The Welsh Government has provided more details on its proposed Sustainable Farming Scheme (SFS) and opened a consultation on its plans.

Overall Structure

The three-tier structure for the SFS which has been long-proposed, is retained. This comprises;

- Universal Actions – to be undertaken by everyone in the SFS

- Optional Actions – additional payments available for doing more than the Universal Actions

- Collaborative Actions – working with other land managers to deliver public goods at scale

Universal Actions

The Universal Actions under the SFS will be available from 2025. The document sets out 17 Universal Actions (UA) which all farmers entering the scheme must abide by;

- UA1: Benchmarking – all farms will be required to complete an annual self-assessment focusing on some Key Performance Indicators (KPIs). This information will have to be entered onto a Welsh Government online portal

- UA2: Continuous Professional Development – a minimum of six online CPD modules will need to be completed each year by Partners within the business

- UA3: Soil Health Planning – 20% of a farms soils must be tested each year plus nutrient accounts being completed annually

- UA4: Multispecies Cover Crop – on all land which would otherwise be left bare post-harvest for a period of more than 6 weeks

- UA5: Integrated Pest Management – all farms using Plant Protection products (PPP) must produce an IPM plan

- UA6: Managing Modified Peatland – certain farming practices are prohibited on modified peatland (i.e. peat which is not classed as a semi-natural habitat)

- UA7: Habitat Maintenance – all semi-natural habitats must be managed to benefit wildlife

- UA8: Create Temporary Habitat on Improved Land – features such as fallow margins, headlands, grass strips, herbal leys, cover crops etc. must be established where the farm does not have 10% of its area in Habitat land (see scheme rules below)

- UA9: Designated Site Management Plans – for SSSIs

- UA10: Ponds and Scrapes – farms need to manage or create water features (at least two ponds totalling 0.1Ha on farms under 80Ha; minimum of two ponds totalling 0.2Ha on farms over 80Ha)

- UA11: Hedgerow Management – all hedges to be thick and dense stockproof barriers. 1m buffer strip for sprays and fertiliser from base of hedge

- UA12: Woodland Maintenance – maintain existing woodlands to optimise benefts for livestock, wildlife, and business diversifcation

- UA13: Woodland Creation – tree planting including shelter belts, agroforestry and orchards. Required if the farm does not have 10% of its area in woodland in line with the scheme rules (see below)

- UA14: Historic Environment – maintain and enhance any historic features on the land

- UA15: Animal Health Improvement Cycle – working with a vet to improve livestock health

- UA16: Animal Welfare – complete competency training and carry out lameness and body condition scoring to improve livestock welfare standards

- UA17: Biosecurity – establish protocols to prevent disease entering or leaving the farm

Slightly confusingly, the document also sets out two Scheme Rules and a Universal Code alongside the Actions. The Scheme Rules require that 10% of the farm must be in ‘habitat’ for the benefit of wildlife. In addition, 10% must also be under tree cover. Under the Scheme Rules;

- habitat land covers any semi-natural habitats plus ponds, hedgerows etc.

- where there is woodland, the ground layer of the wood can count towards the habitat percentage whilst the trees contribute to the tree cover requirement

- if there is not enough existing habitat, new temporary habitats can be created under UA8

- woodland, scattered groups and individual trees will count towards the 10% tree cover requirement. Orchards and agro-forestry will also be eligible

- The minimum tree cover requirement must be met by the end of 2029

- in calculating the requirement, it is acknowledged that some areas are ‘unplantable’ – these include land under tenancies where the agreement excludes tree planting; permanent features such as tracks, yards & ponds; and high-quality habitats such as peatland. These areas will be removed from the calculation

The Univeral Code for Habitats applies to any land where the vegetation comprises less than 25% of sown agricultural species. There is a list of managment practices which are prohibited.

There will also be a requirement for all farms joining the scheme to undertake a carbon assessment.

Payments

The SFS will operate on a calendar year basis. There will be an annual declaration of land (probably by 15th May). Advance payments for the Universal Actions are envisaged in October, with a balance in December.

There will be four categories of payment, depending on land use;

- land in existing woodland being maintained

- woodland creation

- habitat (either maintaned or created)

- all other land (i.e. farmed area)

There may be capping of payments (as under the BPS) for large recipients of support.

No details on actual payment rates have been released as the Welsh Government is waiting to find out the budget settlement for 2025 onwards. The methodology of calculating payments will effectively be ‘income foregone’.

Phasing and the BPS

Farmers will be able to choose to continue with the BPS, or move onto the SFS. Once they have opted for the SFS they cannot go back to the BPS. BPS payments, including Redistributive and Young Farmer Payment will be phased down over the Transtion Period 2025 to 2029 as set out in the table below;

BPS capping will also be adjusted to fit in with tapering down of payments.

BPS capping will also be adjusted to fit in with tapering down of payments.

For those that choose to go into the SFS, there will be a safety-net during the Transition so that their SFS payment is at least the same amount as their BPS would have been. Measures will be put in place to prevent the BPS claimant population and individual BPS claims increasing in size during the Transition. This will mean, from 2025;

- farmers who choose to participate in SFS will surrender their entitlements

- the National Reserve will be closed; new entrants will be directed to the SFS

- the transfer of BPS entitlements will be restricted to those who transfer and / or lease entitlements with the land and farmers currently leasing in entitlements for land they currently claim under BPS

- the two-year entitlement usage rule will be removed.

Optional & Collaborative Actions

These will not be available in 2025, the document indicates they will be introduced later, but does not specify a precise date. In the meantime, a number of existing schemes will continue. These include;

- Small Grants – Yard Coverings

- Small Grant – Environment scheme

- a range of Woodland schemes to create new and manage existing agro-forestry and woodland areas

- Integrated Natural Resources Scheme and the National Peatland Action Programme

- the Sustainable Innovation Scheme – helping to join up supply chains

- Nutrient Management Investment – helping to ensure water is protected from pollution

- Animal Health and Improvement Cycle – a Pilot will help improve on-farm animal health and welfare measures

This is to be the final consultation before the scheme is launched. If most Government consultations are anything to go by, there is likely to be little difference between the proposals set out here and what is finally enacted.

Details can be found at – https://www.gov.wales/sustainable-farming-scheme-consultation . Responses to the Consultation need to be made by the 7th March.

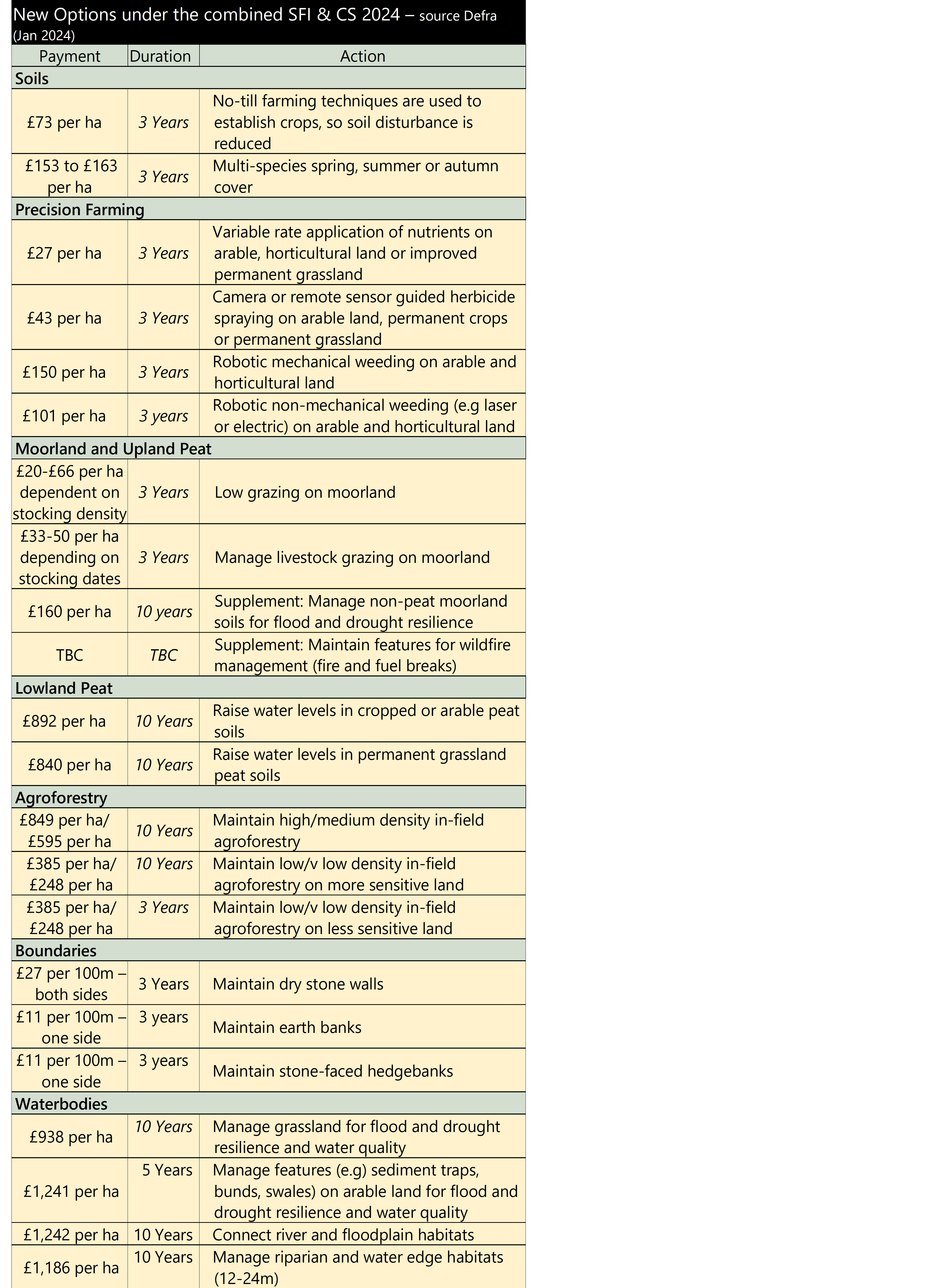

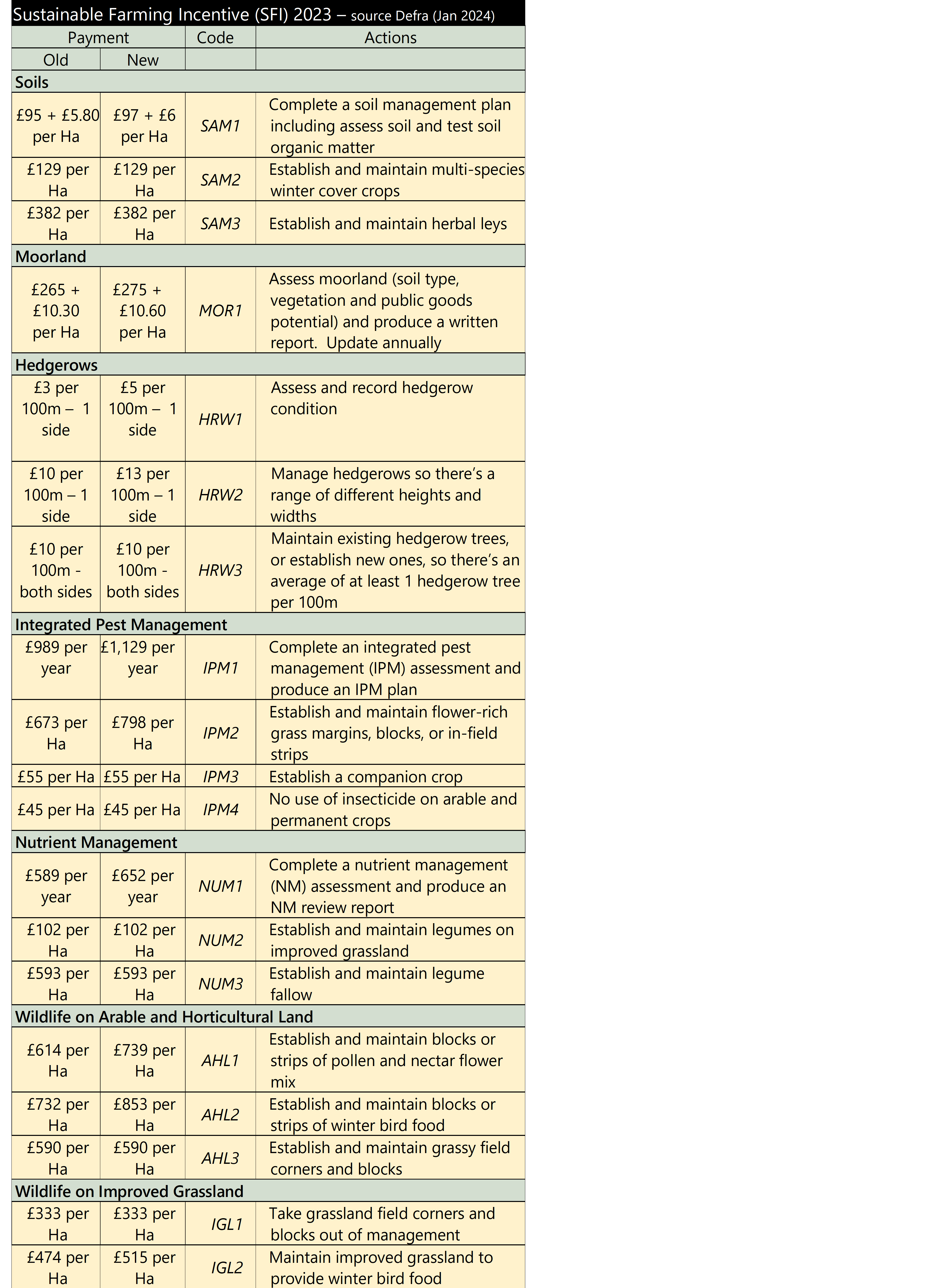

New Actions

New Actions