Fertiliser usage in Great Britain declined considerably, in the wake of inflated costs, following Russia’s invasion of Ukraine. For the 2022 crop year, overall nitrogen use dropped by 18%, according to data published by Defra in July. In addition, potash (P) and phosphate (K) usage declined by 22% and 29%, respectively.

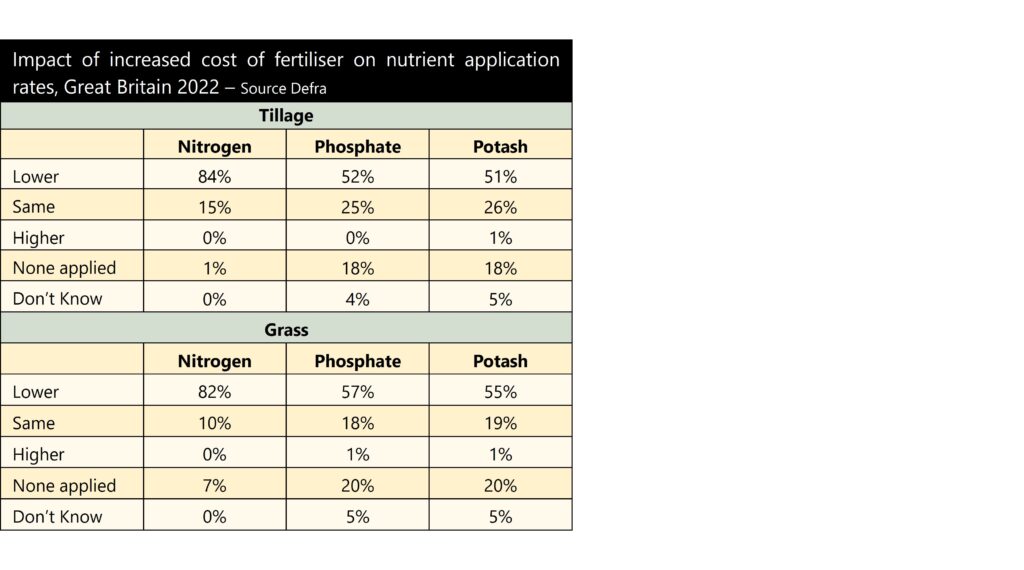

The fall in usage of nitrogen (N) was driven, primarily, by a drop in applications on grassland; down 33% year-on-year. That said, total N use on arable crops also fell by 9%. This is not surprising given the typical timing of purchasing fertiliser in the respective sectors – arable farmers are more likely to have purchased their requirements in autumn 2021 before the invasion of Ukraine saw prices rocket. The impact of the increased cost of fertiliser on nutrient application rates in 2022 is summarised in the table below.

The decision to apply less fertiliser is clearly not as simple as reducing rates purely because it has become more expensive. This is evidenced by the increase in the area being tested for nitrogen, prior to application, in 2022. In 2022, 20% of the arable area surveyed was tested for N content, up from 15% in 2021.

As use of mineral fertiliser fell, applications of farmyard manure increased. The percentage of farms applying farmyard manure increased from 65% in 2021 to 67% in 2022.

In response to inflated costs, Defra added additional questions to the British Survey of Fertiliser Practice in 2022. The questions asked about specific measures taken (or not) because of the increased cost of fertiliser. As a result of the higher cost, 6% of farms increased the area of crops with a lower fertiliser requirement. Additionally, 5% of farms reduced the area of crops grown. There were also indications that farms looked to make longer term behavioural change including 6% of farms introducing new technologies to improve efficient use of fertiliser. Those that did not make a change cited the good grain price/ yield and lower cost of fertiliser at the time of purchasing as key drivers.

Given costs remained high going into planting 2023, we can expect to have seen declines in application rates for harvest 2023 as well. We will not officially know whether that assumption is correct until this time next year.