The Agri-Environment and Climate Scheme (AECS) will be open again in 2024 with an expanded offer. This was announced in the Scottish Governments’ Programme of Government on the 5th September. There will be a focus on organic conversion with an ambition to double the amount of land managed organically. Some actions that were not available in 2023 due to budgetary pressures will be open next year – the chemical & mechanical treatment of bracken, heather cutting and restoring of drystone or flagstone dykes. In addition, the Creation of Hedgerow option has had its limit raised from 500m to 1,000m and the Pond Creation & Restoration will be reintroduced albeit limited to 2000m2 per application. In addition, it was announced that there would be capital grants to improve slurry stores.

The application windows for the various elements are;

Slurry Stores – early 2024 (details to be announced)

Stand-alone organic conversion and maintenance – 1st February 2024 to 31st July 2024

Other Agri-environment – 1st February 2024 to 10th June 2024

Defra has announced an ‘accelerated payment’ for all those with a live SFI 2023 agreement by the end of this year. The payment will be worth 25% of the annual value of their agreement and will be paid within the first month of the agreement. It is unclear when the remaining payments will be made, they are supposed to be paid quarterly. The accelerated payment is intended to help farmers’ cashflows and is in recognition of the challenges faced with inflation and rising input costs.

Although the scheme is not open for applications yet, those interested are able to pre-register. Most will have received an email asking them to complete a form expressing their interest. It is also now possible to complete the form via farmers’ Rural Payment online accounts, using the new Sustainable Farming Scheme link which takes you to the the SFI ‘Register Your Interest’ Form. This form can also be found via https://defragroup.eu.qualtrics.com/jfe/form/SV_4NrweBnVkycIkT4. Those with SFI 2022 agreements are also encouraged to to express their interest in SFI 2023. All 2022 agreement holders will have their agreements terminated and will receive closure payments (see our earlier article https://abcbooks.co.uk/sfi-2022-closure/). Defra will work with these farmers to make an application to the SFI 2023

For those who have already expressed an interest, Defra has said it is ‘on track’ to start inviting them to apply for an agreement from 18th September.

The announcment of early payments under 2023 SFI agreements was part of a mini-package of announcements to mark ‘Back British Farming Day’ on the 13th September. Other elements include;

A £4m Small Abattoir Fund to support improvements at facilities slaughtering less than 10,000 head per year

The opening of recruitment for five extra agri-food attachés to boost the UK agri-food exports, as promised in the Prime Minister’s Farm-to-Fork summit earlier in the year

Confirmation that £15m will be available under the Farming Investment Fund to provide grants for barn-top solar installations. Grant applications will open later this year, along with a further £15m round for robotics and automation.

The Government has changed Planning Rules which could boost the development of onshore wind. There has been a de-facto moratorium on new wind farm developments in England since 2015. At that point the Planning rules were changed so that sites for turbines needed to have been pre-identified in a Local Plan (many areas don’t have a Local Plan, or they do not include such sites). In addition, any wind farm needed to have ‘community backing’. In practice, this meant that a single objector could see a development blocked. The new rules still require turbine sites to be pre-identified, but this can be done in ways other than through the Local Plan. In addition, Planning Authorities will be provided with guidance on how they can reach a ‘balanced view’ of whether their is local support for development. A further announcment will be made in the autumn on mechanisms whereby local communities can receive benefits if they host wind farms. Overall, despite these changes, the Planning hurdles to develop a wind farm in England remain high. There is unlikely to be a surge in opportunities for landowners.

More details have emerged on how the 2022 SFI Standards will be ‘closed’. As we have written previously (see https://abcbooks.co.uk/sfi-2022-agreements/), those who have SFI agreements under the previous 2022 rules will see these terminated with closure payments made.

Defra will give agreement holders 6-months’ notice of termination as required under SFI contracts. It is envisaged that all 2022 agreements will be closed by March 2024. Termination will be timed to coincide with quarter end dates. The closure payments are set out below. They are a ‘per Ha’ rate for each full year left under the agreement (so, for example, if an agreement is terminated after exactly a year, the farmers will get two of the payments set out below – to cover the two years left on the contract);

Arable Soils Standard – Introductory – £15.80 per Ha

Arable Soils Standard – Intermediate – £8.00 per Ha

Grassland Soils Standard – Introductory – £21.80 per Ha

Grassland Soils Standard – Intermediate – minus£5.50 per Ha. This is because the payment rate for the equivalent actions in SFI 2023 is higher – thus the agreement holder gains by moving from SFI 2022 to 2023. If the total claculation comes to a negative figure, there will be no payment made either way.

Moorland Standard – Introductory – no closure payment – the 2023 SFI offer is identical

A figure of £95 will be taken off closure payments to reflect the fact that SFI 2022 agreement holders will now be able to get the £95 flat-rate payment under SAM1.

In terms of entering the 2023 SFI, the aim is to allow any new agreement to start the day after a 2022 agreement has ended. The RPA is working on a way for applications to be made on land already under the SFI 2022. More details will be made available once the main SFI 2023 application process is up-and-running.

Defra has published new Guidance to Local Authorities which should make it easier for farmers to divert footpaths. Effective from 1st August 2023 it covers public rights of way that go through gardens and working farmyards. Local Authorities are now required to give due weight to the privacy, safety and security of landowners when an application to divert or extinguish a path is made. The Guidance does not yet have legal force, but should mean that applications to alter footpaths have a more sympathetic hearing.

Steve Reed has been appointed Shadow Defra Secretary in September’s reshuffle of Labour’s Ministerial team. He replaces Jim McMahon. Mr Reed is the MP for Croydon North and was previously Shadow Justice Secretary. He has little direct experience of farming or rural matters. Daniel Zeichner remains Shadow Minister for Farming and Food. With a General Election having to be held before January 2025, and Labour retaining a healthy lead in the polls, the makeup of the Shadow Cabinet becomes more important.

The application window for the Calf Housing for Health and Welfare Grant is now open. The application process for the grant has three stages:

Stage 1: Online checker

Stage 2: Ambient Environment Assessment

Stage 3: Full application

Our article in July (See https://abcbooks.co.uk/calf-housing-grants/) gives further details on this grant. The Online Checker is now available to make an initial application. This will check an applicant’s eligibility and also how well the project fits with the funding priorities. Applicants will need some basic information about the business and the proposed project including building design, calf space, environmental impacts, location, information on Planning Permission and an estimated total cost.

The Scottish Government has set out its Programme for Government for the next Parliamentary term. This confirms there will be an Agriculture Bill and a Land Reform Bill introduced – probably both this autumn. The former will provide powers to enact the proposed new support arrangements. The latter will look to introduce a public register of land ownership, strengthen the right-to-buy provisions, and also update agricultural tenancy legilsation. The Programme for Government also sets out plans for a new Housing Act, which will introduce further controls in the private rental market – potentially affecting farmers and estates letting surplus cottages. Finally, the announcement states the the Government will prepare to introduce (likely in the next session) a Natural Environment Bill.

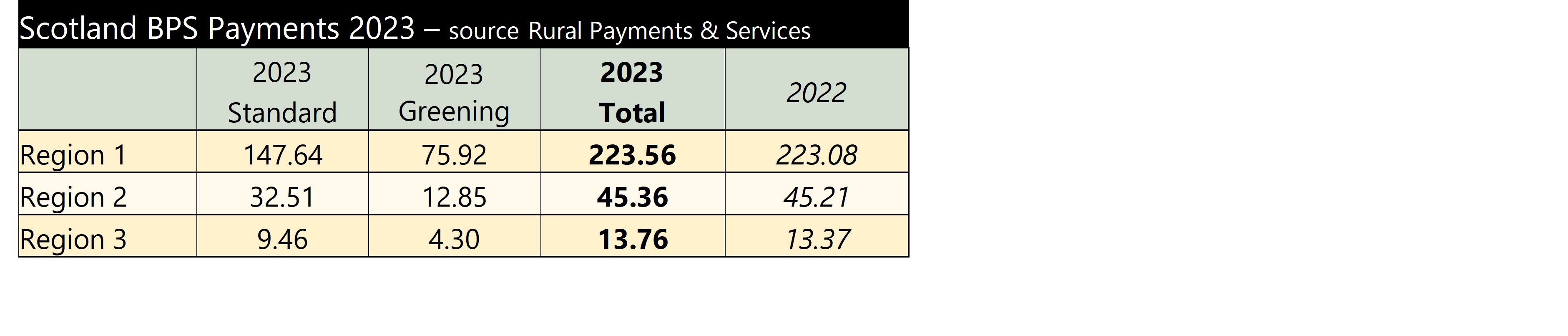

Scottish BPS payments will be a whisker higher than last year. The Scottish Government has published the rates for this year, with advance payments due to begin this month. Rates have gone up by around 0.2-0.3% – this will be due to slightly less entitlements being claimed as the budget is fixed. The table below sets out the breakdown between Standard BPS and Greening, plus last year’s rates. More detail is at – https://www.ruralpayments.org/news-events/increased-rates-for-basic-payment-scheme-and-greening-2023.html .

The Welsh Government has provided some outline guidance on the new interim enviromental scheme announced in July (see https://abcbooks.co.uk/interim-environment-scheme-in-wales/ ). The new scheme will be called Habitat Wales. There will be a six week application window opening later this year, with 12 month contracts offered, commencing on 1st January 2024. All applications will be via farmers’ RPW online accounts.

The scheme will be available to all eligible farmers and grazing associations, including those who have a Glastir Advanced, Commons or Organic contract which ends on 31st December 2023. Eligible land for the scheme falls into three categories;

Land currently under a habitat option within a Glastir Advanced contract (including Glastir Commons).

Habitat land (excluding designated sites), as identified by published maps on DataMapWales which is not currently under management in 2023.

Land managed as habitat which has potential to become habitat land following management.

All identified habitat land must be included in an application and additional land to be managed as habitat land can be included. Payment will be made for following management requirements. Examples of actions that will be prohibited include;

Plough/cultivate, reseed or improve habitat

Apply any inorganic or organic fertilisers such as farmyard manure, slurry, sewage sludge, chicken manure or fish meal

Apply any herbicides, insecticides, molluscicides or any other pesticides (except for spot treatment of invasive species or notifiable weeds)

Allow the area to be poached (existing gateways, feeding and watering areas are acceptable, providing poached and bare areas are less than 5% cover)

Apply lime

Supplementary feed any livestock, except for existing feeding and watering areas

Cut or top more than 30% of rush or weed species in any one year

The scheme will be competitive and only those applications which achieve the greatest environmental benefits will be selected. There will be no payments for capital works, but applicants can apply for these via the Small Grants – Environmental scheme. Full guidance, including payment rates and information of capping will be available in due course.