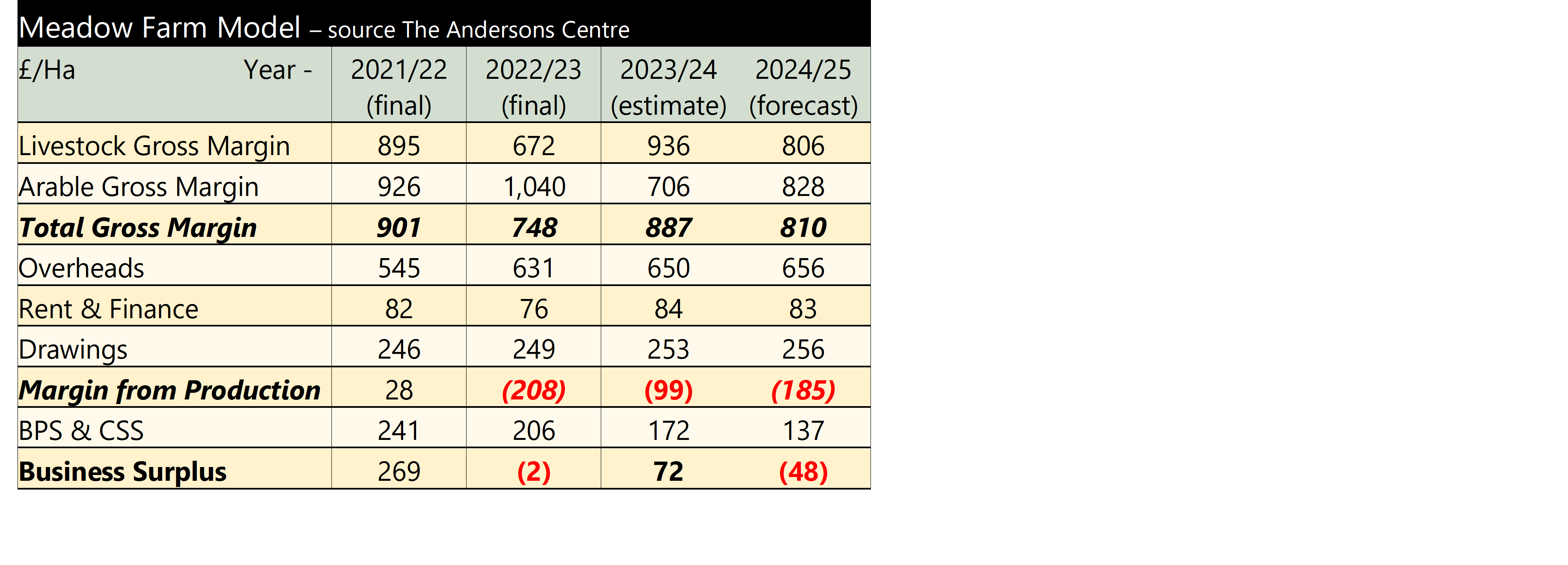

Meadow Farm has been updated for Anderson’s latest Webinar. An increase in the lamb price since the previous update earlier in the summer means, even though the arable gross margin has declined, the returns for the current 2023/24 year have improved. However, the farm’s margin from production remains negative and with declining subsidy payments the future for the business as it currently operates looks unsustainable.

Meadow Farm is a mixed lowland farm, typical of many livestock holdings in England, it is a notional 154 hectare (380 acre) beef and sheep farm in the Midlands. It consists of grassland, with wheat and barley for livestock feed. There are 60 spring-calving suckler cows with all progeny finished, a dairy bull beef enterprise and a 500 breeding ewe flock.

The table below shows the final results for the last two years, an estimate for 2023/24 and a (tentative) forcast for 2024/25. The 2021/22 year was exceptional as the farm made a margin from production for the first time in many years. For 2022/23, it can be seen how ‘agflation’ impacted even when livestock and crop prices were buoyant. In that year input prices rose substantially and feed costs were especially expensive for this type of holding. The result being the farm made a loss of £208 per Ha from production. A further cut to the BPS meant overall the farm made a loss.

For the current, 2023/24 year, high beef prices and an improved lamb price result in a higher estimated livestock gross margin. Meadow Farm markets its cattle in the autumn and lambs from July through to December. It looked likely that the beef price would have to be adjusted downwards as cattle prices had fallen throughout the summer, but over the last month they have made a strong upsurge. The GB deadweight steer overall price has risen from a year low of 455p per kg in the week ending 12th August to 475p per kg in the w/e 16th September 2023 (see Key Farm Facts). The lamb price has been at similar levels to last year over the summer, but is now tracking above it. The latest GB deadweight SQQ overall figure for the w/e 23rd September 2023 was 553p per kg compared with 525p per kg a year earlier. Whilst lower cereals prices brings down the crop gross margin, the overall gross margin figure is higher than 2022/23. However, overhead costs are drifting upwards and the farm again makes a loss from production, although lower than the previous year.

The budget for the 2024/25 year shows a deterioration in the margin once more – mainly through lower budgeted prices. With another drop in the BPS the farm returns to a loss-making position. Meadow Farm is currently in the Countryside Stewardship scheme. This agreement ends December 2023 and the proprietors are currently drawing up an SFI scheme to start when the CS finishes to see if some of the ‘lost’ BPS can be recouped from this scheme.