Tighter beef and lamb supplies in key producing countries across the EU are supporting prices. Reports from the AHDB reveal beef production in Spain and France for the first three quarters of the year is down by -7% and -4% respectively on the year, with Italy experiencing a -20% decline. There is a ‘general decline’ in beef production across the EU, but poor quality grazing and high feed costs is having a particlular impact this year. There are also industry reports that abattoir throughputs of Irish cattle have slowed in recent weeks, supporting prices in Ireland and narrowing the price differential between GB and Irish steers; this stood in the region of 77p per kg at the end of November. GB deadweight beef prices have remained pretty stable since September with the GB all steer average deadweight price for the w/e 9th December 2023 standing at 483.1p per kg, comfortably above the 5-year average and 40p per kg above the same time last year.

The EU sheep reference price has gained in recent weeks. Of particular interest is the Spanish lamb price which has risen by over 200p per kg (deadweight) since August, breaking the 800p per kg barrier at the end of November. Usually the Spanish lamb price is lower than French, by about 50-100p per kg, but it is now trading above; in the region of 50p per kg. Price growth has been seen in France, but not by as much, the same can also be said for Ireland and GB. Sheep meat production across the EU is reported to have declined by -2% in the period January to September. Spain and France have both seen output fall by -9%, with production in Greece down by -3%. In contrast, Ireland has recorded a 2% growth in production. The GB liveweight lamb SQQ has also remained ‘steady’ throughout the autum. The price for the w/e 9th December 2023 stood at 260.1p per kg (585.8ppkg deadweight for the same week), compared with 238.3p per kg in 2022, although prices have now fallen below those received back in 2021.

The latest GB prices can be found in Key Farm Facts.

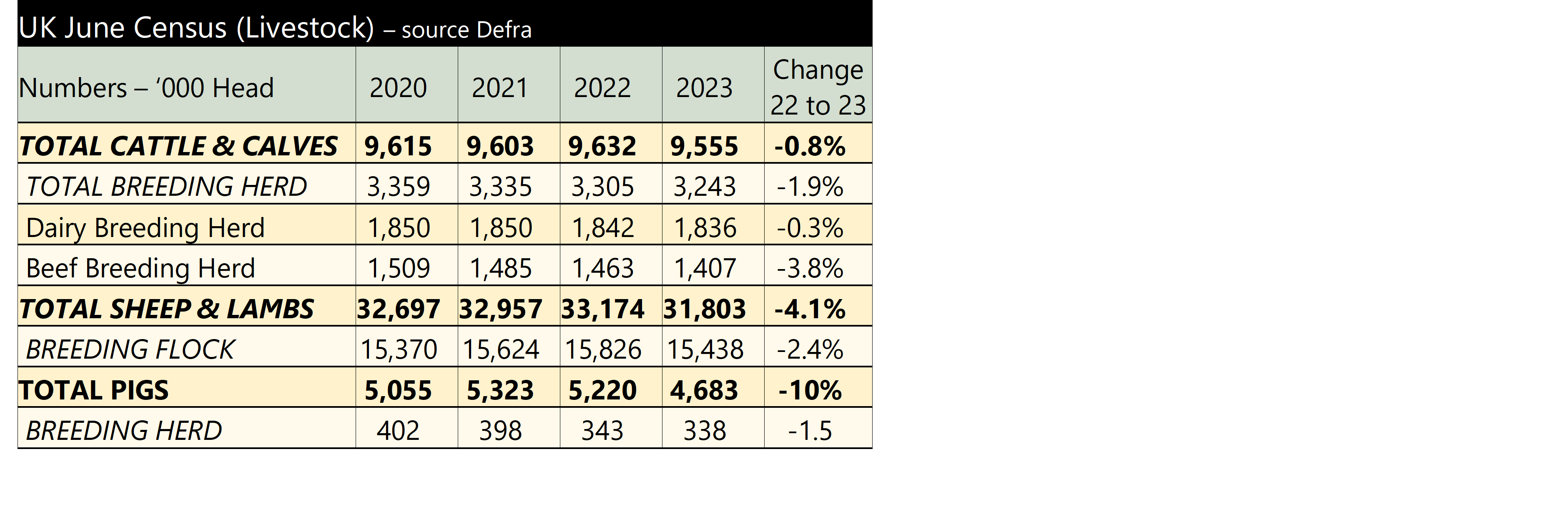

The economic climate for pig producers, although still challenging, is much better than this time last year, even so the breeding herd continues to contract. The female breeding herd decreased by 1.5%; falling to 338,000. This is the lowest it has been in the past 21 years. However gilts in pig saw a rise of 13%, suggesting some herd re-building is now happening. The large reduction in the total pigs number will partly be due to last year’s figure being high as pigs were having to remain on farm due to problems in the processing sector; there was an 11% fall in the number of fattening pigs, which now stand at just under 4.3 million.

The economic climate for pig producers, although still challenging, is much better than this time last year, even so the breeding herd continues to contract. The female breeding herd decreased by 1.5%; falling to 338,000. This is the lowest it has been in the past 21 years. However gilts in pig saw a rise of 13%, suggesting some herd re-building is now happening. The large reduction in the total pigs number will partly be due to last year’s figure being high as pigs were having to remain on farm due to problems in the processing sector; there was an 11% fall in the number of fattening pigs, which now stand at just under 4.3 million.