Production

According to AHDB data, GB milk production totalled 1,139m litres in the peak month of May. Compared with last year, this is 1.5% less. This year, GB milk production peaked at 37.54m litres per day on 6th May and we are now seeing the seasonal decline. How rapidly and how low the fall is from peak will be key over the next few months. Costs continue to increase, but will be felt harder in the winter months; good quality conserved forage will be more important than ever this year. Processors keep increasing farmgate prices (see below) to try and encourage more production. However a decline in the milking herd will not be helping. Figures from BCMS, reveal the GB milking herd declined by 1.6% to total 1.64m head as at 1st April. In contrast, young stock (<2 years) have been steadily increasing and were up by 4.4% compared to the same time last year. This increase commenced a couple of years ago and we should therefore be seeing some of these entering the milking herd. However, it appears they are replacing the older, less productive, cows rather than any herd expansion.

Global production is also recording year-on-year declines. Of the six key exporting regions (Argentina, Australia, EU-27, New Zealand, UK and the United States) only Argentina is experiencing a growth in production, up 2.5% on the year, recording its highest March milk production since 2015. But with the other five all recording declines, global milk production for March was 0.7% down on the year. Adverse weather has impacted production in Australia, New Zealand and the United States. In the EU, Italy and Poland have seen year-on-year increases but declines have been recorded in the key countries of France (-1.2%), Germany (-1.4%) and the Netherlands (- 2.5%). Even Ireland, who has seen strong growth recently, was down 2.5% compared to March 2021.

Prices

Given the status of production outlined above, it is perhaps not surprising at the latest event held on 7th June, the GDT average index recorded a 1.5% increase to $4,656. However, this follows five consecutive declines. Butter and SMP increased by 5.6% and 3% to $6,068 and $4,240 respectively. Whilst cheddar declined by -3.6%, but is still at $5,365. WMP experienced a marginal (-0.3%) fall to $4,158.

With the GDT index on the increase again and production contracting, processors continue to put farmgate milk prices up to try and encourage production and now, also to ‘keep’ their producers who may be looking and welcomed elsewhere. Both Tesco and Sainsbury’s have been under fire for their prices not keeping up, but have both now announced rises to 46p per litre from 1st July; following Muller Direct and Arla. Most farmgate milk prices are now around 46ppl for July except First Milk which will only be 43.45ppl. A further 3.05ppl rise has been announced for 1st August, which will take its manufacturing standard litre price to 46.5ppl; a month later than the rest.

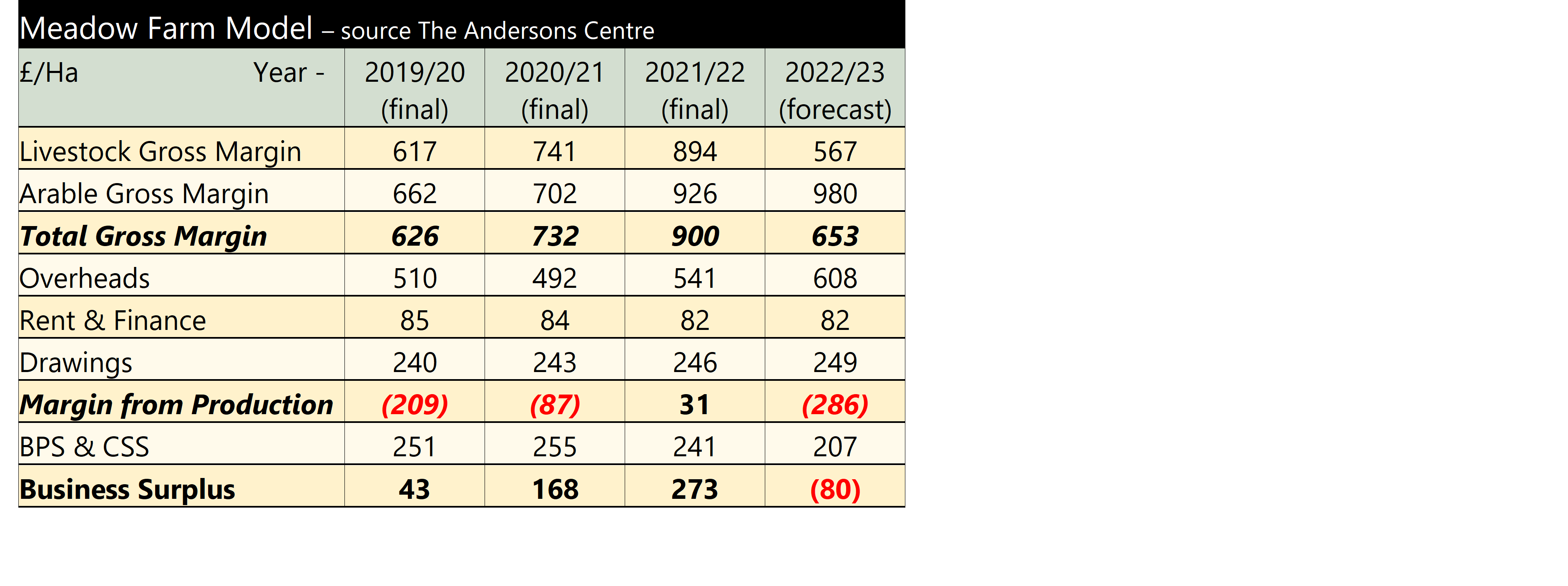

The final column is a forecast for 2022/23 and it clearly shows the impact of increased, fuel, fertiliser and feed costs for this type of farm. Currently, the UK beef price is running ahead of last year’s levels and prices have been ‘tweaked-up’ in the current budget. However, some caution has been exercised. Meadow Farm markets its beef cattle from August to October and an increase in supplies, particularly from Ireland could lower prices by then and this has been accounted for in the budget. In addition, as the energy crisis hits home and consumer spending power is affected, this could see consumers switch to cheaper proteins. However, in lock-down, when consumers were forced to eat at home, the UK beef and lamb market did well. So, if hard pressed consumers reduce their out-of-home consumption, this may not impact as much as might be feared. Overheads rise due to increased fuel prices. A planned investment in a new cattle shed, to replace old ones, means the depreciation increases. The result is the margin from production plummets and not even the BPS, (which is reduced by 20% this year) can bring the Business Surplus back into the black.

The final column is a forecast for 2022/23 and it clearly shows the impact of increased, fuel, fertiliser and feed costs for this type of farm. Currently, the UK beef price is running ahead of last year’s levels and prices have been ‘tweaked-up’ in the current budget. However, some caution has been exercised. Meadow Farm markets its beef cattle from August to October and an increase in supplies, particularly from Ireland could lower prices by then and this has been accounted for in the budget. In addition, as the energy crisis hits home and consumer spending power is affected, this could see consumers switch to cheaper proteins. However, in lock-down, when consumers were forced to eat at home, the UK beef and lamb market did well. So, if hard pressed consumers reduce their out-of-home consumption, this may not impact as much as might be feared. Overheads rise due to increased fuel prices. A planned investment in a new cattle shed, to replace old ones, means the depreciation increases. The result is the margin from production plummets and not even the BPS, (which is reduced by 20% this year) can bring the Business Surplus back into the black.