Beef

GB cattle prices have been strong throughout the year so far, with prime and cull deadweight values about 50p per kg more than the five-year average. Robust demand for domestic beef from the retail sector and tighter supplies have supported the price. According to Defra, UK beef production from January to June totalled 447,100 tonnes; 3% less than the same period in 2020. Carcase weights are very similar, so the decrease is attributable to lower numbers. The prime cattle kill and cow slaughter were down 3% and 4% respectively on the year. Imports and Exports were also lower. For the period January to May, imports of fresh and frozen beef were 24% less than in 2020, with exports also down for the same period by 30%. Reduced imports were mainly due to lower shipments from Ireland, but imports from other EU countries were also reduced. In contrast shipments from non-EU countries increased by 25%; from a pretty low base though, to 2,400 tonnes. Lower exports to the EU and in particular the Netherlands and Ireland were responsible for the reduction in exports.

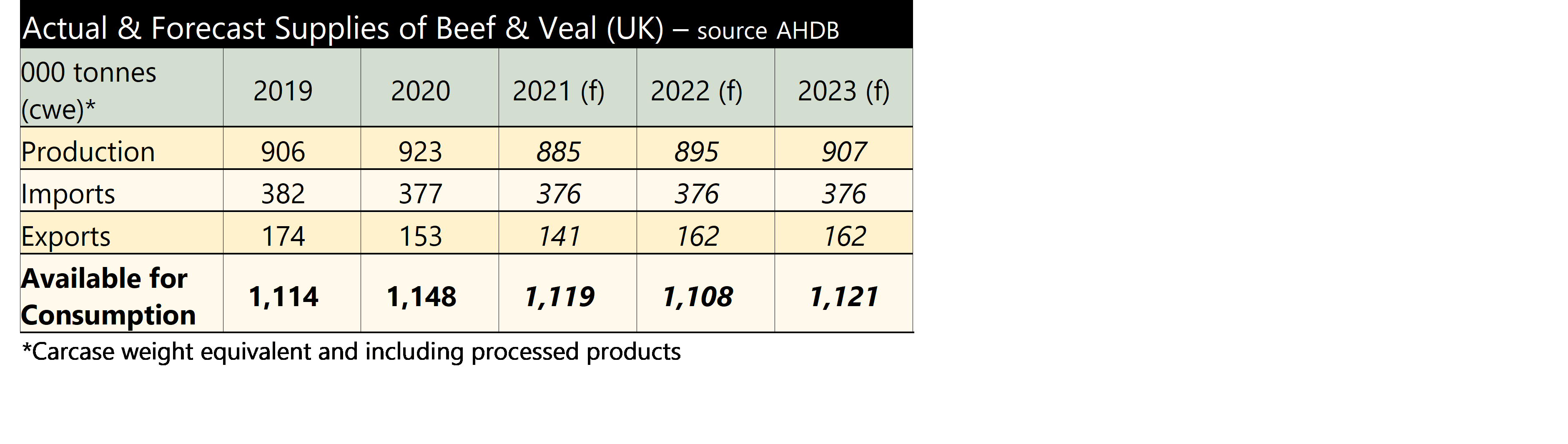

Looking ahead, the AHDB is forecasting total UK beef production in 2021 to decline by 4% compared with 2020, to 885,000 tonnes. Both prime cattle and cow slaughter numbers are forecast to be 4% lower in 2021 compared with 2020. Average carcase weights have been on a general downwards trend since 2015 and marginally lower weights are forecast for 2021. Imports are forecast to be down slightly; by 0.4% over the year as trade increases in the second half of 2021. A rise in demand from the foodservice sector, together with lower domestic supplies is expected to increase the demand for imported beef, this could have a negative impact on GB cattle prices. However, Irish supplies are expected to be tight this year. Bord Bia has indicated a 6% reduction in the Irish cattle kill in 2021 compared with 2020. Furthermore, wider EU beef production is forecast to drop by 1.4% for the year and supplies globally are expected to be tighter for the rest of 2021 due to lower availability in Australia, Brazil and Argentina. Imports from the EU could also be impacted by changes to requirements on UK imports which are to be introduced from October 2021 such as health certificates. Physical checks are due to be introduced from January 2022.

With regards to exports, the AHDB is expecting them to decline further than first forecasted for the year; latest estimates are down by 8%. This reflects the lower volumes in the first quarter (see above), but with trade increasing towards the end of the year as European foodservice markets continue to re-open. However, exports could be limited by tight domestic supplies, strong cattle prices and the new challenges to export for trade between the UK and EU. The table below summarises the AHDB’s forecasts for supplies:

For farmgate prices, tight supplies both domestic and from Ireland will continue to support values. But we have seen how retail demand for British beef has helped during Covid. The foodservice sector tends to rely more on imported product, so as this market continues to open up it will be important that this sector supports domestic suppliers.

For farmgate prices, tight supplies both domestic and from Ireland will continue to support values. But we have seen how retail demand for British beef has helped during Covid. The foodservice sector tends to rely more on imported product, so as this market continues to open up it will be important that this sector supports domestic suppliers.

Sheep

Finished lamb prices reached record-breaking highs this spring and continue to trade comfortably above the highest price received over the last five years (which currently happens to be last year). Similar to beef, sheep prices are being supported by tight supplies and strong domestic demand from retail and the takeaway market. Imports for January to May are down by 20% year-on-year. Shipments from New Zealand and Australia have been reducing for a few years now due to lower production in these countries and also an increase in demand from Asia. Imports from Ireland have also more than halved over the period. UK exports relate closely to production, and so the reduction in lamb output impacts on exports. Additional trade friction between the UK and EU has also played a part in exports declining by 23% over the first 5 months of the year.

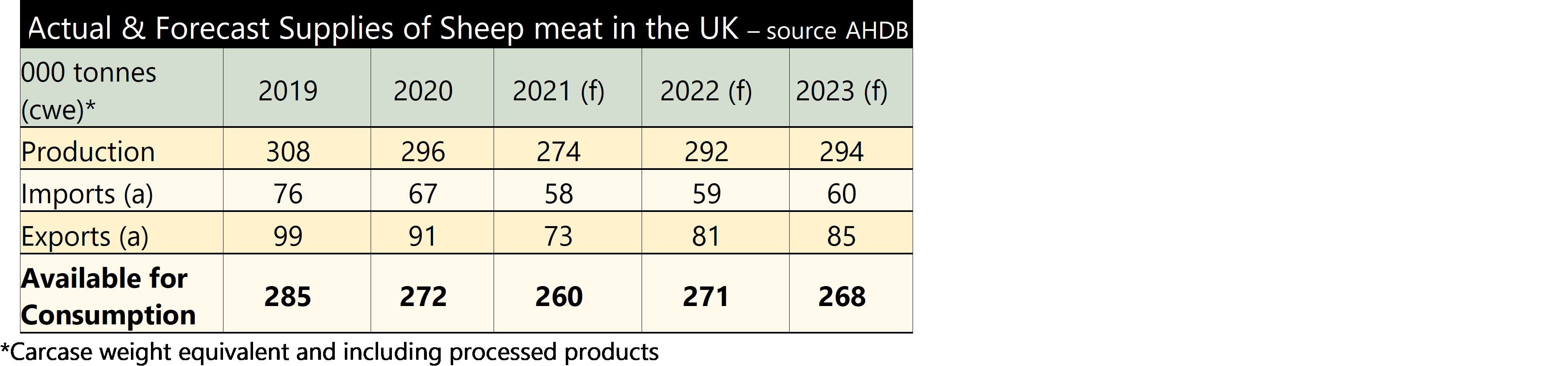

This year, the monthly lamb slaughter profile is expected to return to a more normal pattern. In 2020 the Brexit uncertainty saw lambs marketed earlier than usual. As a result, the AHDB is forecasting the lamb kill in the second half of 2021 to be 4% lower than in 2020, with a 4% year-on-year increase in the carry over. A lower lamb kill combined with reduced adult slaughter numbers results in the AHDB forecasting the UK sheep meat production for the year to decline by 7% to 274,000 tonnes. Imports and exports are both forecast to decline. Supplies from both Australia and New Zealand are predicted to continue to be lower than historic levels. Both are rebuilding their flocks following droughts and demand from Asia remains, but this may be limited as Chinese domestic pork production recovers from African Swine Fever. In addition, global shipping costs and container availability is reducing the competitiveness of New Zealand lamb. Imports are expected to decline by 13% this year, although this is expected to stabilise as imports are required to balance domestic production in the UK. Exports will correlate with production and will therefore also decline this year.

Tight domestic supplies and high shipping costs should help insulate the UK market and support prices through 2021, as there are signs global prices are starting to decrease. Further ahead will depend on whether the increase in consumer demand can be maintained. The table below summarises the AHDB’s forecasts for supplies: