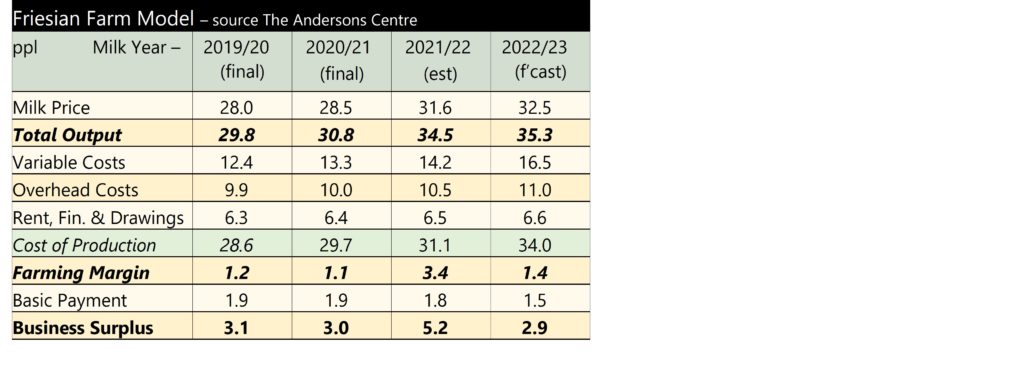

The latest figures for our Friesian Farm model illustrates the rapidly changing fortunes of dairy farming as milk prices and costs both move sharply.

Friesian Farm is a notional dairy business milking a little over 200 cows. It has been used to track the fortunes of British dairy farming for well over a decade. It has a year-round calving system, like most of the UK industry, but it is trying to maximise yield from forage. The farm comprises 130 hectares (of which 60 hectares are rented on an FBT). The proprietor provides labour along with one full time worker (plus casual/relief). The table below shows the farm’s actual results for the two previous milk years (April to March), a budget for the current 2021/22 year then a forecast for 2022/23.

The figures are averages for an entire milk year. For the current 2021/22 year, this means milk prices are not as high as presently seen, as, for a large portion of the year values were lower. By the same token, whilst costs have risen (winter concentrate feed being a big element) the biggest rises have only been seen over the last few months. In particular, fertiliser for the year was bought last spring at far more ‘normal’ values. This means the returns for the current milk year look likely, on average, to be good.

It is in the following year that cost increases are really seen. This is not just in areas such as feed, fertiliser, fuel and electricity, but also in costs such as labour, property repairs and machinery purchase. Even with a higher milk price, returns are much reduced. The effect of the Agricultural Transition in England can also be clearly seen with the pence per litre value of the BPS declining.

Budgeting ahead is currently difficult due to the fast-moving situation with costs and prices. However, it is fairly clear that testing times for dairy profitability lie ahead.