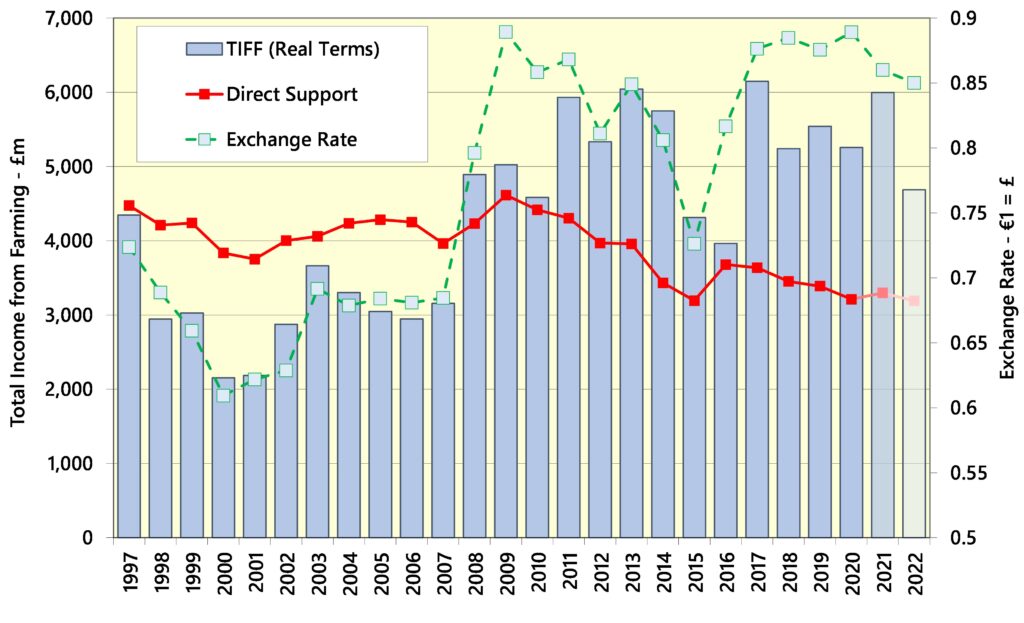

Total Income from Farming

UK farm profits improved by 14% in real terms between 2020 and 2021 according to Defra. The latest figures for Total Income from Farming (TIFF) were released on the 12th May and show that returns increased to £5,998m – the third highest in the last 20 years. TIFF is the aggregate profit from all UK farming businesses for the calendar year. It shows the return to all entrepreneurs for their management, labour and capital invested. In simplistic terms, it is the profit of ‘UK Agriculture Plc’.

Output from both the arable and livestock sectors was higher during the year which offset a rise in costs. Total crop output increased by 20%, whilst livestock sales were up 7%. Costs increased by 12% compared to the 2020 year (and, of course, have gone up considerably more since).

This data is a ‘provisional estimate’. There are often quite large revisions in the figures – both when the second estimate is published in December and when the final figures are produced in a year’s time. For example, the first estimate of TIFF for 2020 was £4,119m. This was then revised upwards to £5,121m in December before now being put at £5,242 (all figures in current prices). We would not be surprised to see an upwards revision in the 2021 figures too – most sectors, with the exception of pigs and horticulture, had a pretty good year.

The chart below shows the evolution (in real terms) of TIFF over the past 25 years. Also included is the average £ / € exchange rate for the year, which is one of the key drivers of overall farm profitability. Also shown on the chart is the contribution of direct support (BPS plus agri-environment scheme payments). This continues to contribute a sizeable proportion of farm profits.

On the chart is an estimate of TIFF for the current, 2022, year. A sizeable drop is forecast. Despite output prices being generally high, increased costs will result in lower profitability.

The full Defra TIFF data can be found at – https://www.gov.uk/government/statistics/total-income-from-farming-in-the-uk

Balance Sheet

Alongside the TIFF figures, Defra also published an updated Balance Sheet for the industry. This shows the Net Worth of farming at the end of 2021 as being £285.6bn. This is a 1% increase on the 2020 figure and shows a rise of 9% (in real terms) over the decade from 2011. The main driver of the increase in asset values is the land price. After falling in the mid-2010’s, land has now shown an increase in value for the past four years