Production

The AHDB’s estimated GB milk deliveries for 2022/23 is 12.39 billion litres (Defra’s figures will be available on 27th April). This is 0.2% ahead of the previous year. Production started the season very slow when margins were squeezed. But buyers increased milk prices, reaching records levels, encouraging an increase in production with seven consecutive months from September to March recording production at higher levels than in the previous year. Although farmgate prices are now falling, the spring flush means production remains strong. AHDB estimates deliveries for March to stand at 1,088 million litres; up by 1.2% year-on-year, although in line with the five-year average. Daily deliveries for March averaged 35.09 million litres, 3% higher than February as we enter the spring flush.

Milk yields are expected to remain high during the spring, but looking further ahead the extent of the fall in farmgate milk prices (see below) will impact output later in the season. The AHDB is forecasting a marginal growth of +0.5% in production for 2023/24 at this early stage of the season.

Global milk production is also above year-earlier levels. This is based on supplies from the six key exporting regions which includes the UK and also the EU-27, Argentina, Australia, New Zealand and the United States. Global deliveries for February averaged 816.6 million litres per day, up by 0.8% on February 2022. Only Argentina and Australia recorded declines in the month. Deliveries in Australia were 5.3% down on the year due to unfavourable weather conditions, whilst Argentina is feeling the effects of high costs. Production in the EU was up by 0.9% on the year and the US by 0.8% with February being the 8th consecutive month to record year-on-year growth. New Zealand has recorded strong growth, with deliveries 2.3% higher when compared with February 2022.

Prices

The GDT price has seen an unexpected increase at the the latest auction held on 18th April. The average index rose by +3.2% to $3,362. This is only the second time the index has recorded an upward movement in 2023 and follows a -4.7% fall at the auction held in early April. All products recorded rises;

- SMP: +7.6% to $2,776

- Cheddar: +5.7% to $4,411

- Butter: +4.9% to $4,821

- WMP: +1.0% to $3,089

SMP and WMP make up the majority of sales at the auction and are particularly influenced by demand from China. This was lower last year; dairy imports fell by around 19% in 2022. This was due to high imports in 2021 and good domestic supplies increasing supply and soft demand due to China’s zero-Covid policy, low GDP growth and the increased cost of living. Looking ahead, demand from China is uncertain but on balance forecasters are expecting it to recover throughout the year as China’s GDP increases and the country’s Covid restrictions lessen. However, Rabobank is forecasting demand to weaken due to the cost of living whilst supply is likely to increase.

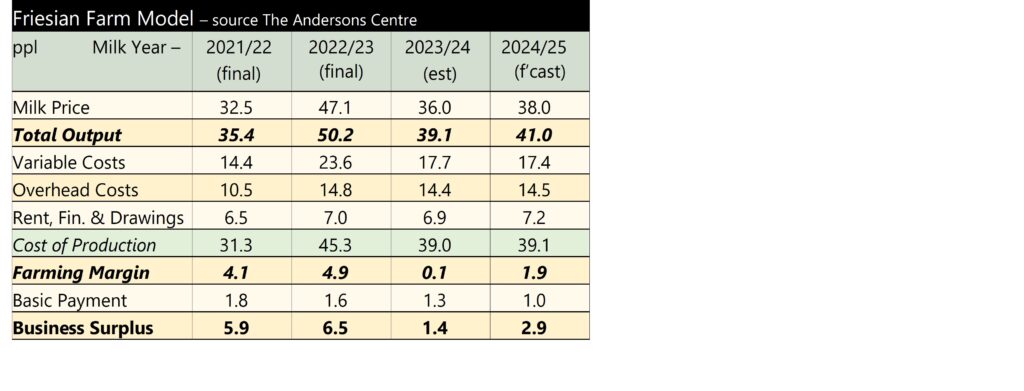

Closer to home, domestic farmgate prices are experiencing further price cuts for May. Muller (Direct), Crediton Dairies, Sainsburys and Muller Co-op are among those who have announced price drops on liquid contracts for May. Meanwhile, Freshways has held its price for May with Tesco increasing the amount it pays to its suppliers by 1.0ppl as it returns to its cost of production model. In terms of cheese contracts, Glanbia, First Milk, Barbers, Saputo, Belton, Lactalis and South Caernarfon Creamery have all announced price cuts for May.