.uk/guidance/apply-for-authorisation-for-the-uk-trader-scheme-if-you-bring-goods-into-northern-ireland-from-1-january-2021

- Reimbursement scheme: for traders who are not part of the UK Trader Scheme or who cannot guarantee that their goods will remain in the UK customs territory (including NI) can join this scheme to have any tariffs paid upon entry into NI reimbursed if such goods are eligible to be traded freely in the UK. This will require proof that such goods have remained in the UK customs territory.

- Grace periods for traders to adjust to new arrangements: these vary from 3 months to 12 months and are predicated on UK regulatory standards remaining aligned with the EU’s for the periods in question. A range of issues are covered including;

- Export Health Certification: will not be required on retail shipments of plant and animal products for three months, provided the organisations involved register as a Trusted Trader.

- Requirements for some meat products to be frozen: on trade between GB and NI for products such as mince and sausages it will not be mandatory for supermarkets (and trusted traders) for the first six-months. Thereafter, fresh/chilled products will have to be sourced locally from NI or from the EU (particularly the Republic of Ireland). However, this requirement could be obviated as part of a wider trade deal between the UK and the EU.

- Veterinary products: will have a 12-month adjustment period to ensure that there will not be a shortage of critical supplies.

- EU presence in NI: although the EU will not formally have an office in NI, which again caused controversy, its officials will be present to oversee the implementation of the Protocol and the EU will have access to relevant databases to monitor trade flows.

- State Aid: GB-based firms will not be subject to the EU’s State Aid rules where there is no ‘genuine and direct link’ to Northern Ireland and no foreseeable impact on NI-EU trade. Further detail will be needed as to what this means in practice but the clarification addresses a key UK concern over its sovereignty in terms of State Aid regulation.

- Agricultural Support: will continue to be exempted from State Aid, subject to ceilings agreed under the Protocol. The agreement in principle provides that approximately “£380 million of agricultural support” can be provided to NI farming and be exempt from State Aid rules. Up to £25 million of support not used in one year can be rolled forward to the next year and an additional £7 million will be made available for crisis support when required. Current spending on agricultural support (including rural development elements) in NI is around £330 million annually. This arrangement provides further flexibility for NI to support its agricultural industry when it sets its own agricultural policy independently of the EU CAP.

Whilst these temporary arrangements will ease the flow of goods from GB to NI initially, longer-term, there will be a significant increase in bureaucracy as Export Health Certificates (EHC) will be required for animal and plant products and Customs (import) declarations will be required for all goods. Furthermore, products will also be subject to a wide range of regulatory checks. Documentary and identity checks will be required for all plant and animal products subject to Sanitary and Phytosanitary (SPS) regulations. A significant proportion of these products (15% for red meat; 30% for dairy and poultry products for human consumption) will need to be physically checked at a Border Control Post. Added bureaucracy will lead to increased food costs in Northern Ireland. However, it must also be acknowledged that the UK plans to introduce a Movement Assistance Scheme to help traders with ‘reasonable costs’ incurred on EHC and official controls on goods moving from GB to NI. This is in addition to the Trader Support Service launched in August to assist with Customs-related issues.

At least, this grace period, will help to put the necessary infrastructure and systems in place to manage the long-term implementation of the Protocol. Such an application (adjustment/grace) period on any UK-EU trade deal is also needed to give traders and regulatory authorities the time to implement the new arrangements. Further detail on the UK Government’s Command Paper on the NI Protocol and supplementary information is available via: https://www.gov.uk/government/publications/the-northern-ireland-protocol

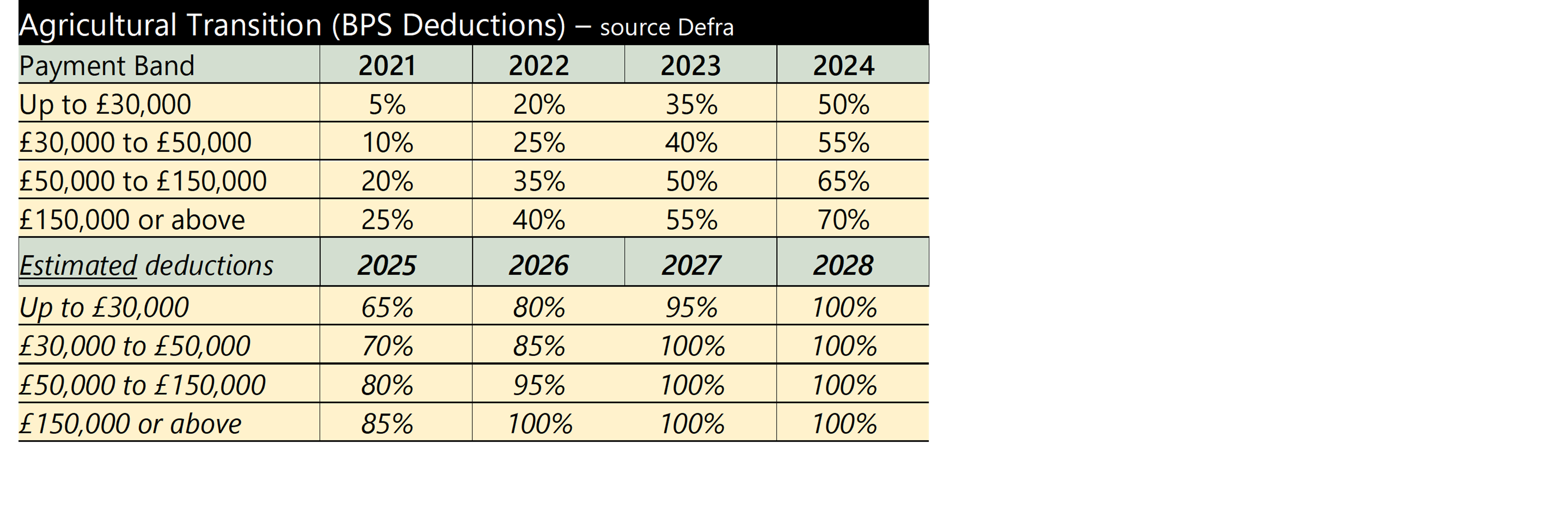

Note that the figures shown are the deductions rather than the percentage being paid. Also, a reminder that the bands work like Income Tax, so all BPS claimants get the lower deductions on their first £30,000 of claim.

Note that the figures shown are the deductions rather than the percentage being paid. Also, a reminder that the bands work like Income Tax, so all BPS claimants get the lower deductions on their first £30,000 of claim.