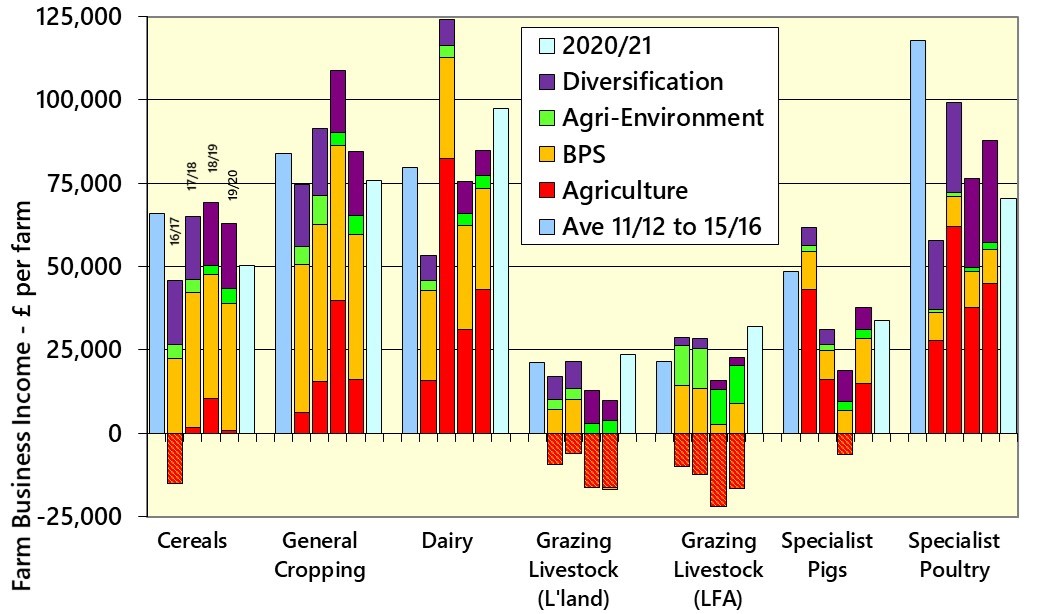

Defra has released its revised Farm Business Income (FBI) figures for 2019/20. Taken from the English Farm Business Survey (FBS), the data shows FBI for various standard farm types. FBI can be thought of as equivalent to the ‘Net Profit’ measure widely used in accountancy. These results update the provisional ones released earlier in the year. The FBS works on Feb/March year ends so the period being reported covers harvest 2019 and the 2019 BPS. The full release can be found at https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/944352/fbs-businessincome-statsnotice-16dec20.pdf

In the chart below, the first column for each sector shows the average FBI from 2011/12 to 2015/16. The next four columns show the FBI for the subsequent four years, broken down into four ‘profit centres’. The final, light blue column is Andersons’ estimate for the current 2020/21 year. As can be seen, only Dairy, LFA Grazing and Specialist Pigs and Poultry farms saw an increase in returns in 2019/20 compared to the year before.

Source:Defra

For Cereal farms there was an increase in yields and areas for some crops, but in general, prices were lower and therefore only partially offset the increase in variable and fixed costs. On General Cropping farms, profits fell by 21% on the year. The return from agriculture was £16,000 compared to £38,900 in the previous year. This was due to lower prices, although an increase in yield for many crops partially offset this. OSR prices were an exception, remaining firm, but the yield and area was lower due to the continued problems with Cabbage Stem Flea Beetle. General Cropping farms have increased their participation in agri-environmental schemes with output from these increasing by nearly 50% on the year to £5,900.

After experiencing a significant drop in agricultural output in 2018/2019 following the highs of 2017/18, dairy farmers have seen a modest (6%) improvement in 2019/2020 with profits from agriculture remaining solid for the sector. Milk production rose, but more because of an increase in cow numbers than yield, however average milk price was down by 2%. Output from other cattle enterprises on the dairy farm saw an 4% increase. Whilst variable costs decreased, notably feed prices, there was a rise in fixed costs, particularly machinery depreciation, rent and other general farm expenses.

Lowland grazing farms saw their profits decline by 25% on the year to average just £9,400; the lowest for this farm type since 2006/07. Poor cattle prices during 2019/20 was the main factor, but also declines in both the sheep and crop enterprises contributed. Both fixed and variable costs reduced but were insufficient to offset the drop in output. Profits from agricultural activities on this type of farm fell to minus £16,300 – more than the Basic Payment (£15,800). Lowland grazing livestock farms saw a big revision from the provisional results forecast earlier in the year which was £19,000, mainly due to an over-estimation of the value of cattle, which was very poor for the year and has thankfully recovered in the current year. In contrast to lowland grazing farms, LFA farms experienced an increase of nearly 50% to £22,800. Input costs, mainly feed and purchased fodder decreased and although the output from cattle also fell, sheep output increased by 7% due to higher prices for breeding ewes and hoggs. Income from agriculture still remained negative though, but LFA farms receive (and rely on) significant payments from agri-environment schemes and also the BPS due to being generally larger. Specialist pigs and poultry have both seen increases for the year, due mainly to a reduction in costs for both farms.

The chart shows a breakdown of where the profit comes from for the years 2016/17 to 2019/20. It can be seen for the two Grazing Livestock farm types the return from agriculture is consistently negative; it takes part (or all) of the Basic Payment to return these farms to profit. This is of real concern when looking ahead to the removal of direct support which is commencing this year. Of course, FBI is only an average for the sector. The range in performance across farms is vast, and the more efficient units are likely to have made a much better return than these average values show. Unfortunately, the opposite is also true. We have made some initial estimates of 2020/21 FBI, shown in light blue on the chart. These show the Grazing Livestock farm types seeing significant improvement mainly due to the better livestock prices experienced since spring 2020, but these are from a pretty low base. Dairy farms are also forecast to see a further increase on the back of solid milk prices and a decline in costs. Lower cereal and other crop output from harvest 2020 are forecast to impact on Cereal and General Cropping farm profits.