Category: Policy & Business

Trade Roundup

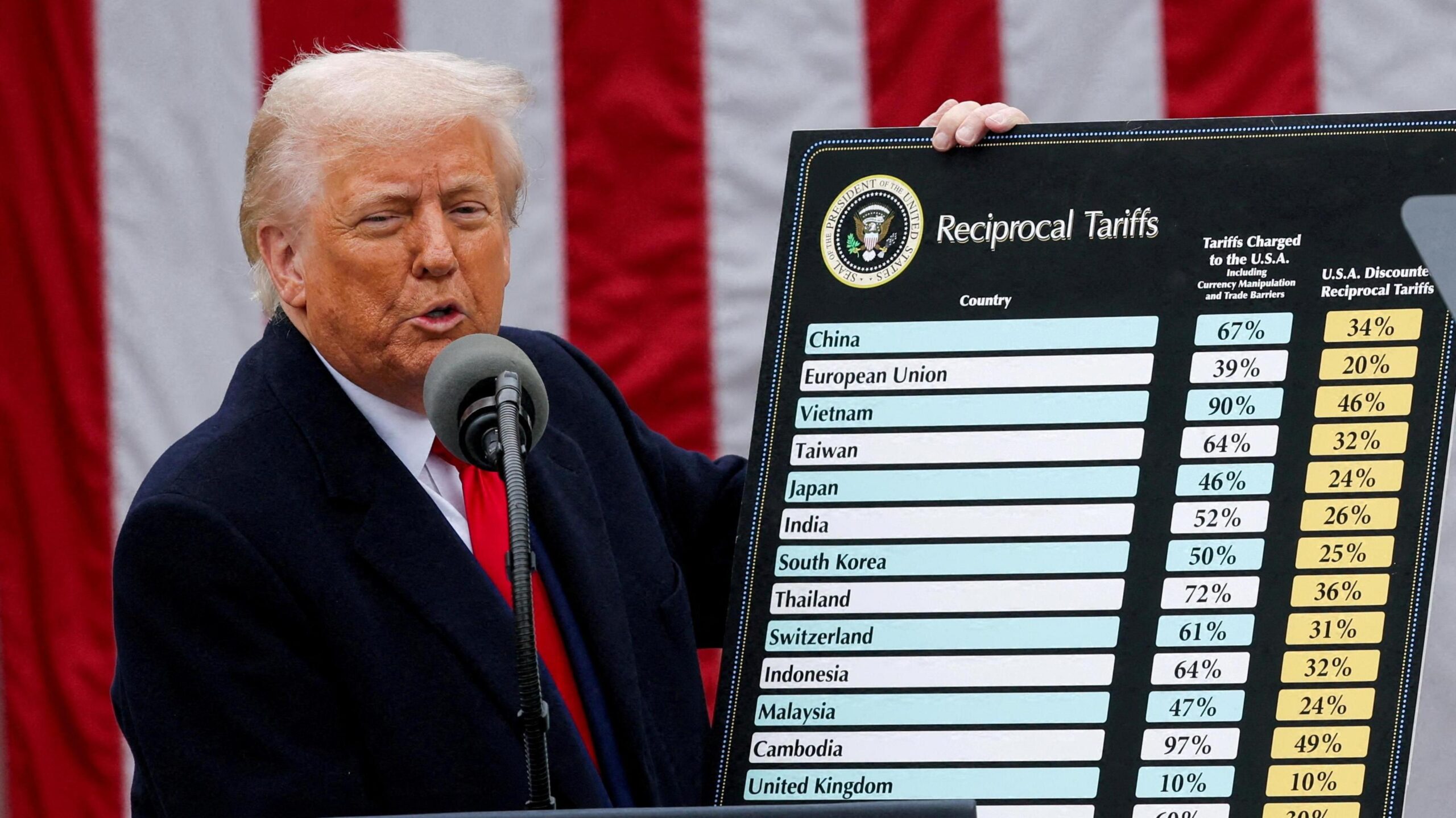

It has been a turbulent month in global trade circles following the US announcements on 2nd April of a swathe of new tariffs being imposed on all its trading partners, with the exception of Canada and Mexico (for most products). This included “universal tariffs” of 10% on most products (excluding key components such as semi-conductors, computer chips etc.), including agricultural goods. Some countries (including the EU (20% tariffs), Japan (24%) and South Africa (30%)) were going to be subject to higher tariffs, which the UK avoided (i.e. UK agricultural exports are subject to the universal tariff only).

Whilst President Trump announced a 90-day pause to the higher tariffs for most countries on 9th April, which has given a temporary reprieve to some, the universal tariffs are in operation. Moreover, for China, a full-scale trade war is now underway with imports of Chinese goods into the US, including agricultural products, now being subject to 145% tariffs. China has retaliated by imposing 125% tariffs on US goods, effective from 12th April and it has suspended imports of key agricultural products like soybeans and pork. In 2022-23, US exports of soybeans to China were estimated at $17.3 billion and from an agri-food perspective, the US exports significantly more to China than what China sends in the opposite direction. (Looking at all goods though China exports much more to the US than trade in the opposite direction).

Trade wars such as this cause significant upheaval on international markets, especially on companies trading directly between the US and China. However, the imposition of tariffs on goods effectively works as a tax on consumption which fuels inflation. Already in the UK, inflation has been trending upwards since the start of the year. The latest estimate (for March 2025) puts inflation (CPI) at 2.6% which is above the Bank of England’s 2% target. Whilst the UK has not imposed reciprocal tariffs on the US any increases in tariffs and associated trade wars are likely to give rise to inflation further down the line.

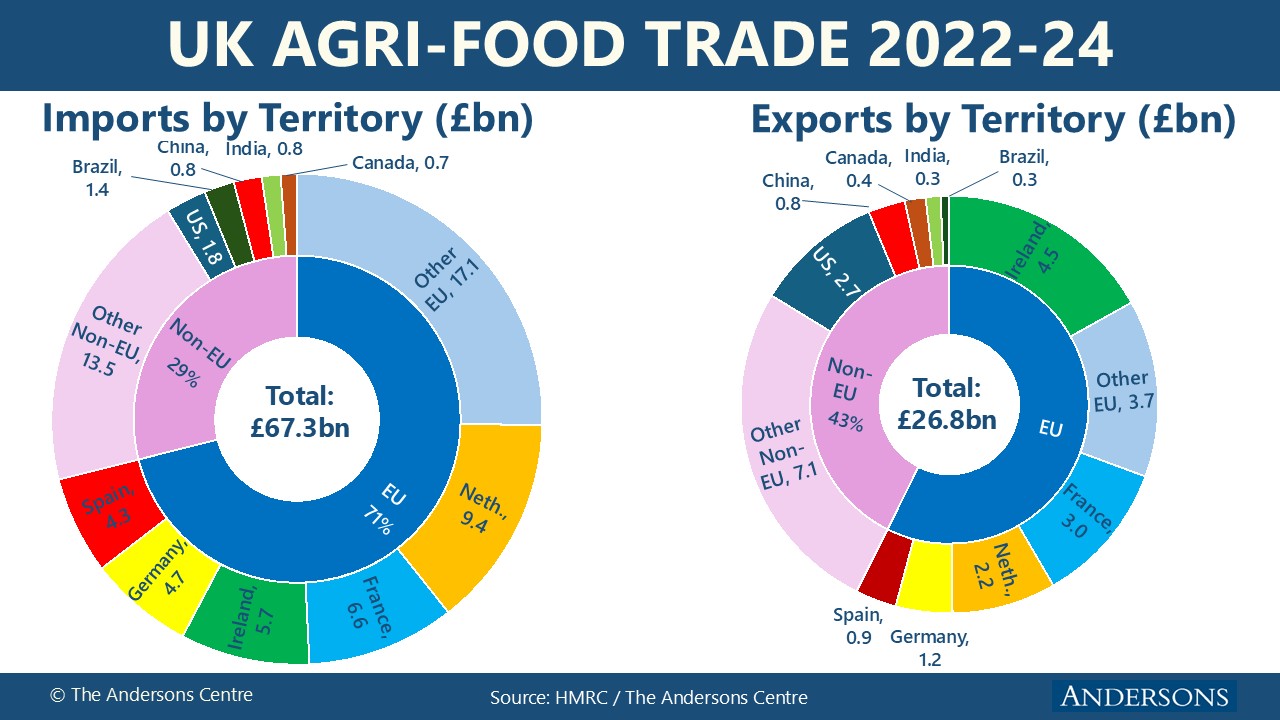

The 10% tariff will also affect UK exports of agri-food products to the US which we reported last month were estimated at £2.7 billion per annum during 2022-24. Within this, whisky exports are particularly significant and were valued at £971 million in 2024. Back in 2019, the previous Trump Administration imposed a 25% tariff on exports of Scotch whisky to the US, as part of a dispute between the US and the EU, which at the time included the UK as a Member State. Back then, the impact on Scotch whisky sales was significant but the tariffs were suspended when the Biden administration took office in 2021. This time around, there is also likely to be an impact on Scotch whisky sales although other countries (e.g. Japan) will also be affected.

The 10% “Trump tariffs” will also have some effects on exports of other UK products to the US including specialty cheeses. That said, other countries will be facing similar tariff levels and a 10% tariff is within the range of shifts in exchange rates which have been seen on trade from time-to-time. The Trump tariffs have weakened investor confidence in the US and as a result the Dollar has weakened noticeably. Since January, the Dollar has weakened from being worth 82 pence Sterling in January to 75 pence at present – 9% decline. This relative strengthening of Sterling will make UK exports more expensive in the US which will also act as a headwind. Conversely, Sterling has weakened slightly against the Euro (by about 1%) over the same period, which should help the competitiveness of UK exports to the EU, which is a much more important market for UK produce.

Overall, upheaval looks like being a continuing feature of international agri-food trade for the foreseeable future which will cause added challenges for global supply-chains and it looks like globalisation, as we have known it over recent decades, is undergoing a significant reversal.

Farm Innovation Programme

Defra has announced funding is available via the Farming Innovation Programme (FIP) for those who want to research or develop an innovative solution to a known problem in the agricultural industry. Readers will recall we wrote about the Programme reopening with funding of £42.5m (see https://abcbooks.co.uk/policy-announcements/). Already open, and closing on 25th June, is ADOPT – Accelerating Development of Practice and Technologies;

- ADOPT – support for collaborative farmer-led, on-farm trials or experiments to generate, test and demonstrate innovative solutions to farming challenges. Project outputs will provide knowledge of new approaches which will be shared to the wider sector to provide confidence for others to adopt.

Two further funding competitions will be available from 5th May;

- Precision Breeding – funding for R & D to enable the commercialisation of precision-bred crops in years, rather than decades which will be nutritious, resistant to pests and diseases, resistant to climate change, and beneficial to the environment.

- Low Emmissions – support for innovative ways to reduce emissions on farm. The examples given include regenerative farming practices, energy efficiency, using organic waste for heat oer electricity generation, and reducing GHG emmissions from livestock production.

There is total funding of £20m for ADOPT and £12.5m for each of the other two competitions, with project costs between £1m -£2.5m available. Applications must be submitted by 25th June 2025. Further information on all three funds can be found via https://farminginnovation.ukri.org/

Farm Profitability Review

Baroness Minette Batters has been appointed to head Defra’s review into farm profitability. The review will feed into the 25-Year Farming Roadmap as well as the Land Use Framework and the Food Strategy. It covers England only. Baroness Batters will be supported by a team of Defra officials – presumably the new ‘Farm Profitability Unit’ as announced by Steve Reed at the NFU Conference in February. The review will also be consulting widely with the industry.

The position of Farming Profitability Review Lead is for six months, indicating the final report will be finalised sometime in September or October. The report aims to make recommendations on policies both the Government and industry could implement to improve farm profitability. It is highlighted that these must be ‘pragmatic’ and will look at the short, medium, and long term. It is stated that this is an ‘internal report submitted to the Secretary of State for his review‘ – but presumably the results will be made public.

The full terms of reference can be found here – https://www.gov.uk/government/publications/farming-profitability-review-terms-of-reference/farming-profitability-review-terms-of-reference . This sets out three main issues for Baroness Batters to consider;

- how farmers can reduce barriers to profitability, increase profit and manage their own risk to improve financial resilience, such as through embracing innovation, improving productivity, increasing market access and using risk management tools

- how the supply chain can support farm profitability such as through greater transparency, cooperation and ensuring a fairer distribution of risks, rewards and responsibilities

- whether there are other ancillary activities that farmers can undertake to support profitability and wider economic growth.

Regulation Review

An independent internal review of Defra’s rules and regulations has been published. The report, which was led by Dan Corry, found that the current system is ‘outdated, inconsistent and complex’. The review concludes that a ‘bonfire’ of regulations is not the solution, but makes 29 recomendations across 5 strategic themes;

- Focus on outcomes, scale and proportionality; with constrained discretion

- Untangle and tidy ‘green tape’ to ensure process-light and adaptive regulation

- Deploy a fair and consistent ‘thin green line’ on regulatory compliance, with trusted partners earning autonomy

- Unlock the flow of private sector green finance to support nature restoration whilst better targeting public sector finance

- Shift regulators to be more digital, more real-time and more innovative with partners

Defra has responded to the report and will ‘fast-track’ the implementation of nine key recommendations, which it has identified as having the greatest impact for growth and nature recovery, these include;

- a single, lead regulator for major infrastructure projects

- rapidly reviewing the existing catalogue of compliance guidance

- speeding up work to update the Environmental Permitting (England and Wales) Regulations 2016

- convene the environmental regulators to set out the work required to upgrade their digital systems for Planning advice, including a single Planning portal for all agencies.

- a new Defra Infrastructure Board to accelerate the delivery of major infrastructure projects

- more autonomy to allow trusted nature groups to benefit from new freedoms to carry out conservation and restoration work without needing to apply for multiple permissions at every step of a project

- a new industry-funded Nature Market Accelerator to bring coherence to nature markets, boosting investment into natural habitats and driving growth

- clearer guidance and measurable objectives for all Defra’s regulators

- rolling regulatory reform

The review was undertaken in response to concerns that environmental regulation is holding back investment and infrastructure – and thus inhibiting economic growth. The notorious £100m HS2 ‘bat tunnel’ is often cited as an example. The full report can be found at https://www.gov.uk/government/publications/delivering-economic-growth-and-nature-recovery-an-independent-review-of-defras-regulatory-landscape/an-independent-review-of-defras-regulatory-landscape-foreword-and-executive-summary

SFS Wales

The Welsh Government provided an update on the progress of the Sustainable Farming Scheme (SPS) at the end of March. In summary, there is little new to report. The overall scheme design remains the same as set out in November (see https://abcbooks.co.uk/sfs-wales/ ). The aim is to provide final scheme rules and, presumably, payment rates in the summer. Likely after the Comprehensive Spending Review provides the budget. The Welsh Government is continuing to work on the details of the Universal Actions and also a number of the Optional and Collaborative Actions that will be available when the scheme starts in 2026. An evidence base with an economic analysis and impact assessment is also being worked on. The full statement can be found at https://www.gov.wales/written-statement-sustainable-farming-scheme-sfs-scheme-design-update .

Spring Statement

There were no (more) nasty surprises for farming in the Spring Statement on the 26th March. The Chancellor, Rachel Reeves, had to announce significant spending changes to stay within her own fiscal rules as lacklustre economic growth and higher debt interest payments reduced her headroom. Ms Reeves has promised only one ‘fiscal event’ per year; the Autumn Budget. Whilst not quite turning into a mini-Budget, the Spring Statement contained rather more than just an update of forecasts. On those forecasts, the Office of Budgetary Responsibility (OBR) has halved its estimate of economic growth for 2025 from 2% to 1% (although growth in subsequent years is seen as being slightly higher than forecast at the time of the Autumn Budget). The OBR’s forecast for inflation (CPI) is for it to peak at 3.8% in July 2025. The average inflation for 2025 is estimated to be 3.2%. There were no new tax increases announced. The spending changes were the previously-announced shift from Foreign Aid to Defence spending (because of classification changes, this results in a saving in the short-term). The greatest effect was a cut in the welfare budget however. Importantly, there was no cut in Defra’s budget for 2025/26 which had been announced in the autumn. Therefore the figures set out in our article last month still stand. Thoughts will now turn to the Comprehensive Spending Review announcement in the summer.

Trade Update

Since returning to office in January 2025, President Donald Trump has reignited his signature ‘America First’ trade agenda. This has escalated tensions with its major trading partners, including China, Canada and Mexico with concerns that the European Union will be next. There are also suggestions that the UK will get caught up in these disputes.

On 4th March, the US imposed a series of tariffs on imports from China. Across goods generally, the US imports more from China than it exports in the opposite direction. However, within agriculture, the opposite is the case and exports of soybeans in particular to China are substantial. Meat exports from the US to China, including pork, poultry and beef are also sizeable. These sectors will now be hit with Chinese tariffs, ranging from 10-15%. It is anticipated that China will source more produce from elsewhere, particularly Latin America. This is what happened when the previous Trump administration imposed tariffs on China.

The US has also announced plans to put 25% tariffs on imports from Canada and Mexico; although these have been suspended until 2nd April if the goods are covered under the USMCA trade deal. Most agricultural goods are covered with the exception of dairy exports from Canada to the US. On 4th March, Canada announced that it was retaliating by imposing 25% tariffs on CA$30 billion worth of imports from the US, and that an additional CA$150 billion of imports from the US would also face similar tariffs by end March. Both the US and Canada have since been in discussions to resolve the trade disputes, but businesses remain cautious given the recent volatility in US trade policy.

In addition, the Trump administration has stated that the EU is on its hitlist for tariffs and on 4th March President Trump stated that ‘reciprocal’ tariffs would be imposed on 2nd April on countries that he believes are treating the US unfairly. Tariffs on steel imports into the US have already been imposed and the EU is preparing a list of products that it plans to hit the US with tariffs from early April. This will include products such as bourbon but other agricultural products such as beef, poultry meat, dairy products, sugar and vegetables will also be targeted.

The US stance on the UK appears to be softer and the President has even floated the idea of a trade deal with the UK. That said, the US administration also implied last month that reviewing the one-month suspension of tariffs on Canada and Mexico was not a priority, but then changed its stance completely. This illustrates the unpredictability of US trade policy and similar could happen with the UK. In 2023 alone, the UK exported nearly £980m worth of whisky to the US and during the 2022-24 period exported on average £2.7 billion worth of agri-food goods to the US. In addition to whisky, the UK has also carved out lucrative niches for products such as specialty cheeses. On its part, the US only exports about £1.8 billion worth of agri-food goods into the UK and as part of any trade deal, it would be keen to increase that figure by exporting more beef for instance.

Although the US has made overtures about a trade deal, the prospects of an agreement appear some way off. The Labour Government is more focused on re-setting its relationship with the EU. The Government will need to strike a delicate balance between any closening of the relationship with the EU whilst not attracting unwanted attention from the US in terms of tariff actions. That said, a longer term trade deal with the US cannot be ruled out, especially if there were to be a change in Government at the next general election.

More generally, trade wars unsettle commodities and financial markets whilst also creating upheaval for supply-chains in addition to being inflationary. With UK inflation rising again, and projected to reach 3.7% in late 2025 (significantly above the Bank of England’s 2% target) the effects of a global trade war adds to economic uncertainty.

Planning and Infrastructure Bill

The Planning and Infrastructure Bill had its first reading in Parliament on the 11th March. This is one of the Government’s flagship pieces of legislation as it aims to deliver on the ‘growth’ agenda through changes in the planning system. It also aims to boost the drive to net zero through supporting renewable infrastructure. Farmers and landowners are very likely to feel the effects of this legislation

Most of the bill relates to England and Wales, although the energy elements will have GB-wide application. It is large piece of legislation split into a number of components;

- Infrastructure: streamling the Nationally Significant Infrastructure Projects (NSIP) regime; improving the system for connecting projects to the electricity grid; amending the rules on Highways works

- Planning: more local flexibility to set Planning fees; introduction of regional strategic plans for Planning

- Development and Nature: introduction of a ‘Nature Restoration Levy’ – this would replace the requirement for site-by-site mitigation of environmental impacts through mechanisms such as Nutrient Neutrality. Instead, the requirements would be aggregated up and delivered on a more strategic level through Environmental Delivery Plans.

- Development Corporations: to build proposed New Towns and other large-scale developments.

- Compulsory Purchase: changes to the rules to speed up development. One of the key changes here is to remove ‘hope value’ from the compensation paid if land is being compulsorily purchased for public good uses such affordable housing, healthcare or education.

The full Bill can be found at https://commonslibrary.parliament.uk/research-briefings/cbp-10216/. There may be significant amendments to the legislation as it passes through Parliament.

Food Strategy

The Government has started the process to produce a national Food Strategy. It has set up a Food Strategy Advisory Board (FSAB). This will be chaired by Daniel Zeichner, Minister for Food Security and Rural Affairs, and will include a selection of members from the food supply industry (including a farmer member – Sam Godfrey).

The cross-Government Food Strategy will ‘restore pride in British food’ by ensuring a food system that ‘backs British food, grows the economy, feeds the nation, nourishes individuals, and protects the planet, now and in the future’. The food strategy will work to improve the food system to:

- provide more easily accessible and affordable healthy food

- maintain our food security by building resilience

- reduce the impact of farming and food production on nature, biodiversity and climate

- ensure growth is at the heart of the Food Strategy

The FSAB will meet monthly. It is also planned to have wider industry consultation on the Food Strategy in due course. The timetable for the publication of the final Strategy is unclear at present. More details of the FSAB and its members is available at – https://www.gov.uk/government/news/leading-food-experts-join-government-food-strategy-to-restore-pride-in-british-food