The AHDB has estimated GB milk production for September was 998m litres. This is 0.9% more than for the same month last year and the second highest in 25 years. Deliveries show an unusually strong increase throughout the month. Production in the last week of September was 2.8% higher compared with the last week in August. According to AHDB statistics, the 5-year average is a 0.6% increase between the two weeks and it has never been more than 1.2%. Daily deliveries are currently tracking at 1.9% above the AHDB’s recent forecast and are in line with where it expected deliveries to be in mid-December. There is anecdotal evidence that more herds are moving to autumn calving. Those that have shifted this year are likely to have calved a little earlier, July/August which could account for some of the rise during September. Next year these will ‘slip’ again to calve mid-August. Summer grass growth has also been good for many this year. However, according to Defra’s most recent data, cumulative production is still behind last year by 0.4% after some producers cut their output in response to over-supply as the country adapted to lockdown under Covid rules.

In contrast, global production from the six key exporting regions (EU-27, Argentina, Australia, NZ, UK and the US) was 1.7% above last year’s levels, for the period from January to August. These regions account for more than 65% of global milk production and 80% of global exports of dairy products. All key regions, except the UK have increased production year-on-year. As the largest producers, the EU and the US have increased most in volume terms (up by 1.3% and 1.8% respectively, compared to the same period last year). But Argentina and Australia have shown the largest year-on-year percentage growth up by 8.4% and 4.9% respectively, albeit on the back of relatively poor years in 2019.

The UK is the only key region to record a decline over the period. However, this is quite small and was on the back of high production in 2019. If current production trends continue, the UK may also be showing a rise in output by the end of the milk year. The extra production around the world may start to have a negative impact on prices, especially if global demand is sluggish due to the economic impact of Covid-19.

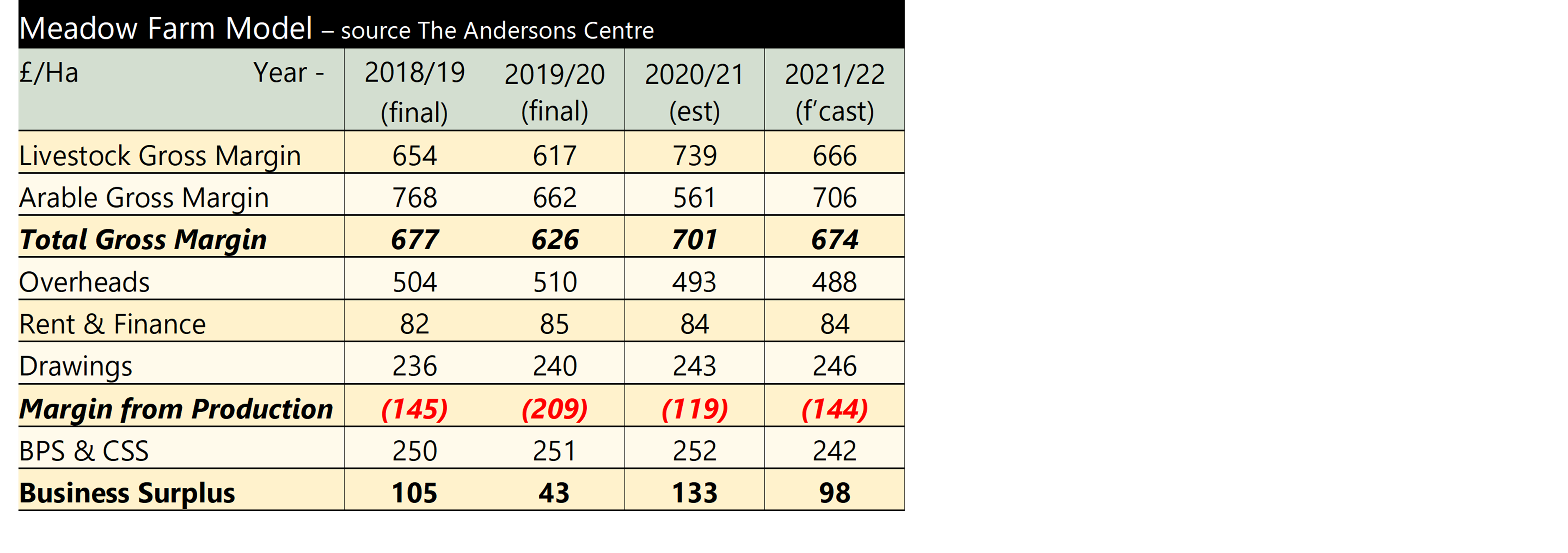

Looking ahead to 2021/22, notwithstanding the possibility of a No Deal Brexit, the sheep price is forecast to decline. But if we do not get a Trade Deal with the EU, Meadow farm could experience a much sharper fall in sheep prices. The beef price is also expected to drop back from its current high as more cattle become available. In contrast, the crops gross margin is forecast to increase as yields recover to a more ‘normal’ level next year. Overheads continue to fall, as a lack of confidence in the industry over Coronavirus and in particular Brexit, sees the proprietors of Meadow Farm refraining from investing. The margin from production remains negative, similar to 2018/19 and it, again, takes the BPS and CSS to provide any profit. This is lower though as the BPS is reduced by 5% in the first year of the BPS Transition, which will see direct payments reduced to zero by 2028.

Looking ahead to 2021/22, notwithstanding the possibility of a No Deal Brexit, the sheep price is forecast to decline. But if we do not get a Trade Deal with the EU, Meadow farm could experience a much sharper fall in sheep prices. The beef price is also expected to drop back from its current high as more cattle become available. In contrast, the crops gross margin is forecast to increase as yields recover to a more ‘normal’ level next year. Overheads continue to fall, as a lack of confidence in the industry over Coronavirus and in particular Brexit, sees the proprietors of Meadow Farm refraining from investing. The margin from production remains negative, similar to 2018/19 and it, again, takes the BPS and CSS to provide any profit. This is lower though as the BPS is reduced by 5% in the first year of the BPS Transition, which will see direct payments reduced to zero by 2028.